Qualified Health Plan

What is a Qualified Health Plan?

Under the Affordable Care Act (ObamaCare), a Qualified Health Plan (QHP) is a health plan certified by the marketplace to meet new benefit and cost sharing standards. Qualified Health Plans include all the metal plans sold on the marketplace and count as minimum essential coverage.

Let’s take a look at what a Qualified Health Plan is and isn’t and how they differ from other types of minimum essential coverage.

In states with a mandate, and on a federal level from 2014 – 2018, you needed minimum essential coverage to be protected from the fee for not having insurance (the fee was reduced to $0 in 2019 in most states).

FACT: All plans sold on the marketplace are certified Qualified Health Plans and are considered minimum essential coverage, and that means all marketplace plans offer the ACA’s benefits, rights, and protections and qualify for cost assistance based on income!

What Makes a Plan a Qualified Health Plan?

For a plan to be sold on the marketplace it must be certified as a Qualified Health Plan. To be certified as a Qualified Health Plan, that plan must meet certain requirements including.

1. Providing at least ten essential benefits.

2. Follows established limits on cost-sharing (like deductibles, copayments, and out-of-pocket maximum amounts and provide minimum actuarial value).

3. Meets all other minimum standards outlined by the Affordable Care Act.

A qualified health plan will have a certification by each Marketplace in which it is sold.

Qualifed Health Plan Defined

Below is the definition of qualified health plan from the Affordable Care Act itself:

PART I–ESTABLISHMENT OF QUALIFIED HEALTH PLANS

SEC. 1301. QUALIFIED HEALTH PLAN DEFINED.

(a) Qualified Health Plan- In this title:

(1) IN GENERAL- The term ‘qualified health plan’ means a health plan that–

(A) has in effect a certification (which may include a seal or other indication of approval) that such plan meets the criteria for certification described in section 1311(c) issued or recognized by each Exchange through which such plan is offered;

(B) provides the essential health benefits package described in section 1302(a); and

(C) is offered by a health insurance issuer that–

(i) is licensed and in good standing to offer health insurance coverage in each State in which such issuer offers health insurance coverage under this title;

(ii) agrees to offer at least one qualified health plan in the silver level and at least one plan in the gold level in each such Exchange;

(iii) agrees to charge the same premium rate for each qualified health plan of the issuer without regard to whether the plan is offered through an Exchange or whether the plan is offered directly from the issuer or through an agent; and

(iv) complies with the regulations developed by the Secretary under section 1311(d) and such other requirements as an applicable Exchange may establish.

Qualified Health Plans Vs. Minimum Essential Coverage

All Qualified Health Plans count as minimum essential coverage, but not all minimum essential coverage types are Qualified Health Plans. Minimum essential coverage is the type of insurance you need to avoid the fee and includes insurance types like Medicare, Medicaid, CHIP, TRICARE, etc. Qualified Health Plans are only health plans sold on the marketplace. Learn more about minimum essential coverage.

How to Buy a Qualified Health Plan

There are two ways to get a Qualified Health Plan:

1. You can buy a Qualified Health Plan directly from the marketplace, as all plans sold on the marketplace are QHPs.

2. Since all plans sold on the marketplace are also sold outside of the marketplace you can also buy your health plan outside of the marketplace from any provider, agent, or broker who sells Qualified Health Plans in your area.

Learn more about how to buy health insurance.

ObamaCare Quotes by ObamaCareFacts.com

ObamaCare Metal Plans

There are four types of Metal plans you can choose from in your state’s Health Insurance Marketplace as well as a catastrophic health plan.

Actuarial value

Before you read this section it is very important that you understand actuarial value. Actuarial value is the average amount a plan will pay for covered services for everyone using the plan, it is not what the plan will pay you specifically. Premiums and costs not covered by your plan don’t factor into determining actuarial value, only costs insurers pay count.

Types of Metal Plans

Each metal plan has a minimum average actuarial value which can be used to tell how good a plan is, what type of subsidies it qualifies you for based on income, and if it provides minimum value.

NOTE: All marketplace plans have a maximum out-of-pocket cost no more than $6,600 for an individual and $13,200 for a family in 2015 and must provide at least ten essential benefits as part of their covered benefits.

1. Bronze plans split covered expenses 60-40 on average.

Bronze plans are the cheapest plans. All employer plans and non-catastrophic marketplace plans must provide at least the value of a bronze plan.

For a Bronze plan with 60% actuarial the insurer will, on average, pay 60 % of covered health expenses while the policy holder must come up with the other 40%. In other words a plan with 60% actuarial value covers 60% of out-of-pocket costs on average for all policy holders, not just you.

Bronze plans have the most basic benefits and most limited networks of doctors and hospitals. The actuarial value reflects this since that percentage is determined by the average expenses your insurer will have.

A Bronze plan is a good choice for those who don’t plan on using many medical services. Many low-income Americans may qualify for free or very low-cost Bronze plans. That being said in many cases a Silver plan will provide better value as Bronze plans won’t qualify for Cost Sharing Reduction subsidies (CSR). You will be getting a low premium in exchange for the fact that you will pay more out-of-pocket and have a more narrow network.

More than 50% of all medical costs are incurred by a very few unfortunate people. Since your deductible will be high and all plans have the same maximum limits on the amount you can pay in a year, most of the costs you pay for a Bronze plan will go to the unfortunate people who get cancer or have a bad accident and reach their cost sharing limit.

2. Silver plans split covered expenses 70-30 on average.

Silver plans are “the marketplace standard” meaning that premium caps are based on the cost of Silver plans. A Silver plan on the marketplace can’t cost more than 9.5% of your income if you make less than 400% of the Federal Poverty Level (FPL) due to Advanced Premium Tax Credits. The less you make, the lower your premium cap is.

Like Bronze Plans, the actual value of Silver plans can range. They simply must have at least a 70% actuarial value.

Silver plans are the only plans eligible for Cost Sharing Reduction subsidies (CSR)

A Silver level plan is a good choice for individuals and families who have access to marketplace subsidies, especially CSR subsidies. If you make below 250% FPL the chances you won’t find your best plan to be a marketplace Silver plan is slim. Go with an HMO when in doubt, you’ll need referrals, but this will be your cheapest option. Like with any other plan, make sure your medical needs are covered in-network.

3. Gold plans split covered expenses 80-20 on average.

Gold plans cost a little more, but the lower deductibles and better out-of-pocket cost sharing coverage means that families won’t have to worry about health care costs stopping them from their families getting the care they need. Even if your premium is capped you’ll have to pay more to make up the difference if you want a gold plan.

Gold plans are smart for those who don’t get CSR subsidies and need the low deductible and robust networks some gold plans provide.

4. Platinum plans split covered expenses 90-10 on average.

Platinum plans have the lowest out-of-pocket costs and the highest monthly premiums. This is the right choice for anyone who wants “the best coverage” for them and their family and is a smart buy for those who are sick or who have dependents who are likely to use costly health services. Even if your premium is capped you’ll have to pay more to make up the difference if you want a Platinum plan.

Platinum plans only make sense if your total medical spending will exceed the amount you will pay in premiums or if you need very specific treatments.

5. Catastrophic Coverage

Catastrophic coverage is available to some people under 30 and those with hardship exemptions. Catastrophic plans only cover the bare minimum health benefits and has a very limited network. You’ll have high out-of-pocket costs and a high deductible but this type of plan will protect you in a worst case scenario and will ensure that you avoid paying the shared responsibly fee for not having health coverage. If you get a catastrophic plan you should assume most of your medical costs will be out-of-pocket.

NOTE: You can also get covered through Medicaid on the marketplace. As a rule of thumb if you make less than 250% FPL a Silver plan is the way to go, if you make less than 138% and your state expanded Medicaid then you’ll go with Medicaid.

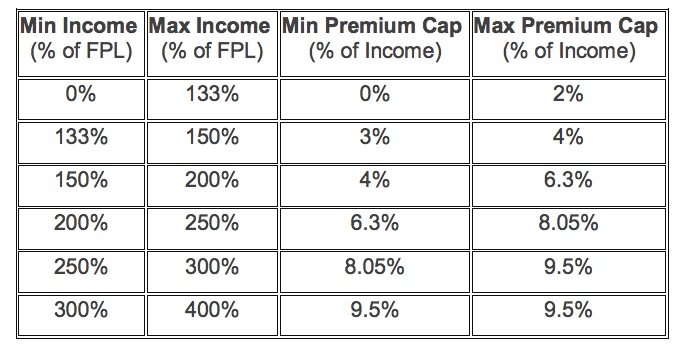

Individual Health Insurance Tax Credits

The amount of your health insurance tax credit is based on the premium for the second lowest cost “silver plan” in your state’s individual Health Insurance Marketplace.

The amount of the tax credit varies with income such that the premium you would have to pay for the second lowest cost silver plan is capped as a percentage of income (adjusted for household size), as follows:

NOTE: Below is an example of how tax credits cap premiums, exact amounts may change each year.

Income Level Premium as a Percent of Income

How to Enroll in a Qualified Health Plan

If you are ready to enroll in a Qualified Health Plan then you’ll want to check out our page on how to sign up for “ObamaCare” to understand your options inside and outside the health insurance marketplace. Don’t forget to see if you and your family qualify for cost assistance, and remember QHPs can only typically be obtained during open enrollment.

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio