ObamaCare Subsidy Ruling Expected in June

Ads by +HealthNetwork

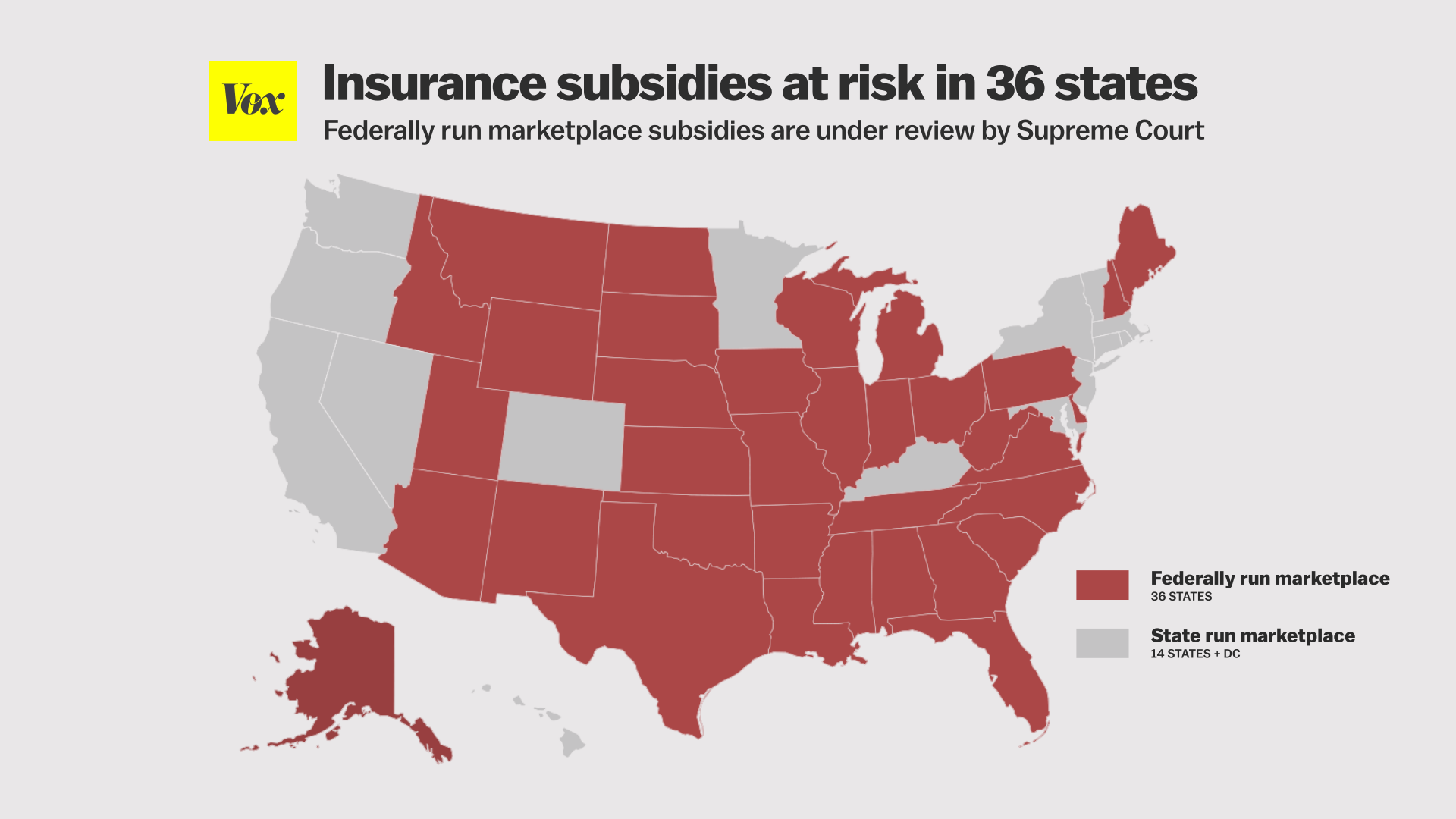

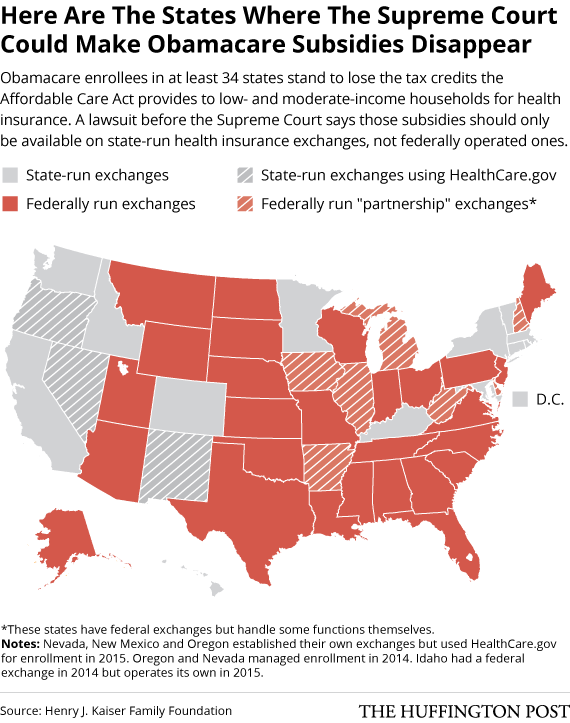

A Supreme Court ruling on King V Burwell (the lawsuit challenging the legality of subsidies offered through HealthCare.Gov) is expected in June of 2015.

A Supreme Court ruling on King V Burwell (the lawsuit challenging the legality of subsidies offered through HealthCare.Gov) is expected in June of 2015.

I wanted to share my story since so many people were affected by what just happened to myself and my coworkers yesterday. I was hired in as a full-time non-career employee. This meant that I had the ability to work 40 hours a week while learning about working for the State Of Michigan while I… Read More

Everything you need to know about ObamaCare for June 2015 including Hawaii’s exchange, a subsidy lawsuit, Florida and Medicaid, and other healthcare news (plus multiple instances of the word “boondoggle”).

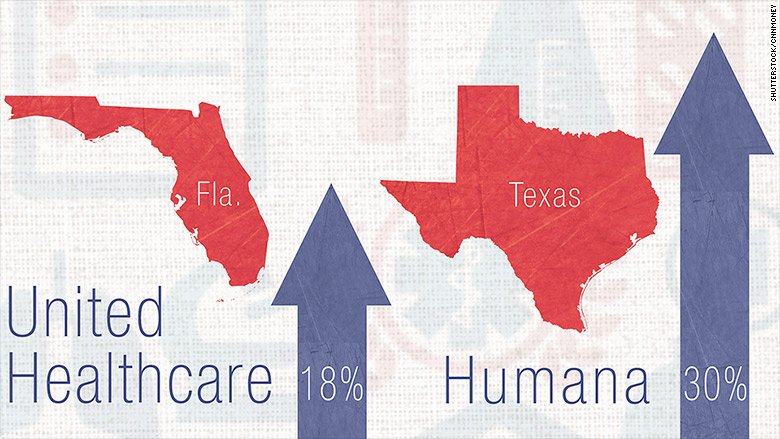

Insurers are planning rate hikes for 2016 under ObamaCare. ObamaCare being both the reason we know about it, and part of the reason it’s happening.

March 1, 2015 A new health insurance policy with Blue Cross Blue Shield of NC (BCBSNC), subsidized by Healthcare.gov begins. The subsidized rate is $257.83. This replaces my policy with BCBSNC that, on Jan 1, increased from $295 to $405 due to me turning 50. April 23, 2015 I called the Marketplace 800# (Healthcare.gov) to… Read More

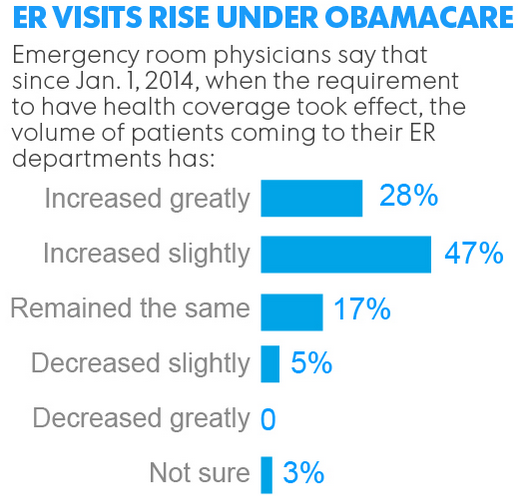

Memorial day is about remembering those who served our country, it’s also a day that has a high civilian death toll due to alcohol related events… and of course that means ER rooms across America working around the clock to save lives.

We could not afford this insurance but due to the law We were forced to get coverage. This year We are told it will double. We can’t make more income , I am disabled and My Wife makes less than than enough to keep us going I explained this to the representative and still were… Read More

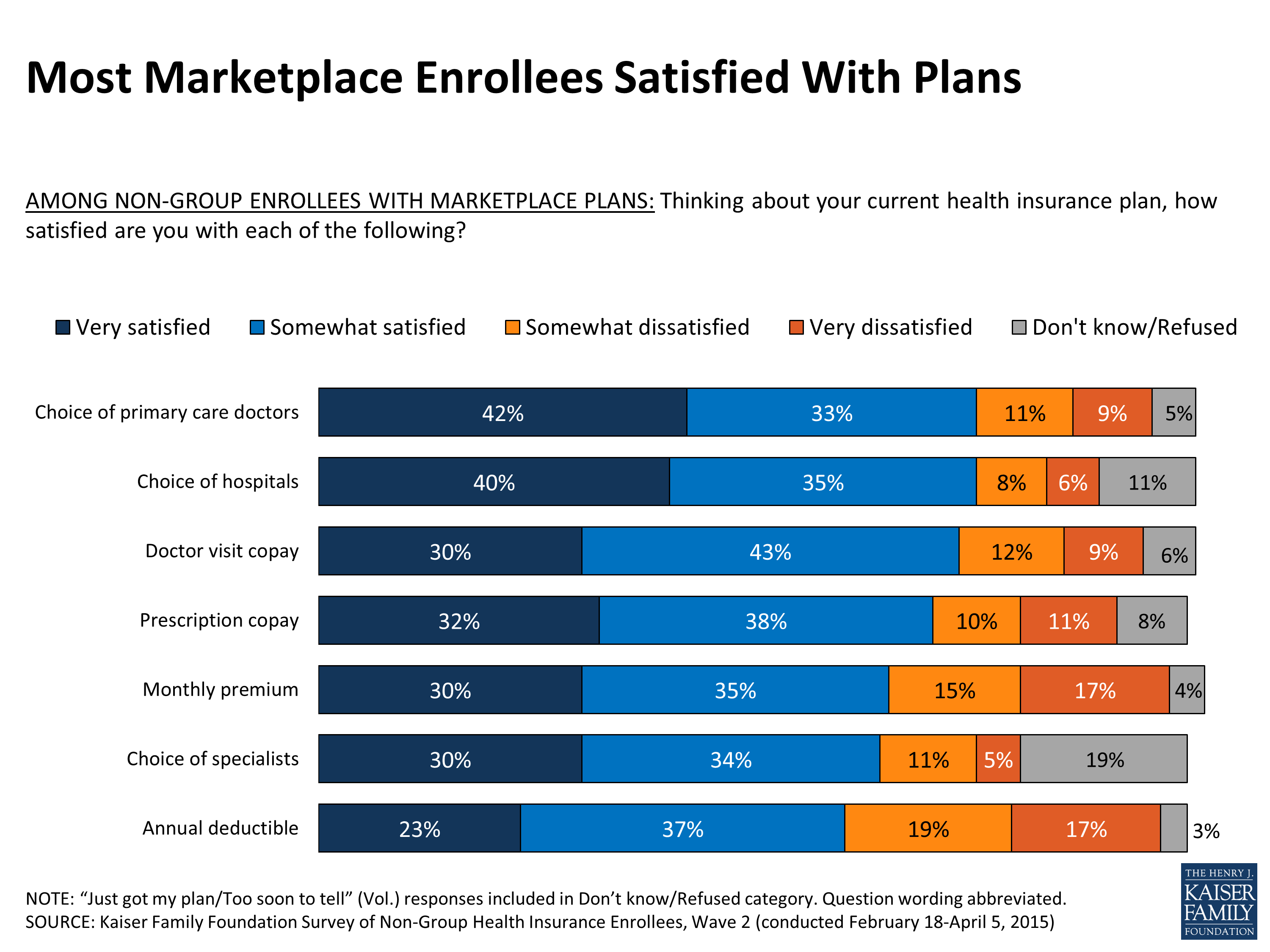

A recent survey from KKF.org shows that people like their non-group insurance under ObamaCare. The findings are pretty remarkable showing that Republicans are more likely to dislike their insurance then independents or democrats, more people are benefiting from plan costs under the ACA then not, and the only thing people like less than ACA-compliant plans are plans that aren’t ACA compliant.

A few weeks ago my daughter’s dentist told us the enivitable had come about. Rachel’s wisdom teeth were erupting and beginning to crowd her teeth. They had to come out. They gave us a referral to an oral surgeon and told us to do it sooner than later. I knew the procedure is not cheap,… Read More

This site is full of facts about ObamaCare. Facts based upon the theory of what ObamaCare would bring. I doubt that this will be published, but I am a REAL ObamaCare user. I received a significant benefit in subsidies by using the marketplace. Due to significant health problems and lack of income I pay a… Read More

A 2015 RAND corporation study shows gross enrollment numbers under the ACA of 22.8 million, while Medicaid sees 12 million according to CMS.

Last week a story went viral about a guy in South Carolina who didn’t get ObamaCare and ended up needing it.

HHS issued guidance to clarify the requirement that insurers cover at least one form of each of the 18 FDA approved contraception (birth control) methods.

Far in the distance, a long time from now, on June 5th 2015 the GOP will be expected to have a solution in place for the potential repeal of ACA subsidies. What is that you say? “June 5th isn’t the distant future, it’s actually less than a month away?… And the GOP have no solid agreed upon… Read More

My story is simple. I was retired at 62, applied for healthcare, received a reduced premium and a waivered amount for coverage due to my income. I decided that social security was not enough income, so I planned to go back to work. I cancelled my coverage when I accepted a job. 30 days later,… Read More

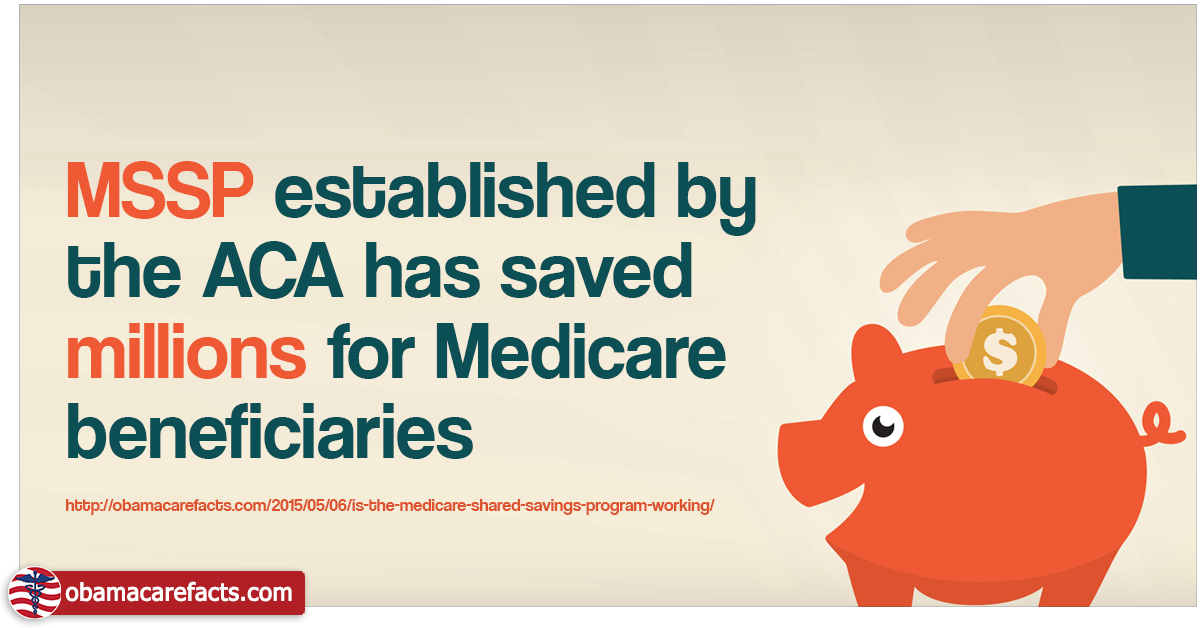

The Medicare Shared Savings Program (MSSP) established by the ACA allows healthcare providers to group together under ACOs to get paid for quality over quantity. Initial reports show savings for Medicare and providers under the Accountable Care Organization (ACO) model established under the ACA. Not all the initial “Pioneer ACO” groups faired equally as well, but overall… Read More

Have had lump in right breast since 2012. Had real insurance then and a mammogram and ultrasound and was told some cells didn’t look right, come back in 6 months. In 6 mos my Cobra insurance had ended. I was uninsured for the next 2 1/2 years. Scored Obama Care Ins. In March 2015. Was excited… Read More

Two years prior to the start of the Affordable Care Act, my health insurance premiums were raised by 40% each year for no reason, 20% each year. I was told by the insurance representative that it had nothing to do with my personal policy but instead that the industry was readying itself for the approaching… Read More

I am 50 years old and have never had health insurance, I always pay out of pocket in FULL for every doctors visit, every ER visit and have always had a reserve of $25,000 dollars saved up through small monthly contributions to draw on in case of emergencies. This is how I figured all American’s… Read More

A study shows that ER visits have increased as more people have gotten coverage under the Affordable Care Act. This expected short term outcome isn’t ideal, but speaks to habits of the previously uninsured, the fact that ER visits are covered under the ACA, and an increased doc shortage as demand outpaces supply in the short term.

If the Supreme Court rules against ObamaCare’s subsides the GOP has offered to allow subsidies to continue until 2016, in exchange for gutting the mandates. This isn’t the only proposal we have seen from the GOP in this regard, but is instead it is the common theme behind a number of different GOP based ideas…. Read More

I am very happy about the Obama Care Act. I was able to purchase health insurance through this plan, but my plan has a $5,000 deductible that has to be met before I can use it, so I feel like I am no further than I was before. This insurance plan has yet to send… Read More

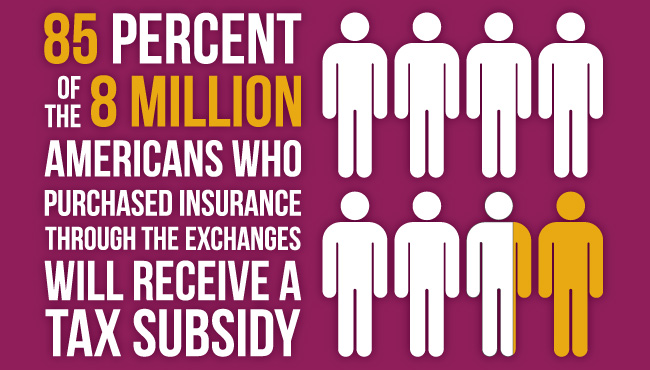

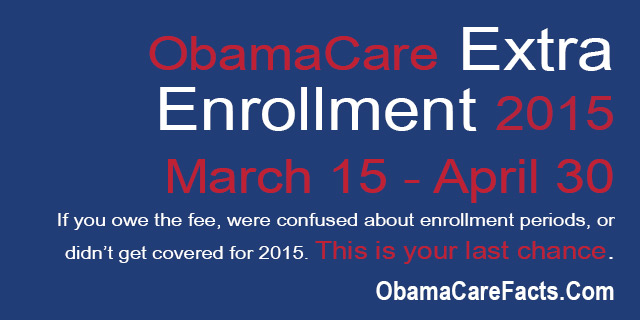

Open enrollment ended February 15, 2015 but last minute shoppers have until April 30 to get covered and avoid the fee, if they don’t have a health plan yet. *Healthcare.gov customers and select states only.

Discrimination, humiliation and denial. Words that I shouldn’t have to use to describe my experience at the doctor’s office while seeking treatment for my arthritic knee. I was openly treated as if I were less than human by a local clinic because I am receiving “Obamacare”. I have been poor all of my adult life…. Read More

My 12/4/12 heart surgery was possible because of the ACA which funded high risk pool insurance in my state just prior to the introduction of the ACA. I am very pleased to be healthy now and pleased to have insurance today !!