Nearly Everyone’s Healthcare Coverage is Heavily Taxpayer Subsidized

Ads by +HealthNetwork

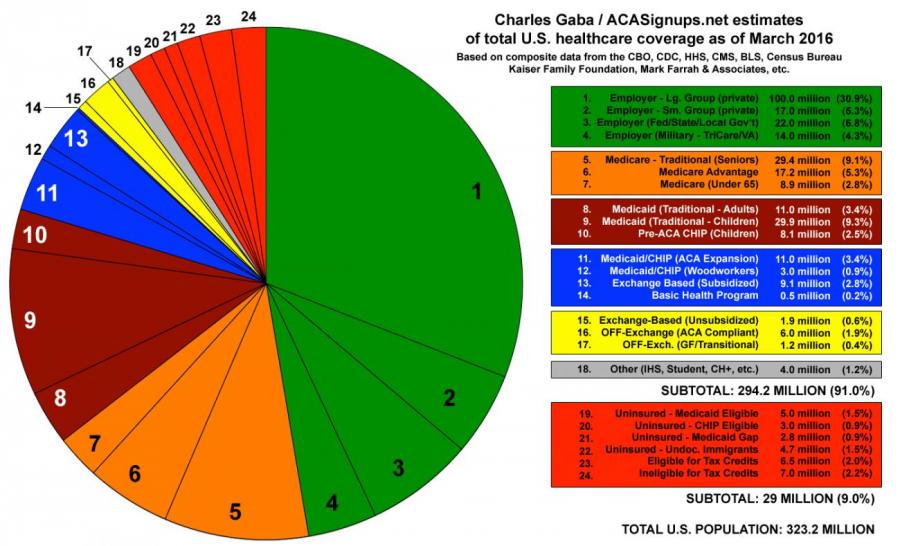

Nearly everyone’s health coverage is highly subsidized (via tax breaks, if not credits). The group that costs tax payers the most money in healthcare is employees.