Why So Many U.S. Counties Have One or Less Obamacare Insurer

Why Do So Many Counties Only Have One ObamaCare Insurer?

Although only a few states have a number of ObamaCare insurers offering plans, some have only one or two. We explain what this means.[1][2][3]

UPDATE: As of late August (shortly after this article was written) it was announced there will be no counties without at least one ObamaCare plan offered. In other words, there will be no county without an ObamaCare insurer in 2018. See: There are no more counties without any Obamacare plans.[4]

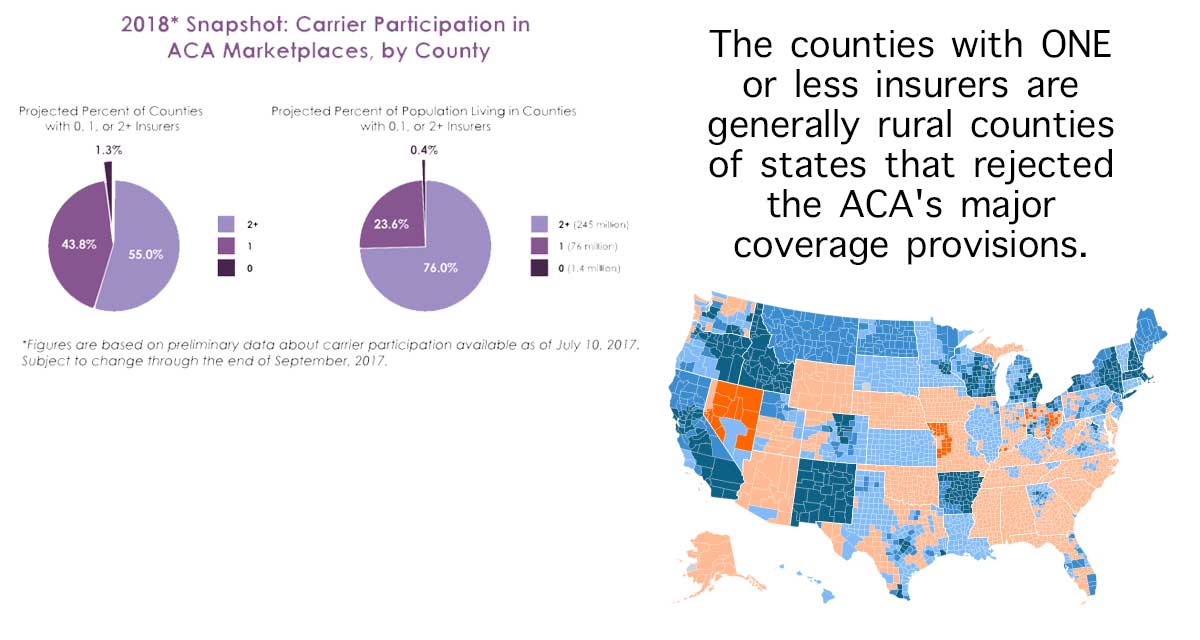

FACT: In August it was estimated that about 1/3rd of counties have only 1 or 2 insurers and about 40% would have only 0, 1, or 2. As noted above, this situation has improved slightly, but the fact remains there are still a number of districts with only a few insurers. With that in mind, almost none of these districts with a limited selection are populated districts, and almost all of those are rural districts in states that rejected ObamaCare’s major coverage provisions. Like with the premium increases, the numbers sound big… until you realize certain areas of the country who purposefully obstructed ObamaCare are dragging down the averages. That said, it is still a real problem (of population distribution and politics), and one that we should all be working together to solve. We explain that problem in context below.[5]

Is ObamaCare to Blame for the Lack of Participating Insurers?

The lack of participating insurers may seem like a serious problem with the Affordable Care Act, but the reality is that not much of this has to do with the ACA as written.

Rather, a lot of this has to do with the fact that the counties with the least insurers are generally rural counties of states that rejected the ACA’s major coverage provisions.

In other words, the general rejection and obstruction of the Affordable Care Act’s major provisions for the past 7 years has, as one would expect, had a negative effect on the citizens of Red states (especially in rural districts). This drags on the entire private individual market and family insurance market as a whole (impacting people across all 50 states).

With all due respect to the GOP, this is exactly what was to be expected given the strategy to break ObamaCare that the GOP implemented back in 2009.

The plan then was simple, obstruct key provisions of the ACA, let the beast collapse under its own weight, then the GOP gets to come in with a free-market solution.

That problem with that is: The GOP plan to create a death spiral worked, but they failed to follow up with a meaningful reform (or at least to ensure the votes to pass their less-than-meaningful BCRA).

I don’t mean to be overly critical of Republicans here, and certainly the ACA and Democrats deserve some blame too, but at the same time it is hard to look at the “Number of Issuers Participating in the Individual Health Insurance Marketplaces [by state, over time]” or “2018 Insurance Plans By County” and not be a little frustrated to see the states that supported the ACA being at the top of the list and the supports that rejected it being at the bottom.

Its clear the politics wasn’t the only issue, but it was such a glaring and impactful issue that one can’t in good conscious ignore it all these years of obstruction later.

At this point the end result was not a GOP healthcare, the end result is millions of suffering Americans paying more money for no reason other than politics (which is frustrating as if that same attention was focused on making the exchanges work, it could have been much different today).

This is sad for those paying more, and this is sad for people in those mostly rural and southern districts… but the rejection of Medicaid expansion by those states was sad too (this is part of what caused insurers to flee those eras), the rejection of cost sharing reduction was sad (this caused some to pull out), the rejection of readjustment payments was sad (this caused some to pull out), and the general opposition to the ACA was sad (this caused some insurers to pull out).

So, while the ACA isn’t perfect, and all parties deserve some blame, and while some of this is just an issue of rural areas without a lot of providers not being able to provide a competitive marketplace to entice insurers to participate, one can’t help but roll their eyes and be like “yeah, that is what we were trying to warn people of back in the Obama years when the obstruction started!”

The GOP tried everything they could to cause a death spiral, it worked, and now they don’t have a meaningful reform plan (or the votes to pass their less-than-meaningful BCRA).

We are all on the same page here, “this is sad,” but that sadness shouldn’t be fodder for more talking points. It should be the basis for the parties coming together to actually fix our current problems. Also, like with an electoral map, we need to stop treating wide-open spaces exactly the same as urban counties. Obviously there are more providers in NY and CA then Montana. That has more to do with the reality of population density than it does with the politics of Montana vs. California.

TIP: See “2 Maps Show The Big Obamacare Crisis Republicans Keep Citing Isn’t Actually That Big It’s a real issue for some parts of the country. But it’s not so hard to fix” for more on how to understand the actual problem here. Consider this quote from the article “ACA marketplaces work well in densely-populated liberal areas. The marketplaces require more care and feeding to really succeed in Wyoming, Iowa or Oklahoma.” – Harold Pollack, University of Chicago… in other words, instead of obstructing healthcare reform in those eras, if we worked together to solve healthcare reform and better serve those communities the we could turn this death spiral into a health spiral.

- “Number of Issuers Participating in the Individual Health Insurance Marketplaces [by state, over time]“

- “2018 Insurance Plans By County“

- Donald Trump: One-third of counties have only one insurer on Affordable Care Act exchanges

- There are no more counties without any Obamacare plans

- About 1/3rd of counties have one or no insurers

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio