Open Enrollment 2016, Rate Increases, and the Medicaid Gap

For 2016 Millions will get coverage, and cost assistance will help ease the impact of rate hikes, yet millions will be left uncovered due to the Medicaid gap.

Let’s take a quick look at 2016 coverage, rate increases, the Medicaid gap, and how this will all affect enrollment numbers and opinions of the ACA in 2016.

Last Week Tonight with John Oliver: Medicaid Gap (HBO). Watch John Oliver explain the Medicaid Gap in a fun “more watch-y, less read-y, albeit slightly NSFW way”.- Open enrollment 2016 goes from November 1st, 2015 to January 31st, 2016. During this time people can renew plans, adjust cost assistance, and enroll in new plans too.

- Anyone who misses open enrollment will have limited options for private coverage in 2016 and will owe the fee for each month they go without coverage or an exemption.

- All Americans who make between 100% – 400% of the poverty level can get cost assistance on coverage.

- Cost assistance caps the amount you can spend on premiums and out-of-pocket costs, ensuring that Americans get affordable coverage despite rate increases (ie. it doesn’t matter how much a rate is increased, the amount a person, not tax payer, can spend is capped by the poverty level).

- Unfortunately for those without cost assistance, despite new ACA rules deterring insurers from price-gouging, insurers in some regions are jacking up rates by double digit amounts or more. This hits small businesses and those just over the 400% poverty level the hardest as they lack the excess capital, but in some instances have to comply with the mandate. (They can still qualify for other exemptions, like exemptions based on income or for small businesses number of employees).

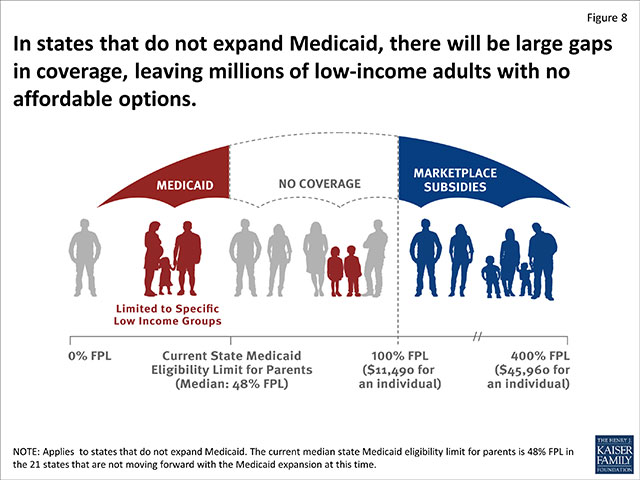

- Even more unfortunate than rate hikes for the 400% plus middle class and small businesses are the lack of options for millions of Americans who fall in the Medicaid Gap caused by the GOP’s anti-ObamaCare anti-safety net ideology.

- The Medicaid Gap is a term that describes the lack of coverage for single adults making less than 100% of the poverty level in 20 states (which rejected 100% funding until 2020 and 90% after 2020). This will leave millions without coverage, based on income and not on assets or if they work or if they have worked in the past and are now too sick to work.

- Funnily enough, in Massachusetts where they have RomneyCare (essentially ObamaCare with a different name), and in some other states that support the program, Medicaid is one of the best coverage types you can have. We will actually get complaints about private insurance (in regard to costs and doctor availability) in Massachusetts but get raving review about Medicaid.

The takeaway, if you make between 100% – 400% of the poverty level you are in a good space under the ACA. In many states you are going to get an affordable premium (and we advise choosing a plan with affordable cost sharing too). If you make less than 100% of the poverty level and your state expanded Medicaid, you are in a really good spot. If you make less than 100% and your state didn’t expand, our hearts go out to you (hopefully the next person you elect will be more caring). If you make just over 400% and your state has high priced premiums, we feel for you too, make sure to shop smart, use HSAs, and look into all of your options including exemptions.

Whatever you do, make sure you get coverage, update your plan, and make sure the plan and cost assistance of your choice is in order before renewal and plan drops take place on December 15th, 2015.

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio