Form 8965, Health Coverage Exemptions and Instructions

Find out how to fill out Form 8965, Health Coverage Exemptions, the form for reporting ObamaCare Exemptions. We provide a simplified breakdown of form 8965.

Exemptions Form 8965 and Instructions

Here are the official IRS form and the instructions for 8965 for 2015 coverage. See below for a simplified breakdown of form 8965.

- Form 8965, Health Coverage Exemptions

- Form 8965, Health Coverage Exemptions Instructions NOTE: These instructions contain a worksheet for figuring out your Shared Responsibility Payment (the fee for not having coverage).

See our File Taxes for ObamaCare page for a breakdown of all healthcare-related tax forms.

What is Form 8965 Used For?

You’ll use form 8965 to report exemptions and to help you calculate the Shared Responsibility Payment on your 1040.

TIP: To fill out form 8965, you’ll want to have completed your 1040 and have your 1095 on hand. Please note you’ll need a Schedule 4 if you have to make a payment due to not having an exemption.

Who Needs to Fill out Form 8965?

Anyone who didn’t maintain coverage throughout the entire year needs to fill out an 8965 form.

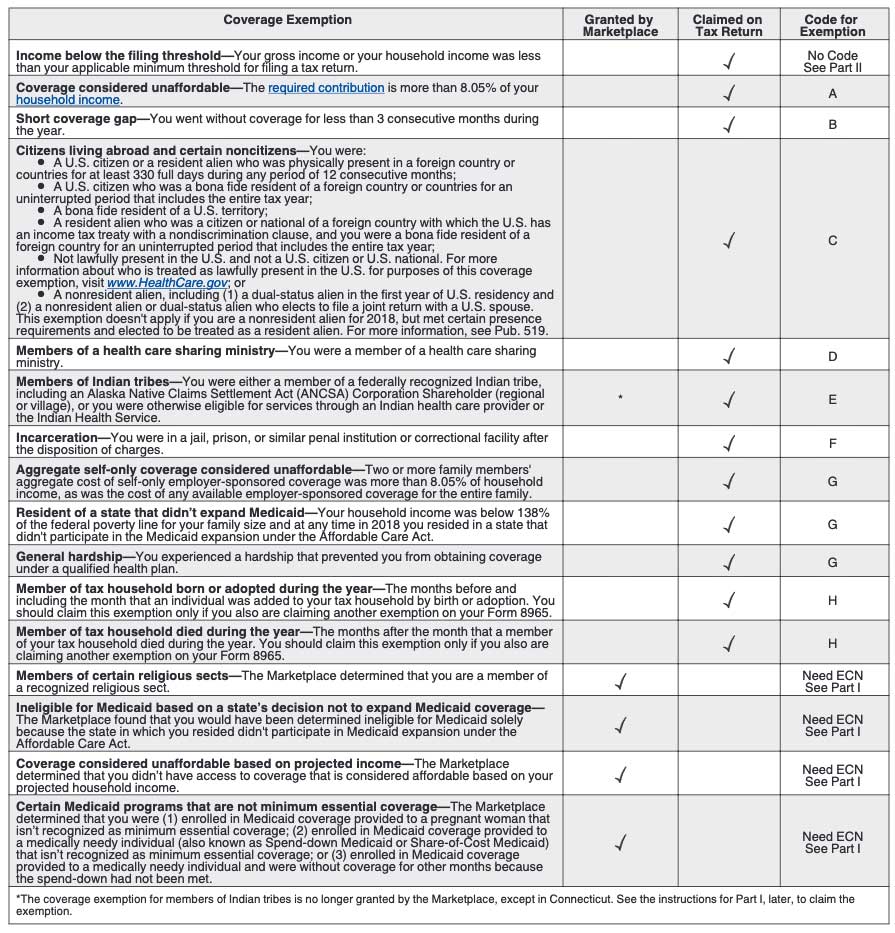

Exemptions and Electronic Confirmation Numbers (ECN)

Some exemptions require an Electronic Confirmation Number from the Health Insurance Marketplace. These reforms typically require proof and the submission of an application. This documentation should be done at the time of the cause of exemption.

Some exemptions last all year, others only last 3 months. Not all exemptions exempt you from the fee; some only initiate a special enrollment period.

Exemptions that don’t require confirmation numbers, such as short-term coverage gaps and affordability exemptions, can simply be claimed on this form. You won’t owe the fee for any months in which you have an exemption. However, you can technically have an exemption and still have coverage, and even cost assistance, in the same month.

See more on ObamaCare’s exemptions or read below for details, including the chart of all exemptions, as they apply to the 8965 form.

Coverage Gap Exemptions

As long as you enrolled in a Marketplace in 2014, you are allowed up to four consecutive months (January, February, March, and April) without coverage for 2014 only. Moving forward, you are only allowed three. If you get covered by January 1st, you can use that coverage gap exemption at another point in the year.

Affordability Exemptions

To determine if you are eligible for an affordability exemption, you can use the lowest cost silver plan tax tool found here. If the lowest cost silver plan on the Marketplace would cost more than roughly 8% of your household income for self-only (or average aggregate) coverage, then you are exempt. That page also includes a tool for figuring out the second lowest cost sliver plan.

ACA exemptions for the 2018 plan year.

Simplified Instructions for Form 8965, Health Coverage Exemptions and Instructions

IMPORTANT: Some specifics may change each year, but the general information below should be true in any year. Please use the current official instructions when filing taxes.

Depending upon the type of exemption you have, you’ll either fill out Part I, Part II, or Part III.

Part I. Marketplace-Granted Coverage Exemptions for Individuals:

If you or a member of your tax household have an exemption granted by the Marketplace, complete Part I

Line 1-6 Name, SSN, and ECN. Here you will report each person and the Electronic Confirmation Number (ECN) you received when you claimed your exemption through the marketplace. If you didn’t need to apply for an exemption, you’d claim that in the next section.

Part II. Coverage Exemptions for Your Household Claimed on Your Return:

Line 7 Income below filing threshold. You’ll use line 7 a and b to report that you are claiming an exemption because you are below the tax filing threshold. A is for regular exemptions based on income, B is for a hardship exemption based on income.

Part III. Coverage Exemptions for Individuals Claimed on Your Return:

If you or a member of your tax household are claiming an exemption on your return, complete Part III.

Here you will report an exemption that doesn’t require an Electronic Confirmation Number for each month, or if applicable, the full year.

Filing Based on Your Health Insurance and Exemption Status

If you had health coverage or an exemption, simply check the “Full-year health care coverage or exempt” box on your 1040.

If you took an exemption, make sure to attach your 8965 form when you file your taxes.

If you can’t check the box, you generally must report a shared responsibility payment on Schedule 4.

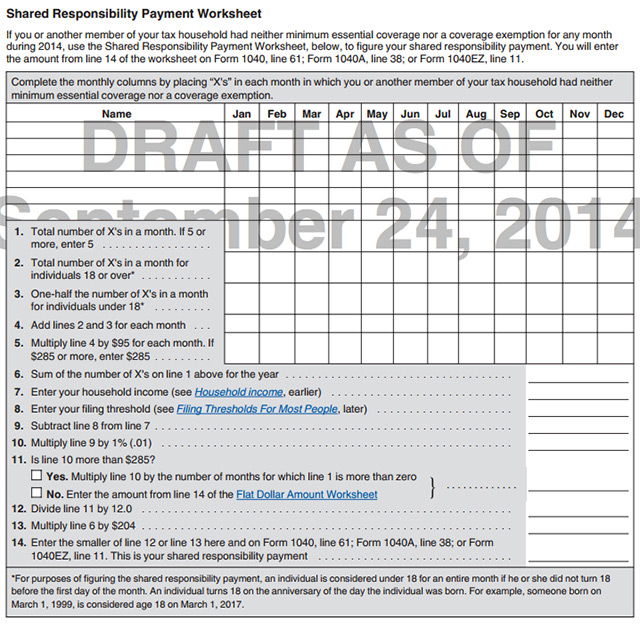

How to Make the Shared Responsibility Payment

There is no Shared Responsibility Form. The amount is derived from the Shared Responsibility Payment Worksheet, found on form 8965 instructions, and is reported on a 1040 Schedule 4.

This is the last ACA-related thing you will fill out since it requires knowing information from other forms first. The image below is a draft. The actual instructions have not yet been released.

TIP: The worksheet below is a draft, you can find this year’s sheet in the 8965 instructions as noted above.

ObamaCare Taxes: Form 8965, Health Coverage Exemptions![]()

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio