Grandfathered Plans

Grandfathered Health Plans Don’t Have to Follow ObamaCare’s Rules and Regulations.

Grandfathered plans are plans that were purchased before March 23, 2010. These plans have a grandfathered status and don’t have to follow ObamaCare’s rules and regulations or offer the same benefits, rights and protections as new plans. This means that on many old plans you can still be dropped form coverage for reasons other than fraud, be denied treatment for preexisting conditions, face annual and lifetime dollar limits and more.

Grandfathered plans are plans that were purchased before March 23, 2010. These plans have a grandfathered status and don’t have to follow ObamaCare’s rules and regulations or offer the same benefits, rights and protections as new plans. This means that on many old plans you can still be dropped form coverage for reasons other than fraud, be denied treatment for preexisting conditions, face annual and lifetime dollar limits and more.

If you like your grandfathered health plan, you can keep it. However, if your plan loses grandfathered status you may have to upgrade to a new plan that meets the requirements of the Affordable Care Act (ObamaCare). In most cases your health insurance provider will make you aware if you have to switch plans for 2015 (UPDATE: in 2014 this was extended to 2017). Some States with working health insurance marketplaces, like Washington State, have rejected the new 2015 deadline and will enforce the original 2014 deadline. Learn more about Keeping Your Insurance Under ObamaCare.

Grandfathered plans don’t have to provide the new benefits, rights, and protections of the Affordable Care Act.

Does Your Health Plan Have a Grandfathered Status?

March 23, 2010 was the day that the Patient Protection and Affordable Care Act (PPACA) became law. Since then private individual and family plans and private group health insurance plans are classified as one of two groups. The groups are:

1. Health insurance plans that were implemented after the act was passed and;

2. “Grandfathered” plans which went into effect before the act passed.

If You Like Your Plan You Can Keep it…

The President has announced a plan to allow Americans to keep their health insurance until 2015 (UPDATE: in 2014 this was extended to 2017) even if it doesn’t comply with the new benefits, rights, and protections of the ACA. Being able to keep your plan depends upon your state agreeing with the extension and your insurer agreeing to keep furnishing the plan. Check out our page on keeping your plan for more details.

In general, you can keep your current health plan after 2015 if:

• Your private plan has grandfathered status and remains unchanged by the provider.

• You have a non-grandfathered private plan that meets the requirements of the Affordable Care Act (listed below).

• You have Medicare, Medicaid, TRICARE or another form of Public health care.

You may have to switch to a new health plan if:

• Your plan doesn’t have, or loses, grandfathered status and doesn’t meet the requirements of the ACA.

Can My Plan Lose Grandfathered Status?

If a plan see significant changes (listed below) for any reason it will lose its grandfathered status. Many insurance companies are opting to update plans and causing them to lose grandfathered status, that combined with the large number non-compliant plans sold after 2010, means millions of Americans will have to switch to a ACA compliant plan for 2015 (UPDATE: in 2014 this was extended to 2017).

Americans with plans that lose grandfathered status will either have to switch to a new version of the plan or choose a different plan. In many cases Americans will be able to find a comparable plan on their State’s health insurance marketplace and may even qualify for subsidies. If you make less than 400% of the Federal Poverty Level you may qualify for cost assistance on the exchange.

If a provider makes changes to a grandfathered health plan, it losses its grandfathered status, and compliance with the Affordable Care Act’s new standards became necessary.

According to HHS estimates:

• 40 percent to 67 percent of individual policies will lose grandfathered status by 2011;

• 34 percent to 64 percent of large employer group plans (100 or more employees) will lose their grandfathered status by 2013: and

• 49 percent to 80 percent of small employer group plans (three to 99 employees) will lose their grandfathered status by 2013.

Please note that insurance companies are electing to change grandfathered plans and thus asking Americans to choose new plans. While the law states that if a plan is changed you’ll need to choose a new plan, it does not mandate that insurers change plans with grandfathered status.

Every year about 40% of insured switch healthcare plans regardless of the ACA. Typically, you are in a one year contract with health insurance companies and it is at their discretion whether they continue to offer a plan or not.

How Does a Health Plan Lose Grandfathered Status Under the Affordable Care Act?

Generally, a plan will lose grandfathered status if any of the following changes are made after March 23, 2010. These rules apply separately to each “benefit package” offered by an employer:

- A significant cut or reduction in benefits by eliminating all or substantially all of the benefits to diagnose or treat a condition, or any necessary element to diagnose or treat a condition.

- Raising coinsurance charges.

- Significantly raising fixed cost-sharing (i.e., deductibles and out-of-pocket limits) by more than medical inflation (as measured from March 23, 2010) plus 15 percentage points.

- Significantly raising copayment charges by more than the greater of: (i) medical inflation (as measured from March 23, 2010) plus 15 percentage points or (ii) $5 (adjusted for medical inflation).

- Significantly lowering the rate of employer contributions by 5 percentage points for any coverage tier.

- Adding or tightening an annual limit (with one exception).

- Reclassifying employees so that the reclassified employees are eligible for a different plan (even if it’s a grandfathered plan), without a bona fide employment reason.

- Failing to continuously maintain at least one covered individual (not necessarily the same individual).

Generally, if any of the changes listed below were made to a plan after March 23, 2010, they will not, by themselves, cause a plan to lose grandfathered status:

- Changes to third-party administrators or insurers in the group market.

- Changing premiums.

- Changes to comply with state or federal law, including voluntary changes to implement ACA.

- Agreeing to binding renewals before March 23, 2010, effective on or after March 23, 2010.

- Allowing new employees or new enrollees who are not new employees and their dependents to enroll (subject to certain anti-abuse rules).

- Allowing new dependents of current subscribers to enroll.

Why Grandfathered Status is Significant

Any health care insurance plan in effect before March 23, 2010 is a grandfathered plan as defined by the Affordable Care Act. There are both pros and cons of grandfathered plans, all rooting from them not having to comply with the ACA. Grandfathered plans are allowed to do things like offer tiered benefits, based on salary, to employees. Grandfathered plans are also allowed to place lifetime and annual limits on treatment. Let’s look at some of the aspects of the law grandfathered plans don’t have to comply with.

Requirements of the Affordable Care Act

Grandfathered plans are exempt from 13 additional requirements of the new act explained below.

- Annual Reports: Plans that are effective after March 10, 2010 are required to send a report each year to the Secretary of Health and Human Services that explains how the company’s employer provided insurance plan would improve health outcomes. Grandfathered plans do not have to do this.

- New Government Reports: Under the new law, employers are required to send to their state insurance commission certain information about enrollment, claim, and payment policies. This does not apply to grandfathered plans.

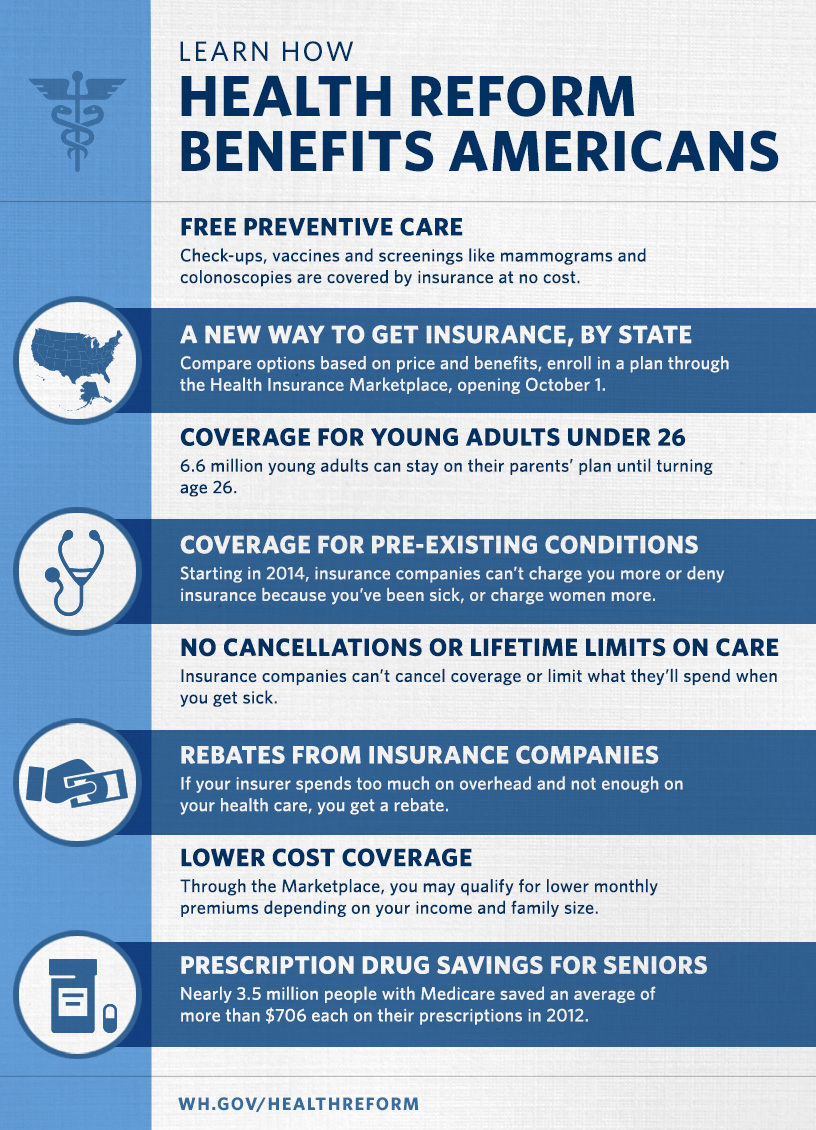

- First dollar coverage: All new plans must provide certain preventative services free to enrollees. These services include mammography examinations, an annual checkup and blood test and other preventative or screening services. Grandfathered plans are exceptions to this rule.

- Health Status: Under the ACA insurers can’t charge more or deny care based on health status (preexisting condition). Grandfathered insurance plans are exempt from this.

- Guaranteed Access: This provision mandates health insurance carriers give insurance to any individual or employee that applies for insurance. Grandfathered insurance plans are exempt from this provision.

- Any Willing Provider: Requires insurance plans to allow any willing provider of health care services to participate in the plan as a provider as long as they operate within the scope of their license. Grandfathered plans don’t have to.

- Emergency Services: Requires that every new plan cover emergency services without prior authorization. Grandfathered plans do not need to meet this requirement.

- Rule Regarding Establishing Premium Rates: A provision of the new act is the “Fair Health Insurance Premiums.” This provision only allows an insurance company to charge a maximum of a 3:1 difference for age difference and 1.5:1 for tobacco use. This does not apply to grandfathered plans.

- Essential Benefits: When the law passed, new plans are now required to offer the essential benefits as outlined in the act (including preventive treatments and women’s services). Grandfathered plans are exempt from this requirement.

- Claims Review: The new law expands the internal review process regarding denied services. There is no such requirement for grandfathered plans.

- Clinical Trials: The new health insurance law requires that insurance companies continue to provide health insurance to enrollees in a clinical trial. Grandfathered plans don’t have to.

- Annual and Lifetime Limits: Both annual and lifetime dollar limits are banned on all essential healthcare services. Grandfathered plans can have dollar limits.

- Gender Discrimination: Women cannot be charged higher rates than men. Grandfathered plans can charge more to women.

Remember, if a grandfathered plan raises rates or changes benefits they may lose their grandfather status. In some cases (especially if you are eligible for subsidies) it may be in your best interest to check out the health insurance marketplace and see if there is a better plan for you and your family. Employees can to ask their benefits office if the plan is a grandfathered plan or not. If you do have a grandfathered plan through work that means your work based health insurance won’t prevent your family from getting subsidies on the marketplace.

What Benefits Rights and Protections Does a Grandfathered Plan Have to Offer?

Grandfathered plans aren’t exempt from all of ObamaCare’s new rules. According to shrm.org these include:

• Limits on waiting periods (starting with the 2014 plan year).

• Patient Centered Outcomes Research Institute fee (PCORI fee).

• Transitional reinsurance fee.

• Summary of Benefits and Coverage.

• Notice regarding public exchanges (due. Oct. 15).

• No rescissions of coverage except for fraud, misrepresentation, or non-payment.

• Lifetime dollar limit prohibitions on essential health benefits.

• Phase-out of annual dollar limits on essential health benefits, with all limits removed by 2014.

• Dependent child coverage to age 26 (an exception for grandfathered plans when other coverage is available expires in 2014).

• Elimination of pre-existing condition limitations (for children currently and all covered persons starting in 2014).

• W-2 reporting of health care coverage costs (this only applies if the employer provided more than 250 W-2s for the prior calendar year).

• Wellness program rules.

• Minimum medical loss ratios (this only applies to insured plans).

• Employer shared responsibility (“play or pay”) requirements (starting with 2015).

• Employer reporting to IRS on coverage (starting in 2015).

• Excise (“Cadillac”) tax on high cost plans (starting in 2018).

• Automatic enrollment (this only will apply to employers with more than 200 full-time employees; this requirement has been delayed indefinitely).

Does Your Health Plan Have a Grandfathered Status?

![]()

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio