5 Years of the Affordable Care Act In Retrospect

The Affordable Care Act (ObamaCare) was signed into law 5 years ago on March 23rd, 2010. We look at the successes, sticking points, and politics of the law.

Here are a few facts about the ACA, ObamaCare and how it’s working:

First and foremost the ACA or ObamaCare is seen as “BIG Government” by Many Conservatives: This is probably the most important thing for the average American to understand. Facts aside, no matter what Medicaid, Medicare, Social Security, the Affordable Care Act and other federal “social safety net programs” accomplish (or don’t accomplish) they will always be “BIG government.” That means they will always be seen a matter for the state and not Uncle Sam.

To the modern Conservative (not the traditional Washington Republican) government spending, taxation, and regulation are not American and therefore Federal social safety programs can never be accepted ideologically. The argument is emotional and ideological, there is little room to debate the facts (of course, to be fair, this can often be true of modern Liberals too).

Social Safety net programs and other social reforms taken on a federal level, whether it is the New Deal, the Great Society Programs, or “President Obama’s change-o-rama” (do we have a name for this?) are the red-headed-step-children of America. Each was passed by a Liberal with a massive push-back from the right.

The modern tea-party-Reagan-Goldwater Conservative will never say, “hey guys, it turns out those programs are working.” They will always find counterpoints to prove, “big government is wrong, we should let states decide.” Even if they were to admit a program was working or protection was needed (like segregation for example) ideology would still force their hand to declare it was a matter of state’s rights and not the job of big government. We know this, because we had video cameras in the 60’s.

Lastly this author would like to note that while Congress may be fighting an ideological battle, for most of the other 320,000 million Americans, THIS IS ABOUT HEALTHCARE. Politics aside, people just want to be able to take care of their families. Don’t lose sight of the fact that individual liberty depends upon a person’s ability to contribute to society. And a person’s ability to contribute to society depends upon things like health, education, food, and housing.

Anyway, all that aside, the facts we have say the PPACA is workin and they also say the PPACA includes some spending, more bureaucracy, and a few missteps. Here is the breakdown.

ObamaCare is working for the middle class: 16.4 million enrolled in the Marketplace or have stayed on their parents private health plan.

The safety net is stronger: Medicare’s solvency is increased and 10.8 million have enrolled in Medicaid or CHIP since October 2013. In-part due to Medicaid expansion.

Consumer’s are protected: No more pre-existing conditions, no more lifetime limits, better access to wellness and prevention.

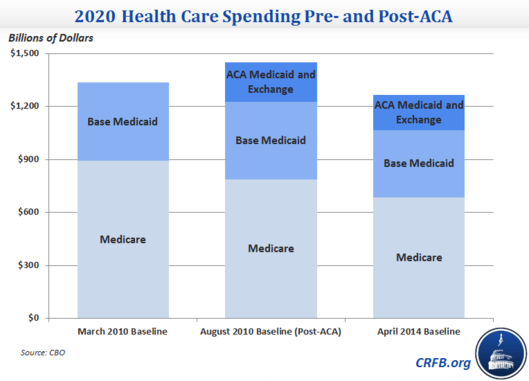

Costs are being curbed: Despite a massive, but lower $1.207 net price-tag, In 2014 health care spending grew at the slowest rate on record (since 1960). Meanwhile, health care price inflation is at its lowest rate in 50 years. Unpaid medical bills are even down by about 20%. Higher out-of-pocket costs, while not very attractive on the surface, have helped to keep premium costs affordable and have the ancillary effect of bringing consumer healthcare prices and long term premiums down by incentivizing people to shop around for healthcare.

Some people are paying more or have a bad taste in their mouths: Whether it was a healthy person’s health insurance premium going up, a MIA 1095-A, or no-one explaining that “if you like your plan you can keep it” applied more to the ban on rescission then to a mandate to force insurers to offer plans, not everyone had an “everything is awesome” experience.

The other 750 pages: All of the above is contained within a few specific sections of the law. Mainly the first two titles. The other 8 titles tend to go un-talked about. You can read them for yourself using our PPACA provision summary. Go ahead and skip to title III. Tell me with a straight face that you knew any of this was actually in the law. Next time you hear about cost curbing measures and healthcare reform, remember some of us are referring to the whole law not just the concept of “big government spending”.

Title I Quality, affordable health care for all Americans <—–Everything you hear about on the Media

Title II The role of public programs <——Medicare and Medicaid reform

…. Everything else you rarely hear about from value based quality over quantity, other Medicare reforms, tons of hospital reforms, a focus on transparency and technology, spending, other revenue measures, and generally reforms that have been a long time coming. Do a quick skim through of our PPACA provision summary for yourself it takes less than 5 minutes.

Title III Improving the quality and efficiency of health care

Title IV Preventing chronic disease and improving public health

Title V Health care workforce

Title VI Transparency and program integrity

Title VII Improving access to innovative medical therapies

Title VIII Community living assistance services and supports

Title VIIII Revenue provisions

Title X Reauthorization of the Indian Health Care Improvement Act

Just remember, repealing the Affordable Care Act means repealing ten titles. It goes beyond political ideology and starts really affecting peoples lives. The next hurdle is King V. Burwell, but it won’t be the last. Careful what you wish for America.

Find out more about how the Affordable Care Act is working.

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio

Marcus

As far as the ACA, it’s basically a patch job lobbyist compromise that was passed to assist more people with acquiring health insurance. It provides tax incentives and competitive rates for large and small businesses (tax credits & exchange pools).

It expanded Medicaid (optional to the SCOTUS first ruling) and allows state/Federal, state or just Federal Exchanges to be available so consumers can view competing private insurance companies and make a decision. Depending on their income, they can get a subsidy and if they are 101%-250% of the FPL, they’ll be eligible for Cost Sharing Reduction Caps on the benefits so their out of pocket expenses would be lower. To simplify for others, co-pays, deductibles and max-out-of-pocket will be lowered. You can get also get plans off-exchange directly through the insurer but without subsidies or CSR eligibility. No one can be turned down, eliminates annual and lifetime benefits maximums and every plan has 10 mandatory Essential health benefits (preventative care, Rx coverage, etc – list provided on this site).

Though I have my criticisms of the ACA, all of these benefits didn’t exist before the law. There are also other benefits as well like the fact the Max-out-of-Pocket amount is regulated by the government. Plans prior to the ACA were cheaper if you weren’t denied but what people are so quick to forget is that they came with higher deductibles in a lot of cases because that was the way to fix a increasing premium… increase the deductible. Recissions existed as well… when they could find some discrepancy on your mortgage long application where you had to remember ANYTHING of medical concerns so they can terminate the contract. Lifetime caps on benefit payouts existed so they could halt claims payments and you’d have to search the market again for anyone who’d “happily” take costly client. You possibly could find coverage if your state had a High Risk Insurance Pool or Pre-Existing Insurance Pool option but after the proving denial and seeing if you can pay the high premiums in the high risk pool, a lot of people may not have been able to afford it. The system wasn’t perfect before but it’s definitely better now and that’s why a lot more people have gotten insurance.

If you’re foolish enough to be mad it’s still not as affordable but believe in the free market approach, you’re literally drinking some contaminated Kool-Aid and refuse to believe in facts. Or, you’re a watching contradiction and want Single-Payer or Medicare-For-All because realistically, that’s the cheapest way to go. Healthcare Triage and just reading about that system will educate you more on other models for healthcare. I work and profit from the current system and the system before so I grudgingly say the government run approach is more efficient but facts are pretty damn stubborn. Hopefully everyone just tries to stay informed and thanks Obamacarefacts for providing this easy to understand source.

ObamaCareFacts.comThe Author

Thanks for the good explainer and kind words.

t

You need to be far more honest and transparent about the effects of this law on families at the top or just outside the subsidy. We don’t have a “bad taste in our mouth”, we are vomiting from cost – we are being financially destroyed and your people either just won’t hear it, seem to not believe it and continually cast families like ours in a very condescending light, like we “have a bad taste in our moth”. No, we are trying to figure out how to buy the next car when this 15 year old one dies. We are trying to figure out how to save for retirement when we have no more disposable income. We are trying to decide if we should actually go to the doctor because even though we are paying $1,500 per month our deductible is 3K so nothing is ever covered when we are sick. And those free check-ups? they are only free until they find something. “Think” they see something in the mammogram? Oh, now its a diagnostic test and you have to pay full cost for something you were told was free. It’s all just a giant dirty trick to families like mine. Please, hear us. Do not reject us. We are a political inconvenient, but we are the people too.

ObamaCareFacts.comThe Author

I get it. I personally have been hearing people’s comments since 2012 when I started this site (this independent non-government site where we can all share feeling and ideas on the ACA). I talk to a lot of people in different income brackets. Some people are in that sweet spot where cost assistance isn’t there or is just capping them at the 9.5%, some people who don’t have coverage because they were rejected Medicaid by their states refusal of expanding under the ACA, some people who struggle with costs due to debt and mortgages and child care. Your pain is felt and shared and you aren’t being dismissed. I think people underestimate how expensive the healthcare system is for everyone, including the government.

This is not “a dirty trick” this is step one toward us figuring out our healthcare issues. The more we come together the more pressure we put on the politicians and industry and the faster it gets done.