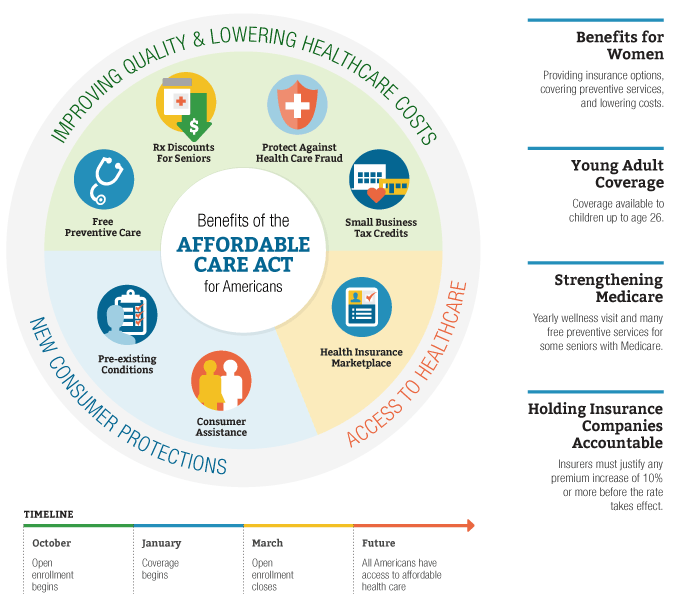

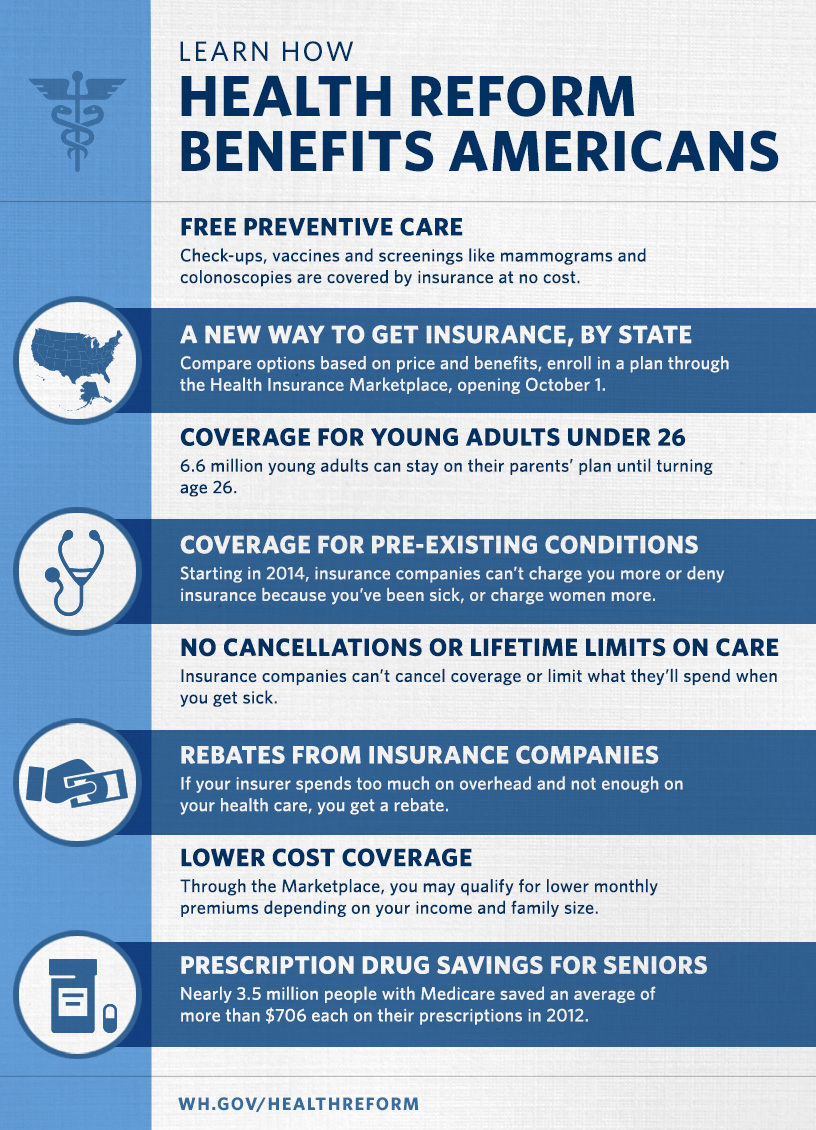

Benefits Of ObamaCare: Advantage of ObamaCare

New Benefits, Rights, and Protections in the Affordable Care Act

ObamaCare offers many new benefits, rights, and protections. Most of the benefits of ObamaCare are already here, more benefits are coming.

A Summary of ObamaCare’s Benefits, Rights, and Protections

Benefits, rights, and protections of the Affordable Care Act (also called the ACA or Obamacare), include:

- Letting young adults stay on their parents’ plan until 26

- Stopping insurance companies from denying you coverage or charging you more based on health status

- Stopping insurance companies from dropping you when you are sick or if you make an honest mistake on your application

- Preventing gender discrimination

- Stopping insurance companies from imposing unjustified rate hikes and helping to keep rates down with the 80/20 rule and rate review provision

- Doing away with lifetime and annual dollar limits

- Giving you the right to a rapid appeal of insurance company decisions

- Creating new Health Insurance Marketplaces (HealthCare.Gov and the state-run Marketplaces) to allow shoppers to compare health plans

- Expanding coverage to tens of millions by subsidizing health insurance costs through the Health Insurance Marketplaces

- Expanding Medicaid to millions in states that chose to expand the program

- Providing tax breaks to small businesses for offering health insurance to their employees

- Requiring large businesses to insure full-time employees

- Requiring all insurers to cover people with pre-existing conditions

- Making CHIP easier for kids to get

- Improving Medicare for seniors

- Expanding women’s health services, including many new free preventive treatments and screenings

- Ensuring all plans cover minimum benefits like limits on cost-sharing and ten essential benefits including free preventive care, OB-GYN services with no referrals, free birth control, and coverage for emergency room visits out-of-network

- Simplifying the process of understanding benefits by requiring insurers to provide an easy-to-understand summary of a health plan’s benefits and coverage

- Reforming the healthcare industry and cutting wasteful spending

- New rules and regulations ensure that all major medical plans provide minimum actuarial value and have a maximum out-of-pocket costs

- Plus many more benefits, rights, and protections.

Each new benefit, right, and protection is part of one or more of the provisions contained in the Affordable Care Act or subsequent rule changes.

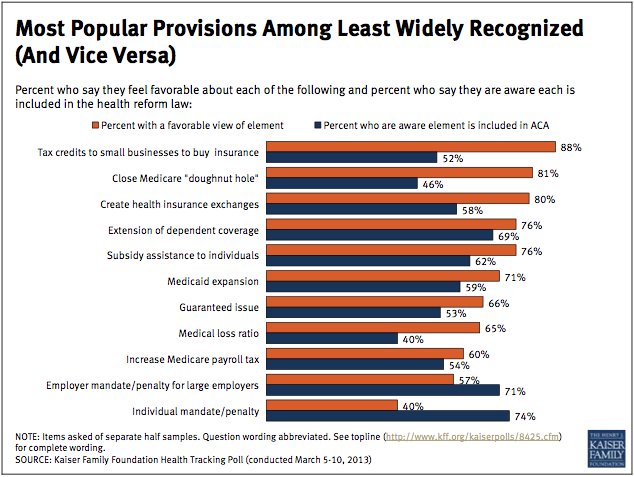

As you can see by the image below, some of the most popular provisions of the Affordable Care Act are the ones that the least amount of people are aware of.

FACT: ObamaCare guarantees individuals and families in the private market, public market, and workplace a number of benefits, rights, and protections on all major medical plans sold after 2014. Many benefits went into effect in 2010 when the law was signed; others didn’t start until 2014 (or later in a few select cases), and a few won’t be fully in effect until the 2020s (that is if it can avoid a full repeal).

TIP: Know the Law. The Affordable Care Act contains 10 titles; each title addresses a different aspect of health care reform. Title I Quality, affordable health care for all Americans addresses most of the new benefits, rights, and protections. Check out our Summary of Provisions of the Patient Protection and Affordable Care Act for a plain English summary of each provision pertaining to the “benefits of ObamaCare.”

Grandfathered plans: Plans that had started before the ACA was signed are sometimes called grandfathered plans. Learn more about grandfathered plans and keeping your health care plan.

Who Benefits From ObamaCare?

Everyone benefits from ObamaCare in one way or another.

Many Americans who did not have coverage before the law got access to quality affordable health insurance through either the federal marketplace, their State’s health insurance marketplace, or the expansion of Medicaid and the Children’s Health Insurance Program (CHIP) starting in 2014.

Then, starting in 2016, the employer mandate expanded access to work-based coverage to full-time workers who weren’t already offered health benefits.

That didn’t mean there was 100% coverage, but that did mean that everyone had access in theory under the law (in practice many states rejected Medicaid expansion and so millions went without coverage).

Meanwhile, for the Americans who already had health insurance, the benefits, rights, and protections offered under their current plan generally increased (and in some cases they got access to cost assistance too).

Many Americans don’t realize that they have been enjoying many of ObamaCare’s benefits, rights, and protections since the Affordable Care Act was signed into law in 2010.

The video below does a great job at explaining your new benefits, rights, and protections under the Affordable Care Act:

Advantages Offered By ObamaCare

Before ObamaCare (the Affordable Care Act) many low-to-middle income Americans and small businesses had trouble affording healthcare for themselves and their families. If you were sick in the past, you could be denied health coverage or treatment with little right to an appeal. Companies could charge you more based on your health status and charged higher rates for being a woman (making insurance unaffordable). If you lost work-based coverage, you would have to rely on expensive COBRA insurance, which was only offered for a limited time.

The Affordable Care Act contains provisions that solve all of these problems. We will get to your rights and protections in a minute. First, let’s look at how ObamaCare addresses the cost.

Affordable Care Act Fact: Before the ACA over 60% of bankruptcies in the U.S. were medical-related and almost 3/4 went bankrupt despite having insurance. By 2014 the elimination of both lifetime and annual limits protected Americans from going bankrupt by allowing them to continue treatment as long as they need it, not just until their dollar limit was reached.

ObamaCare Benefits: the ACA Makes Health Insurance More Affordable and More Available

As one benefit of ObamaCare, if you make less than 400% of the federal poverty level, you may be eligible to receive subsidies for reduced premiums via tax credits offered on your State’s Health Insurance Exchange. Exchanges are online Marketplaces where Americans can purchase health plans that enjoy all the new benefits, rights, and protections offered by the law.

If you make less than 250% of the federal poverty level, you may be eligible for help with out-of-pocket costs on health insurance purchased on the marketplace.

In State’s that opted to implement Medicaid expansion more men, women, and children to be eligible for Medicaid (in fact, in many states, any adult making less than 138% of the poverty level is eligible and the thresholds are even higher for children and families with young children).

Cost assistance will help many low and middle-income individuals and families to purchase affordable health insurance. Find out more about Receiving Subsidies, Tax Credits, and Cost Assistance on the ObamaCare Health Insurance Exchange.

Cost assistance can also help small businesses with less than 25 full-time equivalent employees with up to 50% of their share of their employee’s premiums. Learn more about ObamaCare and Small Business tax breaks.

Ten Essential Benefits: A Quick Summary of ObamaCare “Essential Health Benefits.”

The new ObamaCare health care law states that health plans offered in the individual and small group markets, both inside and outside of the Health Insurance Marketplace (also called Health Insurance Exchanges), offer “essential health benefits.” Please note that grandfathered plans purchased before the bill was signed into law may not be required to provide these services. Read more information about ObamaCare “grandfathered plans.”

Starting January 1st of 2014, the following “Ten Essential Benefits” had to be included under all insurance plans with no lifetime or annual dollar limits:

- Ambulatory patient services (Outpatient care). Care you receive without being admitted to a hospital, such as at a doctor’s office, clinic, or same-day (“outpatient”) surgery center.

- Emergency Services (Trips to the emergency room). Care you receive for conditions that could lead to serious disability or death if not immediately treated, such as accidents or sudden illness.

- Hospitalization (Treatment in the hospital for inpatient care). Care you receive as a hospital patient, including care from doctors, nurses, and other hospital staff, laboratory and other tests, medications you receive during your hospital stay, and room and board.

- Maternity and newborn care. Care that women receive during pregnancy (prenatal care), throughout labor, delivery, and post-delivery, and care for newborn babies.

- Mental health services and addiction treatment. Inpatient and outpatient care provided to evaluate, diagnose, and treat a mental health condition or substance abuse disorder.

- Prescription drugs. Medications that are prescribed by a doctor to treat an illness or condition.

- Rehabilitative services and devices – Rehabilitative services (help recovering skills, like speech therapy after a stroke) and habilitative services (help developing skills, like speech therapy for children) and devices to help you gain or recover mental and physical skills lost to injury, disability or a chronic condition (this also includes devices needed for “habilitative reasons”).

- Laboratory services. Testing provided to help a doctor diagnose an injury, illness, or condition, or to monitor the effectiveness of a particular treatment. Some preventive screenings, such as breast cancer screenings and prostrate exams, are provided free of charge.

- Preventive services, wellness services, and chronic disease treatment. This includes counseling, preventive care, such as physicals, immunizations, and screenings, like cancer screenings, designed to prevent or detect certain medical conditions. Also, care for chronic conditions, such as asthma and diabetes. Note: please see our full list of Preventive services for details on which services are covered.

- Pediatric services. Care provided to infants and children, including well-child visits and recommended vaccines and immunizations. Dental and vision care must be offered to children younger than 19. This includes two routine dental exams, an eye exam, and corrective lenses each year.

Essential Benefits are provided with no out-of-pocket limits to the amount of care you can receive on every insurance plan sold on ObamaCare’s Online Health Insurance Marketplace.

Exceptions:

- Insurance companies can still put a yearly dollar limit and a lifetime dollar limit on spending for health care services that are not considered essential health benefits.

- Some health insurance plans may have received a temporary waiver from the rules on yearly dollar limits. Yearly limit waivers end with plan or policy years beginning in 2014.

Read more about the Ten Essential Health Benefits

Essential Benefits: Cost Sharing and Dollar Limits

Essential benefits cannot be subject to lifetime or annual dollar limits, and all non-grandfathered health plans must limit the total out-of-pocket costs enrollees pay for in-network, essential health benefits.

While you may have to meet a certain amount of out-of-pocket expenses (deductible) before essential benefits are covered, the Affordable Care Act prohibits health plans (grandfathered and non-grandfathered) from imposing annual and lifetime dollar limits on essential benefits. Health plans can still however set limits on the number of times you can receive a certain treatment.

TIP: Above we covered all the “essentials,” below is just a detailed list to help bring everything together and give you a timeline of when each benefit was implemented.

Full list of Preventative Services Offered By ObamaCare

The following links will give you a breakdown of all included preventative care benefits covered by ObamaCare at no out-of-pocket cost for all adults, women, children and seniors.

The following is a full list of benefits, rights, and protections under ObamaCare is from Consumer Reports:

Full list of Protections and Benefits Offered By ObamaCare (The Affordable Care Act) From 2010

Below is a detailed list of the benefits, rights, and protections that were offered since 2010 under the ACA.

Protections

Whether your health insurance is purchased by you or your employer, the health law has outlawed practices that have left people without health insurance when they need it most. These protections include:

Curbs on canceling policies. Insurers can no longer cancel your policy if you get sick, a practice known as “rescission.” They cannot cancel your coverage if you make an honest mistake on your application.

Rapid appeals. Consumers can appeal insurance company decisions to an independent reviewer and receive a response within 72 hours for urgent medical situations.

Ban on lifetime limits. Major or long-term illness can rack up serious medical bills. Health insurance policies used to set lifetime limits on how much they would pay for an individual’s medical bills. These are now illegal, meaning people with insurance won’t have to get into debt because their coverage runs out.

Annual dollar limits on their way out. As of September 23, 2012, the law says annual dollar limits must be no less than $2 million. In January 2014, limits will be completely eliminated. Exceptions: Insurers can still impose other types of benefit limits like doctor visit limits, prescription limits, or limits on days in the hospital.

Better Benefits

Free preventive care and annual checkups. The law focuses on prevention and primary care to help people stay healthy and to manage chronic medical conditions before they become more complex and costly to treat. New private health plans must cover and eliminate cost-sharing (co-payment, co-insurance, or deductible) for proven preventive measures such as immunizations and cancer screenings. Additional preventive measures for women kicked in August 2012, including free well-woman visits, screening for gestational diabetes, domestic violence screening, breast-feeding supplies, and contraception, all with no cost-sharing. Exceptions:

Workplaces run by religious organizations that object to birth control do not have to pay for contraception, but insurers must pick up the cost. Existing plans that haven’t changed significantly since passage of the law can continue to charge for preventive care until 2014.

Premium rebates if insurers underspend on care. The health law says that most insurers must spend at least 80 percent (85 percent for insurers covering large employers) of the premiums you pay on medical care and quality improvements. If insurers spend too much on overhead, such as salaries, bonuses, or administrative costs, as opposed to health care, they must issue premium rebates to consumers each summer.

Because of the new health law, 12.8 million individuals and businesses got back more than $1.1 billion in rebates in 2012 from insurance companies who underspent on medical care.

Standard disclosure forms. Starting September 23, 2012, all health plans must use a standardized form to summarize benefits and coverage, including information on co-payments, deductibles, and out-of-pocket limits. Insurers must note any excluded services all in one place. Insurers must also calculate and disclose your typical out-of-pocket costs for two medical scenarios: having a baby and treating type 2 diabetes. Future years will include more coverage examples.

Doctor Choice & Emergency Room Access. You have the right to choose the doctor you want from your health plan’s provider network. You also can use an out-of-network emergency room without penalty. You don’t need to get a referral from a primary care provider before you can get obstetrical or gynecological (OB-GYN) care from a specialist either.

Expanding coverage

The law makes it easier for some uninsured Americans to find more affordable health insurance right now:

Young adults can stay on a parent’s plan until age 26. Health plans must let young adults remain as dependents on their parent’s policy until they turn 26, regardless of whether they live at home, attend school, or are married. Exception: Some health plans are not required to extend benefits to young adults if they can get coverage at work; this exception went away in January 2014.

Chipping away at pre-existing condition exclusions. As of 2014, insurers were no longer be able to deny coverage to people with pre-existing conditions or charge them more for premiums. Meanwhile, the health law offered some temporary help.

Adults with pre-existing conditions who were without coverage for at least six months may have been eligible for subsidized coverage through the temporary Pre-existing Condition Insurance Plan in their state.

Children under 19 with pre-existing conditions cannot now be denied coverage by most insurers. Until 2014, however, insurers could charge more for premiums than they charge for someone without such conditions. Exception: Some individual plans still refused to cover a child until January 2014.

There was a 365 day waiting period for individuals with pre-existing conditions the BCBS terms and the ACA section “SEC. 101. NATIONAL HIGH-RISK POOL PROGRAM.” We can verify that there was a 365 day waiting period for coverage of pre-existing conditions upon purchasing insurance. This was scheduled to be eliminated along with the pool in 2017.

There is also an “Exclusion Rider” policy that essentially said that, until 2014, you could be denied coverage on a medically underwritten health insurance policy. EX. You had surgery previously and you need another operation for the same issue.

The PCIP Pre-existing Condition Insurance Plan: makes health coverage available to you if you are a U.S. citizen or reside here legally, you have been denied health insurance because of a pre-existing condition, and you’ve been uninsured for at least six months.

These plans were expensive and thus probably beyond the means of low-income individuals. The Program ended in 2014 when insurance through the exchange will cover pre-existing conditions

Visit PCIP.gov for information on plans, premiums, eligibility, and how to apply in your state.

You can apply online or print and complete a paper application from the website. Or, call 1-866-717-5826 (TTY 1-866-561-1604) to apply.

Full list of Protections and Benefits Offered By ObamaCare (The Affordable Care Act) After 2014

Some of the biggest changes resulting from the health law take effect January 1, 2014, with the goal of making affordable health care available for all Americans, regardless of their medical history or ability to pay.

Below is a detailed list of the benefits, rights, and protections that were offered since 2014 under the ACA.

Most Americans will be required to have health insurance. As of January 1, 2014, Americans who can afford coverage will be required to purchase health insurance or pay a tax penalty.

No more pre-existing conditions denials. Starting in January 2014, insurers cannot deny coverage to anyone, regardless of pre-existing conditions. And they cannot charge you more because of your gender or more than they charge a healthy person your age. That means you can buy health insurance even if you are seriously ill.

Online insurance marketplaces. Read More About ObamaCare Online Insurance Marketplaces.

More primary care doctors, coordinated care. With millions more insured Americans on the way, the current national shortage of primary care physicians presents an ongoing challenge to access in the health-care system. The health law has begun to fund training for more primary care physicians and increased resources for community health centers. It also promotes better-coordinated care and increased payment rates for primary care doctors who accept Medicaid or work in rural areas.

Essential benefits offer a minimum level of coverage. A minimum level of coverage known as essential benefits must be part of plans, effective January 1, 2014. Individual health plans and those sold to small businesses—whether sold in or out of the health insurance exchanges—must offer a comprehensive package of essential benefits.

Medicaid expansion assists low-income Americans. Up to 16 million Americans could be eligible for Medicaid. As of January 1, 2014, states that choose to can expand their Medicaid programs to legal residents under age 65 earning less than $15,302 for an individual and $31,155 for a family of four. States that opt-in will get federal funding to cover 100 percent of the costs for the first three years, then 90 percent thereafter. Exception: Medicaid expansion was the one part of the law that changed significantly with the U.S. Supreme Court ruling on June 28, 2012. The Justices said states were allowed to refuse to expand Medicaid to all low-income adults without losing all federal funding for existing Medicaid programs. If a state opted out, it left some of its poorest residents without coverage.

It’s obvious that ObamaCare offers individuals and families a wide range of benefits and services, but the benefits of ObamaCare go beyond services and tax breaks. The core of health care reform is about Americans ensuring their right to health care, allowing them an opportunity to find that new job without jeopardizing their access to coverage and the comfort of knowing that their loved ones will be taken care of when they need it the most. Support ObamaCare, protect your interests, and help to give every American access to the benefits of the Affordable Care Plan.

The Benefits of ObamaCare For You and Your Family![]()

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio