ObamaCare Mandate: Exemption and Tax Penalty

The ObamaCare Mandate Exemption and How You Can Qualify for an Exemption from the Tax “Penalty.”

From 2014 – 2018, who chose not to purchase insurance had pay a tax “penalty” unless they qualified for an exemption. Exemptions from ObamaCare’s tax “penalty” mandate are available to a number of Americans.

We will cover all of the ObamaCare exemptions below, but first let’s take a quick look at common exemptions from the fee, how to avoid the fee, and what happens if you don’t get covered. If you just want the nuts and bolts, see our page on the 8965 exemptions form.

NOTE: Some states still have a state-based mandate. Please make sure your state doesn’t have a fee before deciding to go without coverage. If you do go without coverage in a state that has a fee, make sure you look into specific state based exemption rules. This page covers how the federal exemption worked from 2014 – 2018.

UPDATE: The exemption information on this page generally applies to each year, however 1. you should always check the most recent 8965 form for information (specific exemptions may change each year), and 2. starting in 2019 the fee for not having coverage is reduced to zero in most states (and thus an exemption is not otherwise needed in most states).

ACA exemptions for the 2018 plan year.

Short List of Common ObamaCare Exemptions

Here are common ObamaCare exemptions from the fee claimed on the 8965 exemptions form:

- You got covered during open enrollment either inside or outside the Marketplace

- You went less than three months without coverage

- You don’t have to file taxes because your income is below the tax filing threshold

- Coverage would cost more than ~8 of household income per person (adjusted for inflation each year) <—– the specific number is subject to change each year; for example 8.13% was the figure for 2016.

- You got denied Medicaid or CHIP (your state didn’t expand Medicaid, and you made 138% FPL or less)

You don’t owe the fee for any month that you have an exemption for. There are many more exemptions than the ones above. See our full list of regular exemptions and hardship exemptions below or see the image below for a quick visual.

- Open enrollment ends Dec 15 each year. Before you look into exemptions, look into Special Enrollment Options. You may still qualify for Medicaid, CHIP, or another option that helps you to avoid the fee!

- The annual fee for not having insurance in 2018 is $695 per adult and $347.50 per child (up to $2,085 for a family), or it’s 2.5% of your household income above the tax return filing threshold for your filing status – whichever is greater. You’ll pay 1/12 of the total fee for each full month in which a family member went without coverage or an exemption.

NOTE: The fee is subject to inflation.

FACT: The fee is sometimes called a penalty, fine, or Individual Shared Responsibly Payment. It is part of the Individual Shared Responsibility Provision, which is often called the Individual Mandate. On this page, we’ll discuss exemptions from the mandate’s requirement to obtain coverage or pay a fee.Avoiding the ObamaCare Fee

Although the fee is $0 in most states moving forward, the information below is still relevant to past years and in states with their own mandate.

The Individual Mandate (AKA the Individual Shared Responsibility Provision) is the part of the Affordable Care Act. It says that you must obtain and maintain minimum essential coverage throughout the year, get an exemption, or pay a fee on your Federal Income Taxes for each month you (or your dependents) go without coverage.

To avoid the penalty, you must obtain minimum essential coverage and maintain it throughout the year or get an exemption. Make sure you and your dependents are covered during your health plan type’s open enrollment period. Most health plans sold outside of open enrollment do not count as minimum essential coverage (the type of coverage you need to avoid the per month fee). The only way around this is to qualify for either special enrollment or another type of insurance such as Medicaid or CHIP.

How to Qualify For An Exemption

The easiest way to qualify for an exemption is to go to HealthCare.Gov and sign up for a marketplace account. When you sign up, you automatically find out if you qualify for some exemptions, and you might discover that you qualify for lower costs on coverage. You may even qualify to shop for a catastrophic plan with lower premiums if you obtain a Hardship Exemption.

Other exemptions must be claimed on your 1040 Federal income tax return using the ObamaCare exemptions form 8965. Although you don’t have to apply for some exemptions, it’s smart to check with the marketplace because many exemptions also trigger special enrollment periods allowing you more coverage options.

If you plan on applying for an exemption, don’t leave it to the last minute. In many cases, you’ll have to fill out a form and wait for confirmation before you can report the exemption. In addition, many exemptions require specific documentation to verify your eligibility. Obtaining the necessary documentation also takes time. Waiting can mean a delay of your Federal Tax Refund.

- Apply for exemptions at HealthCare.Gov.

- There are about 20 different exemptions including hardship exemptions. Some exemptions require documentation. Some don’t.

- Many exemptions require an Electronic Confirmation Number (ECN). If you don’t have yours in time, just report “PENDING” instead of the exemption code.

- Some exemptions only last 3 months; others last a calendar year.

- Some exemptions will qualify you for a catastrophic health plan and a special enrollment period; some will just help you avoid the fee.

- Some exemptions don’t require you to apply or qualify beforehand and can simply be claimed on your 1040.

There are many exemptions from the fee and, according to the CBO, as many as 26 million Americans will qualify for one. Look below to see if you qualify for an exemption from the tax penalty on your yearly Federal Income Taxes.

FACT: If you are over 30, only a Hardship Exemption will qualify you to shop for catastrophic coverage and not pay the fee. Other exemptions would free you from paying the penalty, but they would not qualify you to purchase a low-premium catastrophic health plan.

Reporting Exemptions to the IRS

To report an exemption to the IRS, you’ll use Form 8965, Health Coverage Exemptions (see an example from Exemption instructions below). Some exemptions require you to report Electronic Confirmation Numbers sent by the Marketplace upon approval of your exemption application. You’ll attach that form to your 1040 when you file your taxes. Learn more about filing taxes for ObamaCare.

How Much is the ObamaCare Fee?

The fee for not having insurance increases each year.

For the 2014 tax season, the Individual Shared Responsibility fee for not having insurance was $95 per adult and $47.50 per child (up to $285 for a family) or 1% of your income – whichever was greater. The monthly fee is 1/12 of the total fee for each month you don’t have coverage or an exemption. See Individual mandate for more details on the fee.

In 2015, the Individual Shared Responsibility fee for not having insurance was $325 per adult and $162.50 per child (up to $975 for a family) or 2% of your taxable income – whichever is greater. The monthly fee is 1/12 of the total fee for each month you don’t have coverage or an exemption. See Individual mandate for more details on the fee.

For 2016 – 2018 (and generally beyond; although it is subject to change), the Individual Shared Responsibility fee for not having insurance is $695 per adult and $347.50 per child (up to $2,085 for a family). Alternately, it’s 2.5% of your household income above the tax return filing threshold for your filing status. The amount you owe would be whichever of these amounts is greater. You’ll pay 1/12 of the total fee for each full month in which a family member went without coverage or an exemption.

The fee increases each year until it ends up being about the price of getting the cheapest health plan. Find out how the fee works moving forward.

What Happens if I’m Not Exempt From ObamaCare and Don’t Pay the Fee

If you decide not to get coverage and don’t qualify for an exemption, then you’ll have to make an Individual Shared Responsibility payment on your income tax return for each month you went without minimum essential coverage.

Can I Go to Jail for Not Paying the Fee?

The IRS cannot enforce the Individual Shared Responsibility Provision with jail time, liens, or any other of typical methods of collection. The only way for the IRS to collect the fee for not having health insurance, if you choose not to pay it, is for them to withhold the money you would get back from your Federal Income Tax Refund from the IRS after you file your income tax return.

How Do I File my Taxes for the Fee?

You’ll get a 1095-A, 1095-B, or 1095-C form from your insurer about which months you had coverage. You’ll use this to file your taxes. If you had an exemption for one or more months, you might need an ECN number provided by the Health Insurance Marketplace. Find out details on how you file taxes for ObamaCare by checking out our pages on filing taxes under the Affordable Care Act.

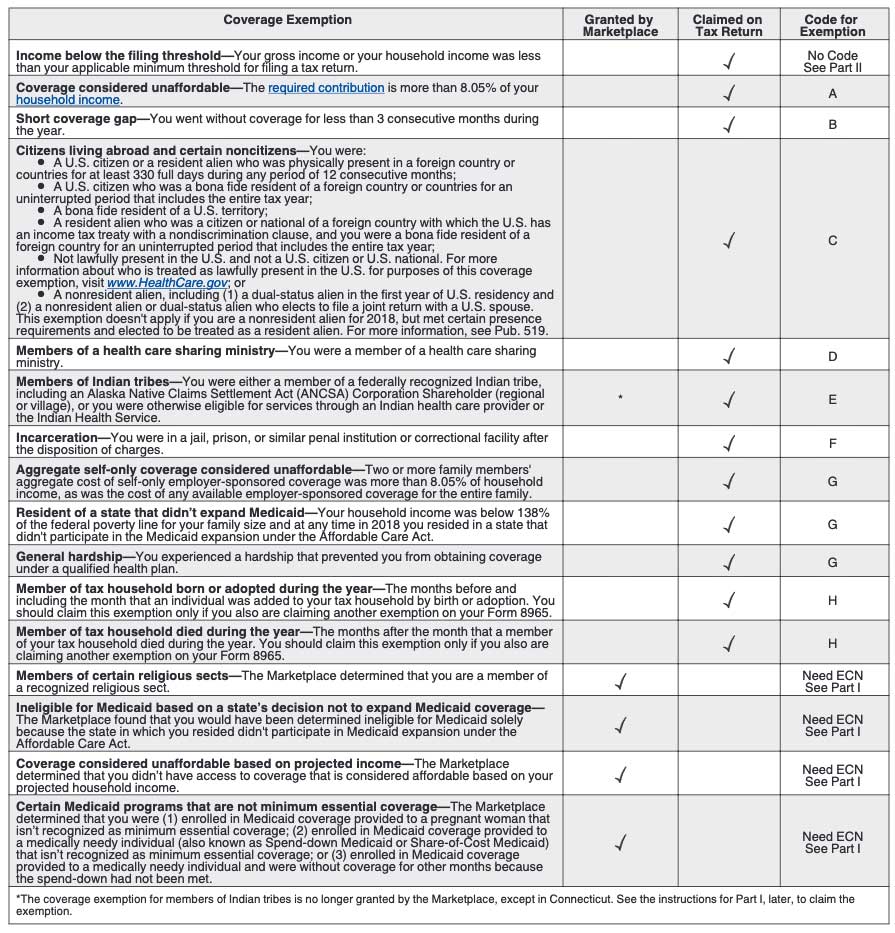

Full List of ObamaCare Exemptions

TIP: Some specifics below are subject to change each year. Make sure to check out the latest 8965 form for the current figures.

The mandate’s exemptions cover many individuals including members of certain religious groups and Native American tribes, undocumented immigrants (who are not eligible for health insurance subsidies under the law), and incarcerated individuals. People whose incomes are so low they don’t have to file taxes (in 2014, it’s $10,150 for an individual or $20,300 for a married couple) are also exempt. People for whom health insurance is considered unaffordable due to insurance premiums after employer contributions or federal subsidies exceeding the limits of family income are also exempt, as are those going without insurance for less than three months in a row.

NOTE: Some exemptions exempt you for up to three months, and others exempt you for the calendar year. You won’t owe the fee for months you have an exemption for. However, the goal isn’t to simply go without coverage or the fee. Some exemptions (mainly hardship exemptions) will not only exempt you from owing the fee but will also qualify you for special enrollment, thereby allowing you to get medical insurance outside of open enrollment. Make sure to apply for exemptions at HealthCare.Gov as many exemptions require an Electronic Confirmation Number (ECN).

If you belong to any of the groups listed below, you are exempt from ObamaCare’s mandate to “obtain minimum essential coverage” (i.e. buy insurance):

• Unaffordable Coverage Options- People who would have to pay more than 8% of their household income (MAGI) for the lowest priced Marketplace Health Insurance after subsidies qualify for this exemption. If your employer insurance is unaffordable, costing more than 9.5% MAGI after employer contributions for employee-only coverage, you will probably qualify for this exemption (an aggregate cost of 8% for households qualifies for a Hardship Exemption). You must apply for this exemption. Remember that your MAGI is not the same as your taxable income; it includes the amounts you invested into non-taxable savings accounts, income from Social Security, and educational expenses.

NOTE: If your employer’s coverage is considered affordable (less than 9.5% of your household income), you will not qualify for an exemption from the fee yourself, but your uninsured dependents could still qualify. The fee is 1/12 the fee per month for each family member without coverage.

• Low Income/No Filing Requirement- People with incomes below the IRS threshold required for filing taxes (in 2013, $10,000 for a single person and $20,000 for a married couple) are exempt. This exemption is automatic.

• Hardship Exemption- This applies when the Health Insurance Marketplace, also known as the Affordable Insurance Exchange, has certified that you have suffered a hardship that makes you unable to obtain coverage for valid reasons, financial or otherwise. There are many situations that will qualify you for a hardship exemption, so please see below for the full list. If you wanted to buy health insurance but were unable to do so because of hardship, you qualify. All you need to do is apply and provide documentation of your hardship.

NOTE: If your plan was canceled or became unaffordable in 2014 because of the Affordable Care Act, you qualify for a hardship exemption in 2014 only and were not required to obtain coverage for 2014.

• Short Coverage Gap Exemption– If you go without coverage for less than three consecutive months during the year, you will not be responsible for the fee for those months. This allows folks who have had coverage throughout the year to take some downtime between insurance options when they experience a life change such as moving or switching jobs. The coverage gap doesn’t apply if you don’t get covered; if you have more than one gap, it only applies to the first gap of fewer than three months. It can be paired with other exemptions.

• Exemption for Getting Covered During Open Enrollment- Aside from the “short coverage gap” exemption there was another important coverage gap exemption that applied to those who purchased marketplace (or non-marketplace) insurance between March 15th and April 15th, 2014 (that coverage didn’t start until May 1st, 2014). This allowed for an extra full month without coverage or responsibility for the penalty in 2014. This exemption can be found on the 8965 form as “gap in coverage at the beginning of 2014.” This coverage gap is separate from the “less than three-month” coverage gap exemption. We assume there will be another similar exemption in the future for anyone who got coverage by February 15th, although the ongoing “short coverage gap” exemption may suffice. We will update once the 2015 exemption forms are created. If you got covered during open enrollment use this exemption and not the short coverage gap exemption.

NOTE: You only need an exemption for “full months” you go without coverage. Coverage for even one day in a month counts as being covered.

• Religious Conscience- People can qualify for religious exemptions. The Social Security Administration administers the process for recognizing these sects according to the criteria in the law.

• Health Care Sharing Ministry- If you are a member of a recognized health care sharing ministry, you qualify for an exemption. Find out more about how Health Care Sharing Ministry exemptions work.

• Not lawfully present- If you are an undocumented immigrant, or you are not legally a U.S. citizen, a U.S. national, or an alien lawfully present in the U.S., you are exempt.

• Incarceration- People who are incarcerated are exempt.

• Indian tribes- Members of a federally recognized Indian tribe are exempt.

For those who can afford it and choose not to purchase health insurance, the tax will be unavoidable. The money collected from these taxes goes towards funding ObamaCare and subsidizing hospitals, which will have to cover unpaid emergency room visits. The money is also a down payment on your almost inevitable use of the health care system.

NOTE: ObamaCareFacts.com is a free informational website, nothing on our site should be taken as legal advice. Check out the official IRS website on exemptions and the Individual mandate for additional details.

ObamaCare Hardship Exemptions

ObamaCare’s hardship exemptions apply to those who have found themselves in certain life circumstances that qualify as “hardships.” There are many things that will qualify you for a hardship exemption, but in simple terms: If you wanted to buy health insurance and were unable to do so because of a life circumstance or financial situation, then you probably qualify for a hardship exemption.

If any of the following circumstances apply to you, you may qualify for a hardship exemption from the shared responsibility penalty, and you may qualify for a catastrophic plan, and/or you may qualify for a special enrollment period. Not all exemptions last for a full calendar year. In most cases, you’ll need to submit documentation to be granted an exemption.

Information below obtained from HealthCare.Gov

ObamaCare Hardship Categories and DocumentationYou may qualify for a hardship exemption if you experienced one of the following: |

||

| Hardship number | Category | Submit this documentation with your application |

| 1. | You were homeless. | None |

| 2. | You were evicted in the past 6 months or were facing eviction or foreclosure. | Copy of eviction or foreclosure notice |

| 3. | You received a shut-off notice from a utility company. | Copy of shut-off notice from a utility company |

| 4. | You recently experienced domestic violence. | None |

| 5. | You recently experienced the death of a close family member. | Copy of death certificate, copy of death notice from newspaper, or copy of other official notice of death |

| 6. | You experienced a fire, flood, or other natural human-caused disaster that caused substantial damage to your property. | Copy of police or fire report, insurance claim, or another document from government agency, private entity, or news source documenting event |

| 7. | You filed for bankruptcy in the last 6 months | Copy of bankruptcy filing |

| 8. | You had medical expenses you couldn’t pay in the last 24 months. | Copies of medical bills |

| 9. | You experienced unexpected increases in necessary expenses due to caring for an ill, disabled, or aging family member. | Copies of receipts related to care |

| 10. | You expect to claim a child as a tax dependent who’s been denied coverage in Medicaid and the Children’s Health Insurance Program (CHIP), and another person is required by court order to give medical support to the child. | Copy of medical support order AND copies of eligibility notices for Medicaid and CHIP showing that the child has been denied coverage |

| 11. | As a result of an eligibility appeals decision, you’re eligible either for 1) enrollment in a qualified health plan (QHP) through the Marketplace, 2) lower costs on your monthly premiums, or 3) cost-sharing reductions for a time when you weren’t enrolled in a QHP through the Marketplace. | Copy of notice of appeals decision |

| 12. | You were determined ineligible for Medicaid because your state didn’t expand eligibility for Medicaid under the Affordable Care Act. | Copy of notice of denial of eligibility for Medicaid |

| 13. | You received a notice saying that your current health insurance plan is being canceled, and you consider the other available plans to be unaffordable. | Copy of notice of cancellation |

| 14. | You experienced another hardship in obtaining health insurance. | Please submit documentation if possible |

| NEED HELP WITH YOUR APPLICATION? Visit HealthCare.gov or call them at 1-800-318-2596. Para obtener una copia de este formulario en Español, llame 1-800-318-2596. If you need help in a language other than English, call 1-800-318-2596 and tell the customer service representative the language you need. We’ll get you help at no cost to you. TTY users should call 1-855-889-4325. | ||

Other Hardship Exemptions

Beyond the hardship exemptions above there are three other exemptions (2 of which are unique to 2014).

- Two or more family members’ aggregate cost of self-only employer-sponsored coverage is more than 8% of household income, as is the cost of any available employer-sponsored coverage for the entire family.

- You purchased insurance through the Marketplace during the initial enrollment period but have a coverage gap at the beginning of 2014.

- You applied for CHIP coverage during the initial open enrollment period and were found eligible for CHIP based on that application but have a coverage gap at the beginning of 2014.

- You were engaged in service in AmeriCorps State and National, VISTA, or NCCC programs and were covered by short-term duration coverage or self-funded coverage provided by these programs.

- You were eligible but did not purchase, coverage under an employer plan with a plan year that started in 2013 and ended in 2014. (Available only in 2014.)

- You were enrolled in certain types of Medicaid and TRICARE programs that are not minimum essential coverage. (Available only in 2014.)

- You had some specific types of limited benefit coverage. These are mostly limited-benefit Medicaid or TRICARE plans. See IRS Notice 2014-10. Further details can be found on the 8965 Form. (Available only in 2014.)

The Medicaid Exemption and Special Enrollment Period

Applying for Medicaid or CHIP and being rejected can grant you not only an exemption but also a special enrollment period. You’ll need to have your rejection letter as proof to qualify for either.

Exemptions for Citizens Living Abroad

You are exempt if you were:

- A U.S. citizen or resident who spent at least 330 full days outside of the U.S. during a 12-month period; A U.S. citizen who was a bona fide resident of a foreign country or U.S. territory;

- A resident alien who was a citizen of a foreign country with which the U.S. has an income tax treaty with a nondiscrimination clause, and you were a bona fide resident of a foreign country for the tax year;

- or Not a U.S. citizen, not a U.S. national, and not an individual lawfully present in the U.S. For more information about who is treated as lawfully present for purposes of this coverage exemption, visit healthcare.gov.

Applying for Exemptions

You can learn about applying for exemptions here. In some cases, you’ll need to fill out a form and send it to the marketplace before you officially qualify for the exemption. Don’t leave this until the last minute.

Applying for a Hardship Exemption

To apply for a hardship exemption, you can fill out the exemption form: Individuals who experience hardships (PDF). See instructions to help you fill out an exemption application (PDF).

You should apply for hardship exemptions early – you need to get approved first and then wait for confirmation to be mailed to you. You’ll get a unique exemption certificate number (ECN) that can be used to qualify to shop for catastrophic coverage or can be used to confirm exemption when filing your taxes.

Learn more about hardship exemptions for Healthcare.Gov.

NOTE: If you qualify for a hardship exemption, you’ll also qualify for a catastrophic plan. Catastrophic plans are high-deductible plans with low premiums. Since all plans cover essential benefits, it’s a great alternative to going without coverage – even if you have an exemption.

How Long Do ObamaCare’s Exemptions and Hardship Exemptions Last?

Most hardship exemptions start the month before the hardship, continue through the month of, and finish with the month after. Some hardship exemptions and other non-hardship exemptions last a full calendar year (which typically ends December 31st).

This means that, while some exemptions will help you avoid a few months of the per-month fee, most are meant to qualify you for special enrollment rather than simply exempting you from the fee.

- Affordability hardship exemptions are granted for the remaining months of the calendar year.

- Hardship exemptions due Medicaid ineligibility (when your state hasn’t expanded Medicaid) are granted for the remaining months of the calendar year.

- For people eligible for Indian Health Services, the hardship exemption will be granted on a continuing basis. It may be kept for future years without its recipient having to submit another application. This is true as long as there are no changes to your membership in a tribe or eligibility for services from an Indian health care provider.

Proof of ObamaCare Exemption

Most exemptions will require documentation as listed above. If you cannot provide documentation, you may still qualify for certain exemptions (for example, the homelessness exemption). The safest way to avoid the fee is simply to obtain health insurance. Some exemptions will buy you more time to sign up, and these tend to be the ones with more flexible requirements of proof. Other exemptions simply allow you not to pay the tax, and these tend to require proof.

What Types of Insurance Will Help Me Avoid the Fee?

To avoid the fee, you’ll need to obtain minimum essential coverage. Most private health insurance options, Medicare, Medicaid, CHIP, TRICARE, and all insurance sold on the marketplace will count as minimum essential coverage. Also, people under 30 and those with hardship exemptions qualify to purchase a catastrophic plan, which is also minimum essential coverage.

Most kinds of insurance offered between each open enrollment period will be short term health insurance. Fixed benefit plans and supplemental insurance will not help you avoid the fee on their own, but they will help you be covered and able to pay for catastrophic medical bills. Also, having one of these types of insurance doesn’t prevent you from qualifying for an exemption or hardship exemption to avoid the fee.

Not sure if your plan will help you avoid the fee? Simply ask your insurer, “is your plan ACA compliant” or “does it counts as minimum essential coverage?” Most kinds of major medical insurance count.

Important Exemptions to Understand

Two of the more important exemptions discussed above are the “Short Coverage Gap Exemption,” and the “Hardship Exemptions” for things like a plan that canceled or a state did not expand Medicaid. Let’s look at these in more detail:

Short Coverage Gap Exemption and Open Enrollment Exemption

The Short Coverage Gap Exemption allows you less than three full, consecutive months without coverage.

In 2014, Americans had until March 31st, 2014 to enroll in a marketplace plan and still avoid the fee. So, if you enrolled on March 31st and had coverage that started on May 1st, 2014, you still would have avoided paying the Individual Shared Responsibility payment. As a rule of thumb, if you sign up during open enrollment, you avoid the fee. The exemption for signing up during open enrollment is claimed on the exemptions form.

If you (and your dependents) get covered during open enrollment and maintain coverage all year, you won’t owe the fee. This is true even when open enrollment is officially extended (as it was in 2014).

NOTE: The gap is less than three months – not exactly three months. You’ll need at least one day of coverage in the third month.

ObamaCare Hardship Exemption Extension for Canceled Plans

On December 20th, 2013, Health and Human Services (HHS) announced that the “hardship exemption” will exempt anyone who had his or her plan canceled due to the Affordable Care Act. These Americans will still be able to buy insurance and use subsidies, but they will not be responsible for the fee for going without coverage in 2014. Since they will now qualify for a hardship exemption, they will also be eligible to buy a catastrophic plan outside the Marketplace. A catastrophic plan provides minimum essential benefits with high out-of-pocket costs, but very low premiums. We at ObamaCareFacts.com suggest, as always, that you buy the plan that is right for you and your family. For most people, that plan is a silver level or higher that comes with reasonable deductibles, affordable out-of-pocket costs, and a solid insurer network.

UPDATE Canceled Plan Hardship Exemption: If you had your plan canceled due to the Affordable Care Act (your insurance company would have notified you of this) you are exempt from the mandate to buy insurance in 2014 and 2015. Also, if your state and insurance company allow you to, you can renew a canceled plan until October 2016. Even if you have an exemption due to a canceled plan, you can still use the marketplace to get coverage. You will qualify to shop for a low premium, high out-of-pocket catastrophic plan outside the Health Insurance Marketplace.

ObamaCare Hardship Exemption Extension for People Living in States where Medicaid was not Expanded.

If you live in a state that did not expand Medicaid, you qualify for this hardship exemption. This one is a bit tricky, though; you must apply for Medicaid in your state and be denied. Your “denial of eligibility” letter is the documentation you must send with your hardship exemption application. Essentially, if your state is refusing to accept the tax money that, had they expanded Medicaid, would have been available them, then you are not required to pay the tax. The reason this is a hardship exemption is that you could have had health insurance free of charge if your state had expanded Medicaid. In states that did expand Medicaid, people who make less than 138% the Federal Poverty Level will qualify for Medicaid Coverage.

How the ObamaCare Mandate Works

Americans who can afford to purchase insurance, but choose not to do so, will have to pay an income tax “penalty”. This is officially a tax, but is also referred to as a “fee,” “penalty,” or “mandate.” The way the ObamaCare mandate works is that any non-exempt American without minimum essential coverage will owe a per-month fee. The fee is $325 per adult and $162.50 per child (up to $975 for a family) or 2% of your taxable income a year. The monthly fee is 1/12 of the total annual fee (example: $325/12= $27.08 per month). The total penalty amount cannot exceed the national average of the annual premiums of a “bronze level” health insurance plan on ObamaCare exchanges.

The fee is a per-month fee for every month you go uninsured. You have a “Short Coverage Gap” exemption, so you can go without minimum essential coverage for less than 3 months in a year without owing the fee.

The actual rules are a little more complicated — they depend on a number of factors such as the ages of dependents and income. We suggested learning more about the specifics of how the Individual Mandate works if you plan to go without health insurance.

When Does the New ObamaCare Tax “Penalty” Come into Effect?

The fee for not complying with the ObamaCare Mandate began to be required on your 2014 Federal Tax Returns. The Health Insurance Marketplace sells plans that will help you avoid the fee and may offer you lower costs on coverage, so we suggest shopping there. Getting covered during the annual open enrollment period will ensure that you avoid paying the tax. Remember that each kind of insurance has their own open enrollment period. Make sure you understand the health insurance marketplace deadlines to be sure you get a plan during open enrollment unless you qualify for an exemption from ObamaCare’s tax penalty.

How You Can Qualify for an Exemption from the Tax “Penalty.”

![]()

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio