Medicare Part D (Drug Coverage)

What is Medicare Prescription Drug Coverage

Medicare Part D, or Medicare Prescription Drug Coverage, covers the gap between your prescription drug needs and Original Medicare. Original Medicare (Parts A and B) includes basic drug coverage. However, many Medicare beneficiaries have prescription drug needs outside of what parts A and B covers. Medicare Part D is a supplemental insurance, so Original Medicare is required for Part D enrollment.

Supplemental Medigap plans are sold by private companies and can be paired with Original Medicare, Medigap policies, and Medicare Advantage plans without drug coverage.

FACT: ObamaCare fully closed the Part D donut hole in 2020.

Find and compare Medicare Advantage and Drug plans at MedicarePolicyHelper.com.

Is Medicare Part D Minimum Essential Coverage?

Medicare Part D doesn’t count as minimum essential coverage (the type of coverage that counts as “having health insurance” under ObamaCare) on its own. Only Medicare Part A (hospital insurance) and Medicare Part C (Medicare Advantage) count as minimum essential coverage.

Even though Part D isn’t minimum essential coverage on its own, it will always be paired with Medicare Part A or Medicare Part C which are considered minimum essential coverage and so you’ll be in compliance with the law despite Part D not meeting the requirements by itself.

Is Medicare Drug Coverage (Part D) Part of ObamaCare?

Although Medicare Part D isn’t part of ObamaCare’s health insurance marketplace, Part D is affected by ObamaCare’s Medicare reform. Neither Original Medicare or Medicare Part D or other supplemental Medigap insurance and Medicare Advantage plans can be purchased through the health insurance marketplace. Instead, you’ll want to follow the instructions under the “how to sign up for Medicare Part D” section below.

If you want information on how Medicare reform under the Affordable Care Act affects supplemental Medicare, you can learn more on our ObamaCare and Medicare page.

How Does the Affordable care Act Affect Medicare Part D

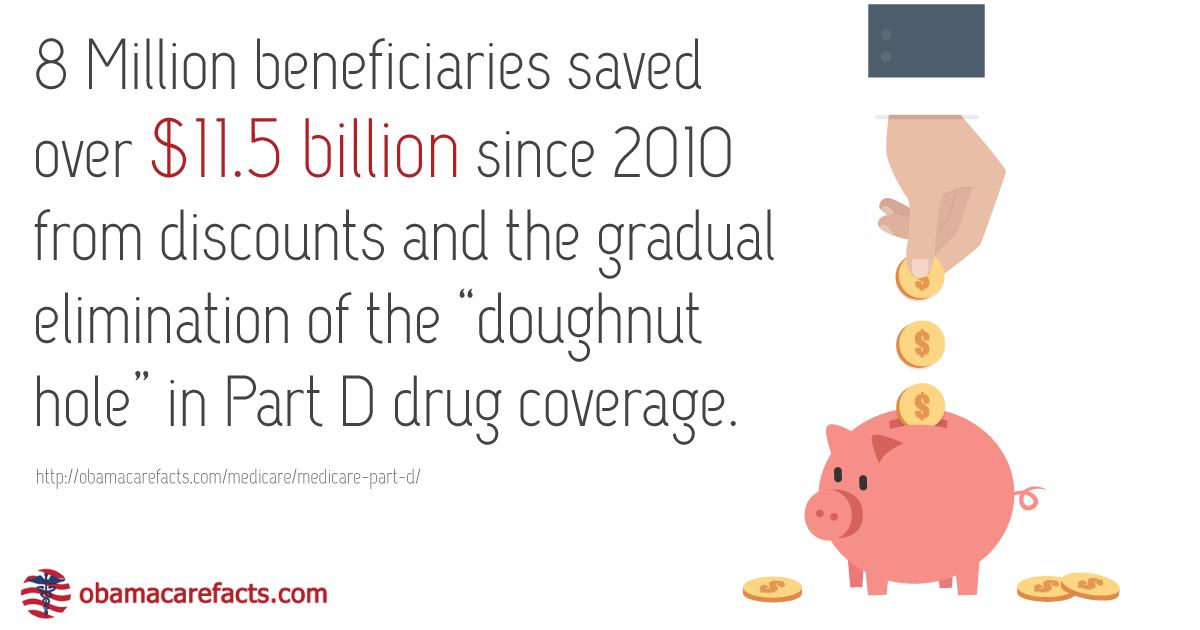

ObamaCare (the Affordable Care Act) helps to close the Medicare Part D donut hole and keep Medicare Part D affordable, sustainable and working for seniors.

The Medicare Part D Donut Hole

ObamaCare helps to make prescription drug coverage more affordable. Because of ObamaCare Part D recipients will now get:

• A discount on covered brand-name drugs when you buy them at a pharmacy or order them through the mail.

• It provides some coverage for generic and brand-name drugs.

• Additional savings on your brand-name and generic drugs during the coverage gap over the next several years until it’s closed in 2020.

If you’re in the donut hole, you’ll also get a 50% discount when buying Part D-covered brand-name prescription drugs. The discount is applied automatically at the counter of your pharmacy—you don’t have to do anything to get it. In addition to the 50% discount on covered brand-name prescription drugs, the percentage you save in the coverage gap (Medicare prescription drug coverage) is currently scheduled to increase each year through 2020.

By 2020, you should pay only 25% for covered brand-name and generic drugs during the gap—the same percentage you pay from the time you meet the deductible (if your plan has one) until you reach the out-of-pocket spending limit (up to $4,550 in 2014). The donut hole will be closed completely by 2020 unless legislation changes.

| Year | You’ll pay this percentage for brand-name drugs in the coverage gap | You’ll pay this percentage for generic drugs in the coverage gap |

|---|---|---|

| 2014 | 47.5% | 72% |

| 2015 | 45% | 65% |

| 2016 | 45% | 58% |

| 2017 | 40% | 51% |

| 2018 | 35% | 44% |

| 2019 | 30% | 37% |

| 2020 | 25% | 25% |

Medicare Part D Facts

We break down Medicare Part D in detail on the rest of the page, but here are some quick facts to help you understand how prescription drug coverage works with Medicare.

• You must already have Medicare Part A and Part B to be eligible for a Medicare Part D plan.

• You can’t have a Part D plan if you have a Part C (Medicare Advantage Plan) with prescription drug coverage.

• You’ll pay your Part D premium in addition to your monthly Part B premium and any Medigap premium you owe.

• Part D coverage is meant to cover additional upfront premium costs with savings on deductibles and out of pocket costs, making prescription drugs more affordable.

• The best time to buy a Medicare Advantage policy and or Part D drug coverage is during your initial Medicare Enrollment Period (see details below).

• Every year there are two open enrollment periods where you can make changes to your Advantage and Part D plans.

How Does Medicare Part D Work?

Medicare Prescription Drug Coverage (Part D) is a supplemental insurance that pairs with Original Medicare (Part A and Part B). Part D will give you better cost savings on prescription drugs in exchange for a monthly premium. Your costs and savings are based on income.

You can have Part D in addition to a Medigap policy or an Advantage Plan without drug coverage. Part D plans are sold by private companies.

When you choose a Medicare Part D Plan, your costs are paid by the company who issued the Part D plan instead of Original Medicare although you’ll still pay your Part B premium on top of your new Part D premium.

Get a better idea of how Medicare Part D works with your current coverage here.

What is the Difference Between Original Medicare and Medicare Part D?

Medicare part D offers better drug coverage in exchange for a bigger upfront cost and does not include hospital or medical insurance. Part D is meant to pair with original Medicare, not replace it.

What Does Medicare Part D Cost?

Medicare Part D comes at a fixed monthly cost, your premium, in exchange your insurer will take on a bigger share of your covered drug costs. If your income qualifies you, then you may qualify for extra help.

Medicare Part D Standard Costs

If you don’t qualify for cost assistance, your Part D costs are simply based on what plan you choose. Different Part D plans will cover different doctor networks, types of drugs and benefits and will have different premiums, deductibles, copayments, and coinsurance. Every plan is different, and some similar plans may be sold for different amounts by different insurers in your area. The best way to get the right coverage for you is to shop around to know your past and projected Medical needs.

Medicare Part D Late Enrollment Penalty

The best time to sign up for Part D is during your initial enrollment period, which is the 60 day period after you enroll in part B. If you enroll after your initial enrollment period, you may pay a higher premium every month due to a “late enrollment penalty.”

Medicare Part D Cost Assistance

Your income level determines how much cost assistance you can get on your Part D drug coverage. If you are eligible for Medicare Part D and don’t have a lot of income, you may qualify for cost assistance. Here are the current income limits and benefits of the four levels of benefits under Extra Help for 2013 through early 2014:

Level 1: If you receive full Medicaid benefits and live in a nursing home, you automatically qualify for full Extra Help and pay nothing for your prescription drugs.

Level 2: If you receive Medicaid or Supplemental Security Income (SSI) or if your state pays your Medicare premiums, you automatically qualify for full Extra Help. You pay no premium or deductible for Medicare drug coverage. Depending on your income, your copays for each prescription are $1.15 or $2.65 for generics; $3.50 or $6.60 for brand names and nothing for catastrophic coverage.

Level 3: If your current income is no higher than $1,293 a month (single) or $1,745 a month (for a married couple living together), and your assets (mainly savings) are no more than $8,580 (single) or $13,620 (married), you pay no premium or deductible. Your copays for each prescription are $2.65 for generic, $6.60 for brand-name drugs and nothing for catastrophic coverage.

Level 4: If your current income is no higher than $1,436 a month (single) or $1,939 a month (for a married couple living together), and your assets (mainly savings) are no more than $13,300 (single) or $26,580 (couple), you pay a percentage of your plan’s premium depending on income. You also pay $66 annual deductible; no more than 15 percent of the cost of each prescription; and, at the catastrophic level of coverage, $2.65 for generics and $6.60 for brand-name drugs or 5 percent of the cost, whichever is greater. The asset limits above include $1,500 per person for intended funeral expenses, whether or not you’ve set aside money for this purpose.

Data from aarp.org.

Am I Eligible for Medicare Part D

To be eligible for a Medicare Prescription Drug Coverage (Medicare Part D) you must have Medicare Part A and Part B and live in the plan’s service area. If you only have Part A, you will become eligible for Part D when you join part B. At this point, you will have a 60 day initial enrollment period (see below) to switch to an Advantage plan.

During initial enrollment, you cannot be denied Part D drug coverage for any reason. Once you have a plan, you can’t be dropped for any reason other than not paying your premium or committing fraud.

Should I Get a Medicare Part D?

Seniors whose medical costs and needs aren’t adequately covered by Original Medicare usually supplement their plans with Medigap, Prescription Drug Coverage (Medicare Part D), or Medicare Advantage (Medicare Part C). The supplemental insurance you choose should be based on your specific medical needs. Any broker, agent, or provider authorized to sell supplemental Medicare plans can help you choose the right plan for you, but be aware that different insurers can charge different amounts for the same coverage, so you’ll always want to shop around before buying.

Please note you must have Medicare Part A and Part B to get Part D. However you can pair Part D with a Medigap policy or with an Advantage Plan that doesn’t offer Part D coverage.

Does Medicare Part D Cost More Than Original Medicare?

Medicare Part D will typically come at a higher premium price than Original Medicare and will be paid for on top of your Part B premium. This cost is meant to be offset by your actual annual medical claims and the additional benefits offered by your Part D coverage.

Should I Get Part D If I Have Medicare Advantage or Medigap?

Prescription Drug Coverage under Medicare Part D pairs with Medigap plans and Medicare Advantage Plans that don’t offer drug coverage. The benefit over one avenue or another depends on your specific medical needs and projected medical costs weighed against available plans in your area.

Medicare Part D Initial Enrollment Period

Your initial Medicare enrollment period is 3 months before, the month during, and the month after you turn 65. There are several special enrollment periods discussed below as well.

You can sign up for a Medicare Advantage Plan or Medicare Prescription Drug Coverage (Part D), or make changes to coverage you already have during your Medicare Part D initial enrollment period. Your initial enrollment periods are these.

1. When you first become eligible for Medicare or when you turn 65, during your Initial Enrollment Period. This includes 3 months before you turn 65, the month you turn 65, and 3 months after. The period is extended for those who qualify for Medicare due to disability.

2. During certain enrollment periods that happen each year.

a) Between April 1–June 30 of each year you are eligible to switch to a Medicare Prescription Drug Plan (Part D) if you don’t have Part A and you enroll in Part B during the January 1–March 31 general enrollment period.

b) Between April 1–June 30 of each year you are eligible to switch to a Medicare Advantage Plan (Part C) if you have Part A and you enroll in Part B during the January 1–March 31 general enrollment period.

3. Under certain circumstances that qualify you for a Special Enrollment Period (SEP), like:

■ You move.

■ You’re eligible for Medicaid.

■ You qualify for Extra Help with Medicare prescription drug costs.

■ You’re getting care in an institution, like a skilled nursing facility or long‑term care hospital.

Please note there is a late enrollment penalty added to your Part D premium for the duration of your coverage if there is a period of 63 days in a row where you don’t have Part D or any other creditable prescription drug coverage after your initial enrollment period.

See this Medicare Part D Open Enrollment PDF from Medicare.gov for more Medicare Advantage open enrollment and sign up information.

Medicare Part D Open Enrollment Periods

The open enrollment periods for Medicare Part D are January 1–February 14 and October 15–December 7. During this time you can change your Part D drug plan or Advantage Plan. Open enrollment periods are not the same as your initial Medicare enrollment period discussed above. See the table below for the specifics of each enrollment period.

First Medicare Advantage Open Enrollment Period: January 1–February 14

■ Change from Original Medicare to a Medicare Advantage Plan.

■ Change from a Medicare Advantage Plan back to Original Medicare.

■ Switch from one Medicare Advantage Plan to another Medicare Advantage Plan.

■ Switch from a Medicare Advantage Plan that doesn’t offer drug coverage to a Medicare Advantage Plan that offers drug coverage.

■ Switch from a Medicare Advantage Plan that offers drug coverage to a Medicare Advantage Plan that doesn’t offer drug coverage.

■ Join a Medicare Prescription Drug Plan.

■ Switch from one Medicare Prescription Drug Plan to another Medicare Prescription Drug Plan.

■ Drop your Medicare prescription drug coverage completely.

Second Medicare Advantage Open Enrollment Period: October 15–December 7

■ If you’re in a Medicare Advantage Plan, you can leave your plan and switch to Original Medicare. Your Original Medicare coverage will begin the first day of the following month.

■ If you switch to Original Medicare during this period, you will have until February 14 to also join a Medicare Prescription Drug Plan to add drug coverage. Your prescription drug coverage will begin the first day of the month after the plan gets your enrollment form.

Note: During this period, you can’t:

■ Switch from Original Medicare to a Medicare Advantage Plan.

■ Switch from one Medicare Advantage Plan to another.

■ Switch from one Medicare Prescription Drug Plan to another.

■ Join, switch, or drop a Medicare Medical Savings Account Plan.

How to Sign Up For Medicare Part D

To enroll in a Medicare Part D Plan follow the steps below:

1. First, make sure you qualify for Original Medicare, you’ll need to enroll in Parts A and B to be eligible for a Part D Plan. To sign up for Original Medicare go to Medicare.gov.

2. Make a choice between Medicare Advantage and a Medigap Plan. Medigap plans supplement your original Medicare plan while an Advantage Plan effectively replaces it, most Advantage Plans already have.

3. Once you decide what direction you want to go with your supplemental Medicare insurance, you’ll want to find a broker, agent, or provider authorized to sell Medicare Part D Plans to help you choose the right plan for you based on your specific needs. Remember you’ll want to check out your current policy options to know if Part D will make sense with your other supplemental Medicare policies.

Medicare Part D Coverage Choices

Choosing the right Medicare Part D drug plan depends upon your medical needs and costs. You’ll want a plan that covers your known needs and projected needs at a cost that will result in lower total costs than original Medicare. Make sure to choose a plan that includes drug coverage and a doctor network that will meet your needs. If a specific doctor is very important to you, find out what networks they participate in and factor that into your insurance choice.

Should I Get Medicare Part D?

Whether or not Medicare Advantage makes sense for you depends on your intentions and specific situation. In many cases, Medicare Advantage will make sense if your total annual costs will be reduced with an Advantage Plan over an Original Medicare plan. Remember you can call any broker, agent or provider authorized to sell these plans and ask them to help you through the process.

Understanding Medicare Part D (Drug Coverage)

![]()

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio