ObamaCare Explained | An Explanation of ObamaCare

ObamaCare Explained as Simply As Possible

We explain everything you need to know about ObamaCare (the Affordable Care Act) in as simple terms as possible.

A Quick Introduction to the Affordable Care Act

ObamaCare, officially called the Patient Protection and Affordable Care Act, is a health care reform law signed in 2010 by President Barack Obama. The general goal of the law is to improve the quality, access, and affordability of healthcare and health insurance.

Some of the law’s provisions started immediately, most of the major ones went into effect in 2014, and the rest continue to roll out until 2022.

The law itself is rather long and contains a number of provisions aimed at less than exciting things like improving the quality of care at hospitals, getting rid of waste and abuse in Medicare, curbing costs over time, and putting calorie counts on the menu at fast-food restaurants (see a summary of all provisions here).

However, when people think of ObamaCare they typically think of a few specifics like the new benefits, rights, and protections for consumers, the mandate for most Americans to have insurance (reduced to $0 in 2019 in most states), the mandate for large employers to provide insurance, the expansion of Medicaid, and the opening of Health Insurance Marketplaces to help subsidize private insurance.

In other words, people are typically discussing ObamaCare’s “coverage provisions,” “cost assistance,” and “mandates” when they discuss the law.

With that in mind, the next section contains a quick summary of the law’s major provisions.

This video discusses lots of aspects of the ACA in a pretty clear cut way.FACT: ObamaCare was a nickname given to the Patient Protection and Affordable Care Act. It is also called the Affordable Care Act, PPACA, or ACA. No matter what people call it, the content of the law is the same.

ObamaCare in 132 Words – A Quick ObamaCare Summary

The Affordable Care Act (sometimes called ObamaCare or the ACA) increases the quality, accessibility, and affordability of health insurance. For example:

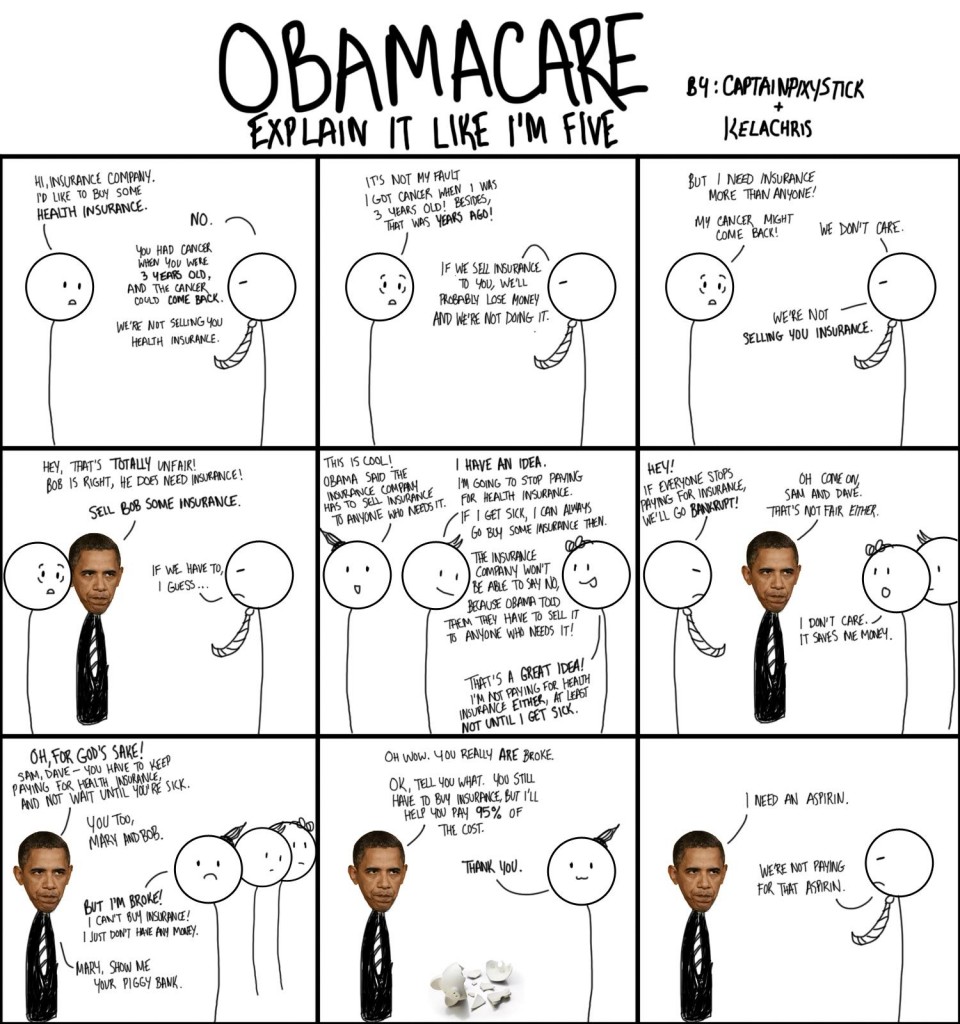

- It stops insurance companies from denying you coverage or raising costs based on pre-existing conditions.

- It stops insurance companies from dropping you when you are sick.

- It protects against gender discrimination.

- It expands free preventative services and health benefits.

- It expands Medicaid and CHIP.

- It improves Medicare coverage.

- It requires larger employers to insure their employees.

- It creates a marketplace for subsidized insurance providing tens of millions of individuals, families, and small businesses with free or low-cost health insurance.

- It aims to curb the growth in healthcare costs.

NOTE: There used to be a fee for not having health insurance, but that was reduced to $0 in most states in 2019.

The Politics of ObamaCare Explained

We may think of the Affordable Care Act as something Obama or the Democrats did, but the reality of the situation is that it was based on Mitt Romney’s Massachusetts health plan (AKA RomneyCare) and includes “a mandate system” first suggested by the right-leaning Heritage Foundation. The final law even excluded a Public Option which many Progressive Democrats had pushed for. The law was passed by Democrats, but many of the provisions actually have a history of bipartisan support.

Trump’s Repeal Plan Explained

Republicans had attempted to repeal the law about 50 times during Obama’s Presidency, and Trump won on a promise of “making healthcare great again”. What does this mean in practice?

In simple terms:

- The 50+ repeal attempts and a few related lawsuits meant that some provisions, like Medicaid expansion, didn’t cover as many people as they were supposed to.

- Changes under Trump included getting rid of the mandate to get coverage. There were more changes planned, but a bill was unable to be passed. For more, see TrumpCare vs. ObamaCare.

- There is a Supreme Court case that declared that law unconstitutional that is making its way to the Supreme Court. Nothing changes for now, but it could impact the law after the legal process plays out.

In short, there have been a few changes due to Republican efforts to repeal both under Trump and Obama, but mostly the ACA has remained intact.

ObamaCare Explained – In More Detail

Above are the basic essentials, below is a simplified explanation of what every American should know about the new health care law.

The Affordable Care Act (ACA) does a lot, and we can’t cover it all here.

Luckily, most of us don’t need to know the details. Let’s take a look at what we do need to know:

• ObamaCare doesn’t create health insurance – it regulates the health insurance industry and helps to increase the quality, affordability, and availability of private insurance.

• Most people who currently have health insurance can keep it (see more on keeping your grandfathered health plan).

• Young adults can stay on their parents’ plan until 26.

• If you don’t have coverage, you can use the new Health Insurance Marketplace to buy a private insurance plan.

• You can obtain private health insurance during each year’s annual open enrollment period in the Health Insurance Marketplace. Open enrollment for 2017 went from November 15th, 2016, to January 1st, 2017. Dates are subject to change each year.

•You won’t be able to obtain most types of private coverage that protect you from the fee outside of open enrollment since most insurers have adopted the health insurance marketplace’s enrollment periods. Medicare and employer-based insurance have unique enrollment periods. Medicaid and CHIP can be obtained at any time.

• If you don’t obtain coverage and maintain coverage throughout each year or get an exemption, you must pay a per-month fee on your federal income tax return for every month you are without health insurance.

• Due to a coverage gap exemption that applies to all Americans, you can go without insurance for up to 3 months in a row without coverage.

• Beyond the coverage gap exemption, there are around 20 other exemptions that you might qualify for.

• Insurance purchased by the 15th of each month will start on the first of the next month.

• For 2016 the annual fee for not having insurance was $695 per adult and $347.50 per child (up to $2,085 for a family), or 2.5% of household income above the tax return filing threshold for your filing status – whichever is greater. Remember, the fee was reduced to $0 in 2019 in most states.

• The cost of your marketplace health insurance works on a sliding scale. Those who make less, pay less.

• Americans making between 100% – 400% o the federal poverty level may be eligible for premium tax credits through the marketplace. Tax credits subsidize insurance premium costs.

• If you can get qualified health insurance through your employer, you won’t be able to receive marketplace tax credits unless the employer will not cover at least 60% of your premium cost, does not provide quality insurance, or provides insurance that exceeds 9.5% (adjusted each year) of your family’s income.

• Up to 82% of nearly 16 million uninsured U.S. young adults qualify for federal subsidies or Medicaid through the marketplace.

• You don’t have to use the marketplace to buy insurance, but you should fill out an application to see if you qualify for assistance before shopping for insurance outside of the marketplace.

• The ACA does away with pre-existing conditions and gender discrimination, so these factors will no longer affect the cost of your insurance on or off the marketplace.

• You can’t be denied health coverage based on health status.

• You can’t be dropped from coverage when you are sick.

• Health Insurers can’t place lifetime limits on your coverage. As of 2014 annual limits are eliminated as well.

• All new plans sold on or off the marketplace must include a wide range of new benefits. These include wellness visits and preventative tests and treatments at no additional out-of-pocket cost.

• All full-time workers who work for companies with more than 50 employees must be offered job-based health coverage by 2015. Employers who do not offer coverage will pay a per-employee fee.

• Small businesses with under 50 full-time employees can use a part of the marketplace called the SHOP (small business health options program) to purchase group health plans for their employees.

• Small businesses with fewer than 25 full-time employees can use the marketplace to purchase subsidized insurance for their employees.

• Medicare isn’t part of the marketplace. If you have Medicare, keep it!

• Medicaid and CHIP are expanded to provide insurance to reach up to 16 million of our nation’s poorest individuals.

• When you apply for the marketplace, you’ll find out if you qualify for free or low-cost coverage from Medicaid or the Children’s Health Insurance Program (CHIP). You’ll also find out if you qualify for Medicare.

Want to explore the ACA in more detail? See our summary of every provision in The Patient Protection and Affordable Care Act here and learn more about getting health insurance through your state’s health insurance marketplace here.

Watch the following video for a simple and complete explanation of ObamaCare basics.What Does ObamaCare Do? – Specifics Explained

ObamaCare helps tens of millions of Americans get access to affordable health insurance by expanding Medicaid and CHIP, improving Medicare, and setting up a “Health Insurance Marketplace” where Americans making under 400% of the federal poverty level can purchase subsidized health insurance. ObamaCare’s reforms also increase the quality of care and help to curb the growth in healthcare spending.

ObamaCare’s provisions regulate insurance companies and healthcare standards, but they don’t regulate your health care or replace private insurance. ObamaCare lowers what most middle-to-low income Americans pay for health insurance and reduces their out-of-pocket health care costs using cost-assistance offered through the marketplace. It decreases the deficit and improves government-run health care programs like Medicare by working to cut out wasteful spending. ObamaCare also expands Medicaid in some States to cover 15.9 million uninsured seniors and low-income individuals.

ObamaCare Explained: Individual Mandate. Most Americans had to buy insurance from 2014 – 2018. Those who aren’t covered by Medicaid, CHIP, or Medicare had several options. People could buy private insurance or obtain insurance through the workplace. Those who didn’t get covered would owe a fee. However, the fee was reduced to $0 in most states in 2019.

ObamaCare Explained: Your State’s Health Insurance Exchange / Marketplace. The ObamaCare exchanges are state or federally run (depending on the state) online marketplaces where health insurance companies compete to be your provider. Getting insurance through the marketplace is as easy as applying for a plan, finding out if you qualify for subsidies, and then comparing competing health plans. A State’s “Exchange” is commonly referred to as “Health Insurance Marketplace”.

ObamaCare Explained: How to Buy Health Insurance. You can obtain private coverage inside or outside of the marketplace during open enrollment in your State’s “Health Insurance Exchange Marketplace.” During open enrollment, all eligible Americans will be able to use the marketplace to purchase Federally regulated and subsidized health insurance through private providers using the side-by-side benefit, rate, and network plan comparisons. When you sign up for the marketplace, you’ll also find out if you or a family member qualify for Medicaid, CHIP, or Medicare. 82% of uninsured young people are expected to qualify for free or low-cost health insurance. Check out our Health Insurance Marketplace Guide.

ObamaCare Explained: How to Buy Health Insurance. You can obtain private coverage inside or outside of the marketplace during open enrollment in your State’s “Health Insurance Exchange Marketplace.” During open enrollment, all eligible Americans will be able to use the marketplace to purchase Federally regulated and subsidized health insurance through private providers using the side-by-side benefit, rate, and network plan comparisons. When you sign up for the marketplace, you’ll also find out if you or a family member qualify for Medicaid, CHIP, or Medicare. 82% of uninsured young people are expected to qualify for free or low-cost health insurance. Check out our Health Insurance Marketplace Guide.

You can also purchase private health plans through a broker or directly from the provider. If you qualify for Medicaid or Medicare, you can sign up through the official .gov sites.

ObamaCare Explained: Businesses. Small businesses with the equivalent of 25 full-time employees making less $250,000 a year can get access to tax breaks through the SHOP marketplace for providing insurance to their workforce. Those with the equivalent of 50 full-time employees will have to provide coverage for their full-time workers by 2015. 3% of small businesses will pay an increased Medicare tax on profit over $250,000 as well. The rest of the small businesses, mom and pops specifically, will have better access to cheaper healthcare for their employees. If they do decide to provide insurance for their employees, they will receive generous tax breaks. Over half of all small business owners and their employees go without insurance each year, and small businesses have historically struggled to provide benefits of a similar quality to those provided by larger firms. ObamaCare’s provisions give small business a fair shake.

ObamaCare Explained: Seniors. Seniors benefit from both cutting $716 billion of wasteful spending from Medicare and closing of the donut hole. The money is reinvested in Medicare and ObamaCare to improve coverage and to help provide insurance for tens of millions of seniors. Medicare parts A, B, C, and D have all changed – and almost all for the better. Find out more about ObamaCare and Medicare.

ObamaCare Explained: Rights and Protections. ObamaCare includes important protections for Americans. It provides better access to preventive services and expands coverage to millions. It ensures that people can’t be denied coverage if they have pre-existing conditions or dropped by their insurance companies you when they are sick. It lets young adults stay on their parent’s plans until 26. The law also regulates insurance premium hikes and improves the appeals process.

Why We Need Health Care Reform Explained?

The health insurance and health care industries are for-profit industries. As such, they put their profit before your health. In many ways, it is left up to the law to regulate their practices. Understanding the law requires an understanding of the health insurance and health care industries as well as a lot of research and experience.

The complexity of the law and the 3 trillion dollar plus U.S. healthcare system both defy any simple explanation. Suffice it to say: We need health care reform to help America focus less on convenience and profit and to encourage America to focus more on wellness, prevention, and health.

ObamaCare Explained Summary

ObamaCare helps save millions of lives, frees up billions of dollars, and gives American workers more freedom by facilitating their independence from their employers and insurance companies for care. Health care is now in your hands – it’s your health care. The government’s job is to try to ensure that you get a fair shake and that the insurance companies play by the rules. Thanks for checking out our quick ObamaCare explained breakdown. Check out the rest of the site for a more detailed explanation of ObamaCare.

ObamaCare Explained

![]()

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio