ObamaCare: Health Insurance Cancellation

Why Was My Health Insurance Canceled?

Let’s clear the air about ObamaCare and health insurance cancellation. Many thought they could keep their plan, but found their health insurance policy canceled as of 2014. Others were able to keep their plan past 2014, but needed to or will need transition to another plan by 2017.

Let’s take a look at why many Americans are losing their policy, how ObamaCare played a part, what was done to fix this, and why it could be a good thing or bad thing for you depending on the situation.

Updates On Keeping a Canceled “Grandfathered” Plan

There were two major updates that changed how long people could keep plans canceled due to the Affordable Care Act moving into 2014.

UPDATE from December 2013: You can now keep your plan until 2015 (or renew your up until 2014 extending your coverage to 2015). This fix is dependent on your state and your insurer. Learn more about keeping your insurance under ObamaCare.

UPDATE March 2014: In some states you can renew your plan up until October 2016 as well (meaning you can keep your plan to 2017 by renewing it yearly through 2016).

Learn more about Grandfathered Health Plans (the plans you CAN keep) and the Health Insurance Marketplace (where you go to get a new plan if your health insurance policy was canceled.

ObamaCare Cancellation: “If You Like Your Plan You Can Keep it…”

Many Americans were under the impression that if, “they liked their health plan they could keep it. PEROID.” This is mainly due to a talking point that worked more like a half truth, than a whole truth.

The fact is the talking point should have read, “If you like your health plan, you can keep it… As long as it complies with the benefits, rights, and protections offered by the ACA or you were enrolled before the ACA went into effect on March 23, 2010. If your plan doesn’t comply with the ACA you’ll be asked to pick a new plan for 2014 and your old one will be canceled. In many cases you will find a more Affordable option in the health insurance marketplace due to subsidies. Even if you don’t find a cheaper plan, the quality of your health insurance will most likely be better.”

“The 17 million people who are covered in the individual health insurance market, where switching of plans and substantial changes in coverage are common, will receive the new protections of the Affordable Care Act sooner rather than later,” a press release from the time showed. “Roughly 40 percent to two-thirds of people in individual market policies normally change plans within a year. In the short run, individuals whose plan changes and is no longer grandfathered will gain access to free preventive services, protections against restricted annual limits, and patient protections such as improved access to emergency rooms.”

How Many People Lost Health Plans Under ObamaCare?

Going into ObamaCare’s first enrollment period in 2013 4.7 million of the 270 million Americans with health coverage lost plans. This group who lost their plans include about 1.4 million who qualified for free coverage from Medicaid and about 2.35 million who qualified for subsidies on the Marketplace. All Americans who had canceled plans qualified for a hardship exemption, meaning if they chose not to sign up they wouldn’t pay the fee for not having insurance in 2014. Others were able to keep their plan to additional years up to 2017.

Moving forward plan loss under the ACA is due to non-payment primarily. Some additional plan loss is due to folks missing opportunities to renew coverage. See ObamaCare enrollment numbers for details.

Why is New ObamaCare Coverage More Expensive?

Coverage is only more expensive in some regions, for some folks, who didn’t qualify for Marketplace cost assistance. Typically those who had high-end plans that excluded sick people saw the biggest rise in premiums. These premiums were being kept law artificially through exclusion or through lack of protections offered under the ACA (namely pre-existing conditions). It’s a myth that minor provisions like the required women’s services and child dental are the cause of premiums being raised by any substantial amount. See the discussion on ObamaCare insurance premiums and ObamaCare myths.

Guaranteed Issue and Ban on Rescission

Under the Affordable Care Act you cannot be denied coverage due to any reason other than your ability to pay, this is called guarantee issue. The ACA also includes provisions that ban rescission, meaning you cannot be dropped for any other reason other than failure to pay or fraud. Beyond that you can’t be charged a higher premium due to your health status and your health status can’t affect your ability to get or keep any health insurance covered by the Affordable Care Act. Please note that in some types of insurance, specifically supplemental health insurance options, don’t have to follow the same rules and regulations ACA compliant plans do.

ObamaCare makes it illegal for health insurance companies to arbitrarily cancel your health insurance just because you get sick.

ObamaCare Cancellation: What if My Old Plan Was Better Than The New Plan

Many people (who don’t qualify for subsidies on the health insurance marketplace) who have to switch of their old plan will find that they pay more for a new plan, sometimes these new plans have higher out-of-pocket costs or higher premiums and sometimes they have a more limited network. What isn’t being talked about as much is the fact that if they DO have to switch plans it means that their old plan was missing some basic protections that all plans now must include. This may not have been noticeable, but some of these protections are arguably priceless they are:

1. A Ban on denied treatment or coverage for preexisting conditions. You can’t be denied or dropped from coverage for being sick.

2. Ten Essential Health Benefits. Essential Health Benefits have no annual or lifetime dollar limits.

3. A Ban on rescission of health insurance coverage and the right to an appeal. You can’t be dropped for any reason other than fraud and if you are dropped you have the right to a quick internal and external appeal.

4. Ban on Discrimination based on gender or health. You can no longer be charged more for being a woman.

5. Ban on all lifetime limits and $2,000,000 Cap on annual limits. You are more protected from bankruptcy due to costly medical expenses.

6. Free Preventive Services and Wellness Visits.

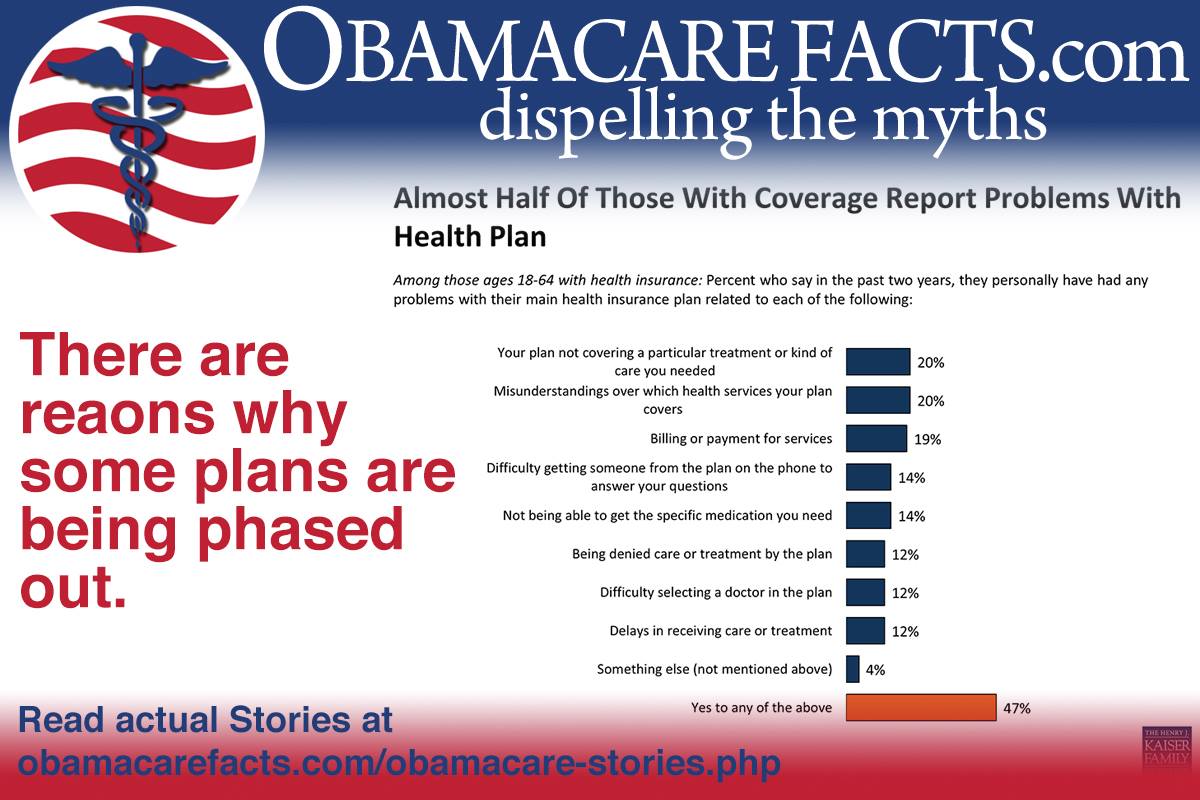

If your insurance was canceled then it wasn’t providing the above benefits, rights, and protections. It can be easy to say you would rather be paying less and not have those rights, but it’s important to imagine that one time that your insurance company refuses treatment. At the end of the day you are getting a better quality product, even if worst case scenario you are paying more for what seems like less.

Important Advice About Health Insurance Cancellations and ObamaCare

For at least 1/3 of Americans who have their health policy canceled their is good news, you’ll be able to find cheaper health insurance on the health insurance marketplace. Even if you don’t qualify for subsidies you should check out the marketplace to see the prices of plans in your area. Health insurers have to offer plans at the same price on and off the marketplace (however they don’t have to offer all their plans on the marketplace). In many cases your insurance company may not tell you about the marketplace. Make sure to check out the health insurance marketplace if your plan was canceled!

ObamaCare Cancellation

![]()

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio