What is ObamaCare?

Understanding ObamaCare (Patient Protection and Affordable Care Act)

ObamaCare is a nickname for The Patient Protection and Affordable Care Act (sometimes called the Affordable Care Act, ACA, or PPACA for short), a health reform law signed on March 23, 2010, by President Barack Obama.

ObamaCare seeks to reform health insurance and healthcare in the United States by creating new rules for insurers, offering cost assistance for health insurance, and more.

What Does the ObamaCare Do?

The Affordable Care Act (ObamaCare) aims to provide more Americans with access to affordable health insurance. It also aims to improve the quality of healthcare and health insurance, to regulate the health insurance industry, and to reduce health care spending in the US.

The law attempts to accomplish the above through a number of regulations, taxes, tax breaks, mandates, and subsidies.

For example, the law includes regulations that stop insurers from denying coverage to those with preexisting conditions, tax credits for health insurance premiums, subsidies for out-of-pocket costs, a mandate for large employers to provide full-time employees health insurance, and taxes on those who profit due to the expansion of healthcare like drug companies.

Specifically, the Affordable Care Act:

- Offers Americans some new benefits, rights, and protections regarding their healthcare and health insurance

- Sets up a Health Insurance Marketplace (HealthCare.Gov) where Americans can purchase federally regulated and subsidized health insurance during open enrollment.

- Expands Medicaid to all adults in states that embraced the program.

- Improves Medicare for seniors and those with long-term disabilities.

- Expands employer coverage to millions of employees.

- Introduces new taxes (mostly on higher earners, businesses, and industry) and tax breaks.

With that said, the above is only a part of what the Affordable Care Act does. In all the law contains over 1000 provisions. You can learn more about the benefits, rights, and protections in the Affordable Care Act here, or keep reading to learn more.

TIP: HealthCare.Gov is the official marketplace website to use if you want to lower costs on private health insurance and qualify for Medicaid under the Affordable Care Act! Make sure to shop during open enrollment for coverage inside or outside the marketplace. If you don’t obtain and maintain coverage each year, you could end up owing the Shared Responsibility Fee (please note the fee has been repealed for 2019 forward).

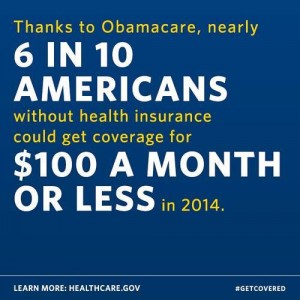

In 2014 6 in 10 without health insurance could get a plan for $100 or less. In 2016, 7 out of 10 Marketplace customers were able to get a plan for less than $75, and 8 out of 10 less than $100 (after cost assistance). The same is still generally true for 2023. Facts like this have been true each year due to the way subsidies lower premium costs. Each year many customers who shop at the marketplace can get low rates after cost assistance based on income.

What is the Health Insurance Marketplace?

The health insurance marketplace (also known as an exchange) is an online price comparison website where Americans can shop for affordable quality insurance and receive cost assistance for lower premiums, reduced out-of-pocket costs, or even qualify for Medicaid and CHIP.

Many states have their own health insurance marketplace. Meanwhile, states that don’t have their own marketplace use the federal marketplace HealthCare.Gov. Find your state’s Health Insurance Marketplace now.

ObamaCare and Cost Assistance

Cost assistance is offered on both premiums and out-of-pocket costs.

Those making between 100% – 400% of the federal poverty level (FPL) may qualify for cost assistance through the marketplace. Those making less than 138% of the poverty level may qualify for Medicaid or CHIP.

100% of the poverty level is between $13,590 for an individual and $27,750 for a family of 4 for 2023 coverage.

138% of the poverty level, is $18,754 for an individual or $38,295 for a family of 4 for 2023 coverage.

400% of the federal poverty level is $54,360 for individuals and $111,000 for a family of 4 buying 2023 coverage.

Cost assistance is only available through the health insurance marketplace.

Find out more about what ObamaCare will cost you. Many Americans will be eligible for subsidized health insurance of anywhere from roughly 2% – 9.5% of their Modified Gross Adjusted Income (or even free coverage via Medicaid and CHIP).

TIP: The poverty levels adjust every year. Make sure to check out the most recent poverty levels.

ObamaCare and Open Enrollment

Health insurance must be obtained during open enrollment. Open enrollment for health plans sold on the Health Insurance Marketplace runs from Nov 1st to Jan 15th each year in most states (unless there is an extension).

Individuals and families without access to employer coverage, Medicaid/CHIP, Medicare, or another type of “minimum essential coverage” need to enroll during open enrollment (or qualify for a special enrollment period).

Individuals and families are well advised to apply at healthcare.gov during open enrollment or apply for a special enrollment period, to see if they are eligible for financial assistance for lower premiums, reduced out-of-pocket costs, or even Medicaid (Medicaid eligibility has been expanded in many states).

Find out how you, your family, and your business can qualify for federally subsidized health insurance. Download our free ObamaCareFacts.com ebook to learn more about the Marketplace and open enrollment.

TIP: Remember, the mandate to get coverage is repealed from 2019 forward, so you won’t need to deal with exemptions moving forward.

ObamaCare Benefits, Rights, and Protections

The ACA includes a long list of new benefits, rights, and protections including:

- Letting young adults stay on their parents’ plan until 26

- Stopping insurance companies from denying you coverage or charging you more based on health status

- Stopping insurance companies from dropping you when you are sick or if you make an honest mistake on your application

- Preventing gender discrimination

- Stopping insurance companies from imposing unjustified rate hikes

- Doing away with lifetime and annual dollar limits

- Giving you the right to a rapid appeal of insurance company decisions

- Expanding coverage to tens of millions by subsidizing health insurance costs through the Health Insurance Marketplaces (HealthCare.Gov and the state-run Marketplaces)

- Expanding Medicaid to millions in states that chose to expand the program

- Providing tax breaks to small businesses for offering health insurance to their employees

- Requiring large businesses to insure employees

- Requiring all insurers to cover people with pre-existing conditions

- Making CHIP easier for kids to get

- Improving Medicare for seniors

- Ensuring all plans cover minimum benefits like limits on cost-sharing and ten essential benefits including free preventive care, OB-GYN services with no referrals, free birth control, and coverage for emergency room visits out-of-network

10 Essential Benefits

One important feature of the ACA is the new ten essential benefits included with every major medical plan.

Starting January 1st of 2014, the following “Ten Essential Benefits” had to be included under all insurance plans with no lifetime or annual dollar limits:

- Ambulatory patient services (Outpatient care). Care you receive without being admitted to a hospital, such as at a doctor’s office, clinic or same-day (“outpatient”) surgery center.

- Emergency Services (Trips to the emergency room). Care you receive for conditions that could lead to serious disability or death if not immediately treated, such as accidents or sudden illness.

- Hospitalization (Treatment in the hospital for inpatient care). Care you receive as a hospital patient, including care from doctors, nurses, and other hospital staff, laboratory and other tests, medications you receive during your hospital stay, and room and board.

- Maternity and newborn care. Care that women receive during pregnancy (prenatal care), throughout labor, delivery, and post-delivery and care for newborn babies.

- Mental health services and addiction treatment. Inpatient and outpatient care provided to evaluate, diagnose, and treat a mental health condition or substance abuse disorder.

- Prescription drugs. Medications that are prescribed by a doctor to treat an illness or condition.

- Rehabilitative services and devices – Rehabilitative services (help recovering skills, like speech therapy after a stroke) and habilitative services (help developing skills, like speech therapy for children) and devices to help you gain or recover mental and physical skills lost to injury, disability or a chronic condition (this also includes devices needed for “habilitative reasons”).

- Laboratory services. Testing provided to help a doctor diagnose an injury, illness or condition, or to monitor the effectiveness of a particular treatment. Some preventive screenings, such as breast cancer screenings and prostrate exams, are provided free of charge.

- Preventive services, wellness services, and chronic disease treatment. This includes counseling, preventive care, such as physicals, immunizations, and screenings, like cancer screenings, designed to prevent or detect certain medical conditions. Also, care for chronic conditions, such as asthma and diabetes. Note: please see our full list of Preventive services for details on which services are covered.

- Pediatric services. Care provided to infants and children, including well-child visits and recommended vaccines and immunizations. Dental and vision care must be offered to children younger than 19. This includes two routine dental exams, an eye exam and corrective lenses each year.

Changes to the Affordable Care Act

There have been some changes to the Affordable Care Act under the Trump administration. The most important change is arguably the ACA previously required you to get coverage or pay a fee.

However, under Trump the fee for not having coverage was reduced to zero starting in 2019.

Despite the changes, here in 2020 the Affordable Care Act is still “the law of the land,” and that means there is still cost assistance and protections for pre-existing conditions for Americans who choose to get covered during open enrollment each year.

(President Obama Portrait Public Domain by Whitehouse.gov)

The Politics of ObamaCare

President Obama signed the Affordable Care Act into law, but the law is actually the result of decades of ideas from both political parties and the healthcare industry. The idea of an individual mandate was first presented by current opponents of the law the Heritage Foundation in 1989. ObamaCare itself was in fact modeled after “Romney Care,” which is the nickname for the health care reform law implemented in the State of Massachusetts by the Republican Governor Mitt Romney.

Despite its non-partisan roots, the Affordable Care Act has become a hot-button and partisan political issue over time.

FACT: The nickname “ObamaCare” was given to the Affordable Care Act by critics of the law in an effort to associate then-President Barack Obama with healthcare reform efforts. The name was used because Obama championed healthcare reform as a candidate in 2008 and then as a President before signing the ACA into law. The name stuck, and Obama embraced it over time at one point saying, “I kind of like the term ‘Obamacare.’ Because I do care. That’s why I passed the bill.” Today many people know the Affordable Care Act by its nickname, “ObamaCare.”

TIP: Republicans have presented a series of bills to replace some of the Affordable Care Act’s main provisions. One such bill was called the American Health Care Act. So far none of the repeal and replace attempts have passed, but many changes have nonetheless been made over the years. Learn more about changes to ObamaCare.

FACT: The Patient Protection and Affordable Care Act and The Health Care and Education Reconciliation Act were both signed by President Obama in March of 2010. Together they contain many healthcare-related provisions that, along with subsequent judicial decisions, statutory changes, administrative actions, and sometimes legislative actions, people refer to as the Affordable Care Act (ObamaCare, Patient Patient and Affordable Care Act, ACA, or PPACA). That said, because one thing those laws did is expand health insurance and cost assistance starting in 2014, people will often use the term “ObamaCare” to refer to health insurance under “the Affordable Care Act.” The point here is, sometimes a little accuracy is put aside for simplicity when it comes to how people use the term Affordable Care Act and especially “ObamaCare.”

Why Was the ACA Passed?

The Affordable Care Act was generally passed to address different aspects of the ongoing “healthcare crisis” in the US. In other words, it was meant to address the rising costs of healthcare that were leading to tens of millions of uninsured, bankruptcies, price discrimination based on gender and health status, and even denials of coverage for those with preexisting conditions.

More ObamaCare Facts

Do you still feel like you have more to learn about the Affordable Care Act? Check out the list of ObamaCare Facts below for more insight.

• Every year during an annual open enrollment period people can obtain coverage through the health insurance marketplace, or shop outside of the marketplace.

• Many Americans making under 400% of the federal poverty level (FPL) qualify for cost assistance subsidies through the marketplace. Cost assistance comes in three forms: Premium Tax Credits (PTCs) for reduced premium costs, Cost-sharing Reduction Subsidies (CRSs) for reduced out-of-pocket costs, and both Medicaid and CHIP.

• The Affordable Care Act contains over a thousand pages of reforms to the insurance and healthcare industries to combat rising healthcare costs and to provide affordable health insurance to more Americans. Despite its overall length and complexity, most of the important reforms are contained within the first 140 pages of the law. Look at our summary of the many titles and sections of the Affordable Care Act.

• Before the ACA passed you could be denied coverage or treatment because you had been sick in the past (had a pre-existing condition), be charged more because you were a woman, or be dropped mid-treatment for making a simple mistake on your application. You had little or no way to appeal insurance company rulings effectively. Today all Americans have access to a large number of unprecedented new benefits, rights, and protections.

• As of 2013, there were around 44 million Americans who went without health insurance (about 16% of the population). The majority of uninsured were working families and others who simply could not afford health insurance. One of the major aims of ObamaCare is to help these individuals to get health insurance through expanding Medicaid eligibility and offering cost assistance through health insurance marketplaces. By the end of open enrollment 2014, less than 13% of Americans were uninsured. By 2015 the uninsured rate had fallen below 10%. The trend reversed slightly from 2017 – 2020, partly due to changes made by the Trump administration before improving again in recent years, but the uninsured rate is still lower than it was before the law and ultimately under the Affordable Care Act the uninsured rate fell to the lowest level in recent history.

• The Affordable Care Act reforms Medicare. This includes offering Medicare recipients the same new benefits, rights, and protections as everyone else, as well as reforming many aspects of the Medicare system including cuts to aspects of the program that weren’t working. Medicare isn’t part of the marketplace if you have Part A or Part C you are considered covered.

• Small businesses with less than 25 full-time equivalent employees making less than $25,000 in average annual wages are now eligible for subsidized health insurance for their employees. Learn more about ObamaCare’s subsidies.

• As of 2016 large employers had to provide health coverage to full-time workers. This helps to provide coverage to those who aren’t covered by subsidized private insurance or the expansion of Medicaid. Learn more about the employer mandate.

• From 2014 – 2019 most non-exempt Americans had to maintain minimum essential coverage throughout each year, get an exemption, or pay a per-month fee on their year-end federal income taxes for every month they went without coverage or an exemption. This “mandate” to get coverage was effectively repealed in 2019 (although some states still have their own mandate).

• Coverage that generally offers benefits, rights, and protections in-line with the ACA is called minimum essential coverage. This type of coverage can only be obtained during each kind of insurance’s open enrollment period. Individual and family private coverage, Medicare, Medicaid / CHIP, and employer coverage all have unique open enrollment periods. Outside of open enrollment periods, most people are limited to short term health insurance options, or in some cases, no options at all.

What Else Does ObamaCare Do?

Now that we know what ObamaCare is, it’s time to find out what else healthcare reform under the Affordable Care Act does beyond the key aspects of the law explained above. Here are some other important aspects of the law:

• ObamaCare, the ACA, contains many cost-curbing provisions that have helped to reduce the growth of Medicare spending and healthcare spending in general. For instance, Accountable Care Organizations (which incentivize Medicare healthcare providers to provide quality over quantity) saved over $400 million collectively in 2014. The 80 /20 rule (which requires insurers to spend at least 80 cents out of every dollar on care) led to an estimated $9 billion in savings for consumers. Also, new regulations for hospitals led to 50,000 fewer lost lives from hospital-acquired conditions and $12 billion in savings according to a 2015 report. See more examples of how the cost-controlling measures are working or learn more about the cost-controlling measures.

• ObamaCare, the ACA, improves the quality of care that Americans receive by providing better preventative and wellness services and raising the standards of basic healthcare coverage.

• ObamaCare, the ACA, eliminates pre-existing conditions and gender discrimination. No one can be charged more or be dropped from their health insurance coverage for health or gender-related reasons.

• ObamaCare, the ACA, gives tens of millions of low-income and middle-income Americans access to quality health care by providing discounts through the Health Insurance Marketplace (also known as a Health Insurance Exchange). Find out exactly what the Health Insurance Marketplace is, and how it works.

• Although the Affordable Care Act (ObamaCare) was signed into law in 2010, the health care reforms it enacts roll out year by year until 2022. Many of the biggest reforms didn’t start until 2014. Find Out More About ObamaCare Benefits and Services.

• ObamaCare, the ACA, helps to ensure that health care coverage is available to any legal U.S. resident who cannot otherwise obtain “quality” healthcare through their employer. Your access to health care is no longer entirely in the hands of health insurance companies.

• ObamaCare, the ACA, gives American employers with over 50 full-time equivalent employees the choice between providing insurance that meets the standards of ObamaCare or paying the penalty. This penalty helps to offset the cost of employees who aren’t covered through their employer to purchase insurance through the public health insurance exchanges instead of using emergency services.

• Employers with less than the equivalent of 25 full-time equivalent employees may qualify for tax credits, tax breaks, and other assistance to help them insure employees through the Health Insurance Marketplace.

• ObamaCare, the ACA, increases consumer protections. These help to protect you from being dropped while sick, denied care due to lifetime limits, or denied care for pre-existing conditions. These offer Americans more legal power against health insurance companies.

• Unless you make over $200,000 as an individual or $250,000 as a family or small business, you are exempt from almost every tax ObamaCare levies except the mandate to obtain insurance.

• ObamaCare, the ACA, expands Medicaid to millions of previously uninsured low-income Americans.

• The new healthcare law has begun to reform the healthcare industry by cutting out waste, reallocating government funding, fixing what doesn’t work, and most of all, ensuring healthcare for Americans.

We hope this answers the question “What is ObamaCare?” Now it’s time to take a look at the ObamaCare Facts and find out what its many provisions do for you.

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio