Impact of ObamaCare on Jobs: Does ObamaCare Kill Jobs?

How Does ObamaCare Impact Job Growth, Unemployment, Wages, Operation Costs, or Hiring Practices?

What is the impact of ObamaCare on jobs? is ObamaCare really a Job Killer? ObamaCare does affect job growth, hiring, wages, and consumer costs. However, the impact of ObamaCare on jobs isn’t as drastic as you might have heard.

The Affordable Care Act includes provisions helping to cover millions through employers and the marketplace, creating new jobs in healthcare and government, increasing operating costs for some larger businesses, eliminating “job-lock”, and saving money for small businesses via the SHOP marketplace.

Let’s take a look at ObamaCare and how it affects health insurance affordability and availability for employees, jobs hiring practices, and operation costs.

How ObamaCare Has Impacted Jobs

There are several important ways that ObamaCare leads to job growth, job creation, job loss, and employee coverage:

- The ACA includes a requirement (employer mandate) for firms with more than 50 full-time equivalent employees to provide health coverage to full-time employees.

- As an effect of the new employer mandate some larger firms who have to provide insurance for employees come 2015/2016 are cutting back employee hours to part-time to avoid paying for their health coverage. Other employers have moved workers from part-time to full-time to embrace the law.

- The ACA also includes tax credits for up to 50% of employee premiums to smaller firms with less than 25 full-time equivalents, so they are be able to attract more workers due to their ability to provide them with better benefits at cheaper rates. In the past small businesses paid more than large businesses for health insurance.

- ObamaCare funds the creation of tens of thousands of new jobs in Government and healthcare sectors.

- The ACA helps to eliminate job-lock giving working Americans other affordable options to cover their family without having to depend on an employer for health benefits.

- Due to a “family glitch” some families are finding themselves with unaffordable employer sponsored coverage, and ineligible for marketplace cost assistance.

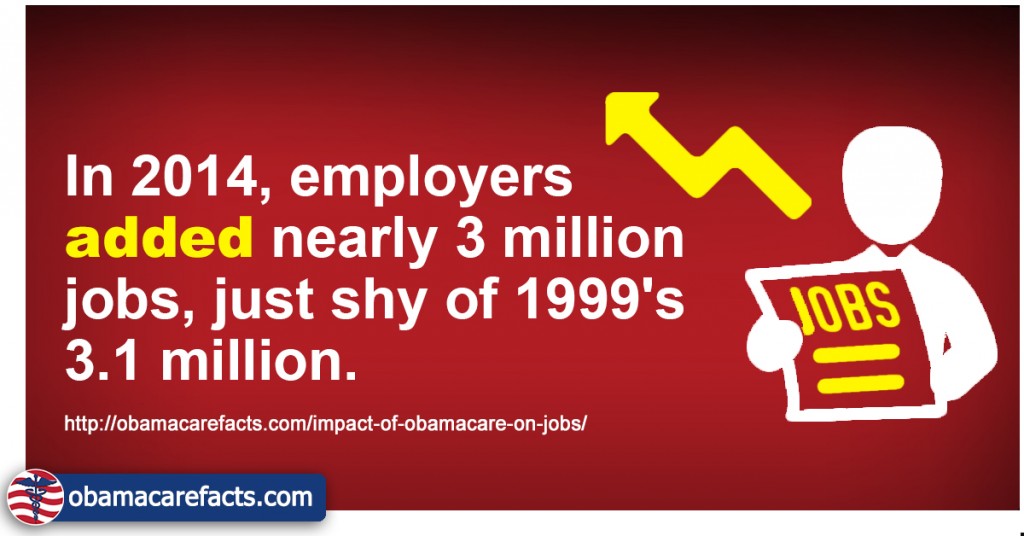

Although many people report hours cut back, actual data shows full-time employment rising, involuntary part-time work falling, and voluntary part-time work rising. The opposite of the claims. It should be noted that we are bouncing back from a recession and thus employment was expected to increase anyway.

Hours Cut Back to Part-Time Due to ObamaCare

Were your hours cut back to part-time so your employer doesn’t have to cover you? On the surface this may seem like a pretty bad deal, but especially in the case of lower wage workers with dependents, you may actually end up saving money by working less. Let’s look at why that is.

If you work full-time for a large employer they must offer you coverage and you cannot get subsidized health insurance through the Health Insurance Marketplace. If they offer coverage to your family, your family can’t get cost assistance through the Marketplace either!

Even after employer contributions, job based coverage on average will be much more expensive than subsidized Marketplace coverage. In addition there are many cases where employee only coverage is affordable, but dependent coverage is not on an employer sponsored plan.

By not being offered insurance by your employer, your family and you may be eligible for cost assistance through the Marketplace. In reality you could be saving big by your employer cutting back your hours. If don’t have dependents, saw a drastic decrease in hours, and/or earn higher wages the chances of this being a benefit to you are decreased.

Bottom-line: Not everyone who had their hours cut back should blame the ACA, as there are many factors beyond health insurance which cause this. However, some larger employers have cut full-time hours to part-time in response to the employer mandate. Typically this means keeping part-time hours at a safe 27 hours a week, since the ACA defines full-time as 30 hours in regards to benefits. For some, this means sacrificing a few hours of income a week for cheaper health insurance for them and their family. For others, this means losing income while at the same time potentially having more costs in regards to health insurance.

ObamaCare Jobs: CBO Report on Jobs

A recent report from the 2014 CBO report on jobs has been used as ammo to back-up the talking point that ObamaCare is a job killer, but the truth is a little more complicated.

The CBO estimates that the ACA will reduce the total number of hours worked, on net, by about 1.5 percent to 2.0 percent during the period from 2017 to 2024. The reduction in the CBO’s projections of hours worked represents a decline in the number of full-time equivalent workers (total hours based on all part-time and full-time employees, not actual job loss from full-time workers losing their jobs or not being able to find work) of about 2.0 million in 2017, rising to about 2.5 million in 2024.

While loss of full-time equivalent hours is partially due to a small number of businesses decreasing full-time workers to part-time, less hours means less full-time equivalents, it is largely a reflection of the Affordable Care Act helping to eliminate health benefit “job-lock” (The term job lock is used to describe the inability of an employee to freely leave a job because doing so will result in the loss of employee benefits, which are usually health or retirement related.)

In other words the report really says the ACA will free people, young and old, to pursue careers or retirement without having to worry about health coverage. Workers can seek positions they are most qualified for and will no longer need to feel locked into a job they don’t like because they need insurance for themselves or their families. The decrease is largely in labor participation and not an increase in unemployment (that is, more workers seeking but not finding jobs) or underemployment (such as part-time workers who would prefer to work more hours per week).

Bottom-line: There are two main factors that lead to a decrease labor participation and full-time equivalent hours (not unemployment). 1) Employers moving full-time employees to part-time and 2) the ACA helping to eliminate job-lock in regards to health insurance.

How ObamaCare Creates Jobs

ObamaCare creates jobs in two ways. First, our tax dollars go to creating millions of new Government and health care jobs. This includes funding for improving training for young adults getting training in health care, new jobs in the health insurance marketplace, new jobs in health education, new jobs in the IRS, and more. The second way ObamaCare creates jobs is through small businesses being able to offer better health benefits and in general more jobs offering coverage and thus making them more attractive.

• Small businesses have increasingly stopped providing health benefits to their employees over the past decade due to the ever-rising cost of health care premiums. The rising costs don’t effect larger firms hiring processes. ObamaCare helps to regulate insurance making it more affordable to small businesses increasing job retention rate and making those jobs more attractive.

• Affordable Health Care Act funds scholarships and loan repayment programs to assist young people with going to school for health care related professions.

• The act promotes much needed jobs in the healthcare industry to prepare for our future thus creating jobs for American workers.

• The Act gives states power to recruit healthcare workers.

• Helps fund and expand community health centers.

Because doctors, nurses, and other health care providers are the backbone of the health care system, the Act supports and expands our Nation’s health care workforce.

ObamaCare Jobs Facts

The fact is, ObamaCare job studies have shown the law has a net increase on job growth, creating millions of new jobs. Of course a net increase doesn’t discount the firms that are cutting back employee hours to part-time to avoid paying for their employee’s health coverage or those who have found themselves in a worse spot due to the family affordability glitch.

• Corporate funded campaigns to defund and repeal ObamaCare are responsible for a lot of the false and slanted information on ObamaCare and jobs. This is because it’s cheaper for them to lobby the Government and fund anti-ObamaCare campaigns than it is to pay their share of it’s costs, to provide health coverage, and to sacrifice their hold over workers by controlling their only access to health care for them and their families. This isn’t something new to healthcare, this is something that happens with every worker right, public program, and tax that helps the average American and costs our largest firms money and power. They count on the public not understanding ObamaCare for their campaigns to work. We count on the American Government to create and enforce regulations that expand our rights. Keep reading the ObamaCare Facts on jobs and in general to help educate yourself and protect your rights.

• 15% of uninsured Americans are full-time workers or their dependents.

• ObamaCare has positive impact on jobs for Small businesses with under 50 full-time equivalent employees.

• Firms with over 50 full-time equivalent employees must provide health insurance to their full-time workers. This, along with a few health care taxes on employers, is what all the controversy is over.

• Some of Americas largest companies have never willingly provided health benefits to their workers. ObamaCare’s “employer mandate” is meant to ensure these companies provide coverage to their workers.

• The firms that must pay the fee, yet don’t provide insurance, only account for .2% of firms in the U.S. although they do employee a large percentage of the workforce. They include corporations like Walmart (Americas largest employer) who are owned by two of the richest people in America. The good news is that because we, as a country, stuck with ObamaCare for the past three years Walmart is now expanding their full-time work force and offering great benefits. This is what happens when we don’t let corporate funded campaigns shut down public programs that help the majority of Americans. Read about Walmart and ObamaCare.

• More than half of Americans get their health coverage through work. In 2011 55.1% of Americans got coverage through their job, the “employer mandate” doesn’t go into effect until 2015.

• ObamaCare provides funding to create many new government jobs and healthcare jobs.

• Some larger firms who don’t insure employees are cutting back employee hours to avoid paying for their health coverage.

• Small businesses can now attract better quality loyal workers due to their being able to provide better quality affordable health benefits.

• A CBO report talked about workers leaving their jobs due to no longer having to rely on their employer for benefits. So some job loss comes from employees no longer depending on their employer for the health of them and their families.

• Despite all the benefits to employers and employees, businesses with over 50 full-time equivalents who have a low profit margin per employee and didn’t offer health coverage before the law and families who found ObamaCare doesn’t offer them assistance due to unaffordable employer based coverage for their family have been hit the hardest by the law. This brings up questions of whether employers should be in charge of employee health care or whether it would be more effective to simply tax employers and let employees shop on the exchanges and for off-marketplace insurance.

ObamaCare Fact: More than 96 percent of the nation’s firms with 50 employees or more already offer health insurance to their workers despite the rising cost of health care (health care costs rise every year, ObamaCare curbs the rate of growth).

Let’s Define “Small Business”

Before we get to the next section it’s important that we get something out of the way. One of the most annoying things about politicians and talking heads is their use of the buzz word “small business”. They use it when they are trying to be folksy and persuade you of something. In reality they are often referring to what we will call “larger businesses” below as small businesses and trying to insinuate that they are mom and pops. Let’s look at how businesses are categorized as it pertains to the Affordable Care Act.

- Mom and Pop Small Businesses – Those with 10 or less full-time equivalent employees and average annual wages of $20,000.

These businesses usually qualify for maximum tax breaks and have historically had the least leverage when it comes to buying power. While the small tech firm or hedge fund making millions may be a small business in terms of employees, for this law their average annual wages prevent them from getting tax breaks… It doesn’t stop the talking heads from lumping these folks in with mom and pops when listing off talking points.

- True Small Businesses – Those with 25 or less full-time equivalents employees making less than $25,000 in average annual wages.

True small businesses have historically had to pay more than large businesses because they lacked group buying power. Today these employers can get tax breaks of up to 50% of their contributions to employee coverage and can use the SHOP website to get the same group buying power large groups can.

- Small Businesses – Those with more than 25 full-time equivalents but less than 49 full-time equivalents (or those making more than 25,000 in average annual wages).

These businesses can’t get the tax credits that smaller businesses can, but they can use the SHOP. They typically lacked the buying power of large firms, so this is good.

- Larger Businesses – Those with between 50-100 full-time equivalent employees making more than $250,000 in average annual wages.

These are the ones who get hit the hardest under the ACA. Unless they had a lot of part-time workers or a decent profit margin the new costs of having to insure their full-timers does mean having to figure out how to cover those costs. Sometimes it’s as simple as raising the price of a hamburger, sometimes it means cutting back some workers to part-time. As a plus they can use the SHOP and that means group buying power. It’s worth noting that they own businesses that employee over 50 full-time workers, so that is the equivalent of 50 workers with families who depend on them and work for them.

- Large Businesses – Those with 100 or more full-time equivalent employees.

Large businesses as a general rule of thumb already offered benefits. Some with smaller profit margins per employee who don’t provide benefits already have had to deal with costs in other ways. In 2016 they can use the SHOP too.

FACT: A small business can range from 1 to 500 employees and do millions upon millions in business. In some industries a small businesses can have up to 1,500k employees.

The Negative Impact of ObamaCare on Employee Health Insurance

The March 2012 CBO report projects that 3 to 5 million fewer people will, on net, obtain health coverage through their employer a year from 2019-2022. This study gives us an idea of how both jobs and employee health insurance will be affected by ObamaCare.

Of course it is not as cut and paste as saying ObamaCare is hurting employees; in fact, many employers and employees will benefit from ObamaCare. Many of these employees will simply get health insurance elsewhere (the exchanges, Medicaid, CHIP) if the employer decides that not insuring them is economical. Here is a breakdown of where those 3 to 5 million are coming from:

About 11 million people who would have had an offer of employment-based coverage under prior law will not have an offer under ObamaCare. That estimate represents about 7 percent of the roughly 161 million people projected to have employment-based coverage under prior law. The businesses that choose not to offer coverage as a result of ObamaCare will tend to be smaller employers and employers with predominantly lower-wage workers; those workers and their families are more likely to be eligible for Medicaid, CHIP, or subsidies through the health insurance exchanges.

Another 3 million people who would have had employment-based insurance under prior law and will still have an offer of such coverage under ObamaCare will instead choose to obtain coverage from another source. Under the legislation, workers with an offer of employment-based coverage will generally be ineligible for exchange subsidies. However, that “firewall” is worked around by the ability of a family member to apply for a hardship exemption giving them access to catastrophic coverage if employment-based coverage for a family member is deemed unaffordable (costing more than 8% of household MAGI per dependent for the cheapest employer plan).

About 9 million people who would not have been covered by an employment-based plan under prior law will have that coverage under ObamaCare. That change reflects the combined impact of the insurance mandate, the penalties that will be imposed on employers who do not offer insurance, and the tax credits for certain small employers who provide insurance for their workers—which will lead some employers who would not have offered coverage in the absence of ObamaCare to offer it and will lead some people who would not have taken up their employer’s offer of insurance to do so.

The Impact of ObamaCare on Employers with Over 50 Full-Time Employees

Job creators with over 50 full-time employees must pay a penalty for not insuring workers. There is also a .09% tax on 3% of small businesses making a profit of over $250k.

The requirement for employers to pay more health care costs and provide insurance will increase operation costs. Of course, that money has to come from somewhere and it’s up to the employer to figure out how they will deal costs associated with ObamaCare. However, the big fib in America right now is that that money has to come from slashing the hours of American workers. The money could come from raising the price of a product or in some cases simply by lowering profit margins. Obviously none of the options are attractive, but cutting hours back past the threshold is only one option and is not the same as cutting back jobs.

Obamacare Hiring and Insurance for Employees. What Aren’t They Telling Us?

Large employers have a long history of using new taxes and wage increases as scapegoats. Just because businesses have to adjust to new regulations doesn’t mean that American health care reform is bad, it just means that these businesses have to evolve and figure out how they will deal with the costs. Most companies will admit that while there are rising costs, the best solution will most likely be protecting shareholders and workers and passing costs onto consumers (usually a matter of a few cents per item).

ObamaCare saves tens of millions of lives and provides unprecedented tax breaks to many small businesses helping them thrive. Already successful companies have already adopted health benefits for their workers without government enforcement.

Papa John’s and the Health Care “Story”

Corporate sponsored entities have been reporting that ObamaCare “kills jobs”, yet no study has shown this. In fact the recent CBO study showed that this was not in fact the case. While some multi-millionaire franchise owners have made a lot of noise, most companies say ObamaCare won’t affect their hiring process or their employees’ hours.

One business who has been very outspoken about their dislike of ObamaCare is Papa John’s. A study shows Papa John’s will have to increase the cost of their pizzas by 4 cents a pie to insure workers. All of this while paying Payton Manning to be the poster boy for a campaign to give away 2 million free pizzas.

Papa Johns tried to gain support for their message by giving customers a deal on a Double Bacon Six-Cheese pizza (wonder how much the health risks involved with that raise insurance premiums on their own?… What do you say about .04 cents on every American?)

Ultimately, Papa John’s CEO has decided while he doesn’t embrace ObamaCare, “Our business model and unit economics are about as ideal as you can get for a food company to absorb ObamaCare. We will find tactics to shallow out any ObamaCare costs and core strategies to pass that cost onto consumers in order to protect our shareholders’ best interests.” Or in summary, Papa John’s puts their shareholders’ best interests before their employees and customers.

So do companies like Papa John’s have a point in saying that employee insurance is too expensive? Of course they do, anyone who has bought a health plan knows first hand why health insurance and the costs of health care have led us to passing health care reform.

There is no easy choices for businesses dealing with new costs, but it’s important to realize that the health and happiness of one’s employees has value. Whether that has more value to a company then the consequences of raising the price of a product is a question each business must answer.

Franchise Owners Take ObamaCare Costs out on Workers

Franchise owners of chains like Papa John’s, KFC, Taco Bell, Red Lobster, Olive Garden, Denny’s, Longhorn Steakhouse, The Capital Grille and Applebee’s say ObamaCare will force them to cut employees’ hours since they can’t afford to provide more full-time workers with health insurance or pay the fines for leaving them uninsured. While normal small businesses won’t meet the 50 or more full-time equivalent employee requirement for insuring employees, many franchise owners own multiple franchises and thus do have to comply.

Many of these chains’ franchise owners have taken the opportunity to talk about the horrors of the cost of ObamaCare. Instead of honestly addressing the many aspects of health care, the workforce, and the law, they simply harp on talking points which say the entire law is bad and new costs MUST be taken out on customers and employees.

Sources for the “job killer” talking points are pretty much only heard from channels like Fox News, Crossroads GPS, Heritage Foundation, and similar openly anti-ObamaCare sources. This is unfortunate as there are many technically larger businesses who are struggling under the law and instead of addressing this matter head on, the “anti-ObamaCare folk” use clever wording to get you to sympathize with the guy who owns 15 McDonalds like he is a mom and pop. As we note above that sort of business does struggle, but the majority of small businesses actually benefit.

The truth of the matter lays somewhere in between opinions from the left and right (as it usually does). The employer mandate truly has a negative impact on smaller large businesses with low profits. However, the answer is certainly not repealing the law due to one provision. The answer rather is to open up a debate in our country about an employers role in health insurance. The video below is from the Heritage Foundation so you can see how they address the issue. Please note that the business they describe is not a mom and pop small business (which the ACA helps drastically), but a businesses with more than 50 full-time equivalent employees.

Small businesses struggled to provide employees benefits before the ACA. This video produced by Heritage Foundation talks about the owner of 12 Ihops (technically a large business). The points they miss include tax breaks for small businesses and the fact that the Health Insurance Marketplace is the way for small businesses to pool buying power in the way large businesses have.Bottom line: ObamaCare really helps small businesses with less than 25 full-time equivalents, creates serious obstacles for businesses who have just barely over 50 full-time equivalent employees and employers with slim profit margins, and doesn’t mean much of much to large employers who already provide benefits and those who don’t qualify for the mandate or tax credits.

What the “Job Killers” Aren’t Telling You

The corporate loudmouths want to blame health care for “killing jobs”, but companies are the ones in control of their hiring and firing process. If they want to slow down productivity, deal with sick workers, low-job retention, and the costs of training and re-training by cutting jobs and wages, then that makes them “job killers”- not ObamaCare. Is there more to this picture? What aren’t these companies telling us?

What they don’t tell you is that over the past decade, the amount of small businesses who can afford to provide health insurance to their employees has dropped dramatically, while larger businesses have been mostly unaffected. 3/4 of small businesses who dropped employee benefits because of the rising costs of health care will receive tax credits to offer their employees insurance. This will help to increase hiring rates and decrease turn over, making small business jobs more attractive.

ObamaCare helps small business, and forces bigger businesses who don’t want to provide benefits to do something that the big boys already do: treat their workers with respect.

Perhaps it’s time to start supporting the 96% of large employers who already offer benefits including WholeFoods, Nordstrom, Starbucks, UPS, Lowe’s, JCPenny, Land’s End, JP Morgan Chase, Barnes & Noble, Target, Home Depot, Costco, among many others who all offer part-time employees health benefits.

How Do Increased Health Benefits Help Businesses Grow Jobs and Hire?

70% of small businesses will be able to insure themselves and workers, something that has become increasingly rare due to the rising costs of insurance premiums. While this has never affected large employers much, small business has been struggling for over a decade. Larger businesses will be able to offer more attractive jobs with better benefits, meaning that those businesses who adopt the ObamaCare model for how employees should be treated will likely see a net increase in profit despite some readjustment.

How ObamaCare Will Impact Job Growth and Hiring due to Associated Costs Moving Forward into 2014

Right now, ObamaCare isn’t costing businesses much (assuming they are in the percentage that does face additional costs), therefore downsizing, cutting hours, and not hiring are all being done in response to what is coming and not what has happened.

“Romney Care” didn’t kill jobs and many successful companies have found that offering benefits improves full-time and part-time job retention and an overall ROI. Companies who feel they have to cut jobs and wages and not hire due to an increase in costs shouldn’t blame the workers rights to health care, they should be looking into their business model to see how they can offer healthcare to full-timer workers and still be competitive. So while ObamaCare affects job growth, hiring, wages and operating costs, are impacted by ObamaCare, the facts are a little more nuanced then the talking points.

Is ObamaCare Really a Job Killer?

![]()

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio