Get Ready for 2018 Open Enrollment

ObamaCare’s open enrollment period for 2018 starts on November 1st, 2017 and ends on December 15th, 2017. This is what you need to know to enroll for 2018. Some states have longer enrollment periods, so you will have to check your state’s rules.

• Open enrollment is the only time you can get cost assistance, enroll in a plan, or change plans. This is true whether you shop inside or outside of the marketplace as all insurers in the individual and families market have adopted the marketplace’s enrollment period for major medical health plans.

• Don’t wait until the last minute to apply. This year’s open enrollment is shorter than last year’s. Almost all advertising and publicity funds were cut. Also, the website you will need to use, Healthcare.gov, has been scheduled to be out of service for “maintenance” during the busy Sunday sign-up hours. Also, the verification process can take more time than you expect. Please don’t put this off to the last minute.

• Get covered or switch plans by December 15th, 2017 to ensure your plan starts on January 1st, 2018 without a hitch.

• Other kinds of insurance like Medicare and employer-based insurance have unique enrollment periods.

• Cost assistance is based on income. If your income changes throughout the year report it to see if you qualify for further assistance and to prevent owing money at the end of the year.

• There are three ways to get cost assistance through the marketplace: Premium tax credits, cost-sharing subsidies, and Medicaid and CHIP.

• Premium tax credits for reduced premiums are offered to most people making less than 400% of the federal poverty level.

• Tax credits can be paid in part or whole to your insurer to reduce your premium or applied to your federal income taxes.

• Cost-sharing subsidies on out-of-pocket costs are offered to most people making less than 250% of the federal poverty level. To qualify for help on out-of-pocket costs you must enroll in a silver level plan.

• Medicaid and CHIP can be enrolled in at any time during the year, but if you want to use the marketplace to sign up you’ll have to do so during open enrollment.

• All insurance sold on the marketplace counts as minimum essential coverage and will protect you from the fee for not having coverage.

• The fee for not having coverage increases every year, so unless you qualify for an exemption, the chances that it is cheaper to pay the fee than to obtain coverage decreases every year. Note that fee collection may or may not be enforced by Trump.

• Anyone who has a marketplace plan from last year must log in and verify their plan and information for 2018 during open enrollment. This will ensure that you get the right plan and cost assistance amount.

• If you had a plan last year and didn’t verify your income and plan, you may be automatically re-enrolled in the plan and cost assistance or may be enrolled in a similar plan with similar cost assistance.

• If your income goes up and you don’t verify your information you could end up owing money at the end of the year.

• Anyone can sign up for ObamaCare’s marketplace, but if you have access to insurance through your employer, qualify for Medicaid, CHIP or Medicare, or make over 400% of the Federal Poverty Level you won’t have access to cost assistance

• Find out if you qualify for cost assistance here: https://www.healthcare.gov/lower-costs/qualifying-for-lower-costs/.

• Most young adults will qualify for free or low-cost coverage. Find out if you qualify by applying to the marketplace.

• Some young adults may qualify for catastrophic coverage which is inexpensive but has a high deductible and poor cost sharing.

• The cheapest plan isn’t always the best. When shopping for coverage remember that your goal is to make sure your medical needs are covered while saving as much on annual healthcare spending as possible. If you think you may need a lot of medical services and drugs, a higher premium plan could save you money in the long run.

• When it comes to comparing plans, you’ll need to understand the difference between an HMO and PPO, how out-of-pocket costs weigh against premiums, and what the plans network and drug formulary covers. Know what your projected medical needs are and how to understand the jargon before shopping for plans.

• Applying for the marketplace isn’t the same as enrolling in a plan. Feel free to sign up, see if you qualify for cost assistance, and shop for plans in your region before making your final choice.

How to Sign Up For The Health Insurance Marketplace

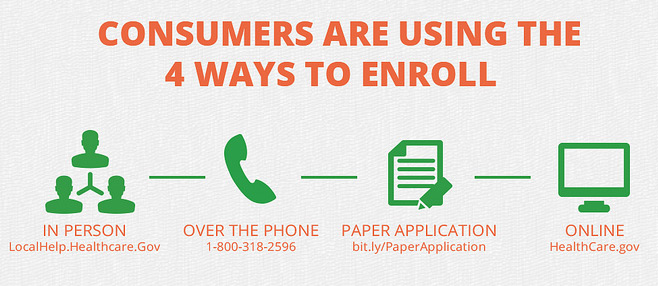

You can use your State’s health insurance marketplace to sign up for private insurance, get access to subsidies, or apply for Medicaid or CHIP, but there are four ways to apply including the website.

1) Find your State’s marketplace website.

2) Get help from a person. You can find in-person help by going toLocalHelp.Healthcare.gov.

3) Call the 24/7 marketplace helpline 1-800-318-2596.

4) Mail in a paper application. bit.ly/PaperApplication. (read these instructions first)

How to Enroll in a Health Insurance Marketplace Plan

Here are the official directions for enrolling in a marketplace plan through healthcare.gov. Remember signing up is only step one. You still need to choose a plan and make sure your first payment is made to have coverage officially. State-based marketplaces have similar sign-up and enrollment processes, the direction below are specifically for states using a federal-based marketplace (i.e., States using healthcare.gov as their marketplace).

- Set up an account. First, you’ll provide some basic information. Then choose a username, password, and security questions for added protection.

- Fill out the online application. You’ll provide information about you and your family, like income, household size, current health coverage information, and more. This will help the Marketplace find options that meet your needs. Important: If your household files more than one tax return, call the Marketplace Call Center at 1-800-318-2596 before you start an application.(TTY: 1-855-889-4325) This is a very important step. Please don’t skip it. Representatives can provide directions to make sure your application is processed correctly.

- Compare your options. You’ll be able to see all the options you qualify for, including private insurance plans and free and low-cost coverage through Medicaid and the Children’s Health Insurance Program (CHIP). The Marketplace will tell you if you qualify for lower costs on your monthly premiums and out-of-pocket costs on deductibles, copayments, and coinsurance. You’ll see details on costs and benefits to help you choose a plan that’s right for you.

- Enroll. After you choose a plan, you can enroll online and decide how you pay your premiums to your insurance company. If you or a member of your family qualify for Medicaid or CHIP, a representative will contact you to enroll. If you have any questions, there’s plenty of live and online help you can use.

For more details on signing up, you can check out our health insurance marketplace guide or find your State’s health insurance marketplace now to get started.

We hope this list helps get you started in open enrollment.

Batson Stevens, Jr.

where can we find what a family for three qualifies for in Texas, on tax credits?

ObamaCareFacts.com

The best thing to do is to start with HealthCare.Gov. https://www.healthcare.gov/contact-us/