King V. Burwell Explained: The Legality of Subsidies

King V. Burwell is a lawsuit that challenges the legality of subsidies issued by the IRS on behalf of HealthCare.Gov under the Affordable Care Act (ObamaCare). If the Court sides with the plaintiffs (King) instead of Burwell (the HHS secretary), millions of people will lose their health insurance.

- You can get up-to-date information on the King V. Burwell case on the SCOTUS blog.

- On March 4th King v. Burwell will be heard by the Supreme Court. This lawsuit questions whether Federal health insurance subsidies are legal or not. Get up-to-date coverage of the oral arguments here.

Here are the basics of what you should know about King v. Burwell:

- This case is one of many that challenge the legality of subsidies, but, essentially, its the only case that has actually made it to the supreme court. Since all the lawsuits are so similar, they will all likely live or die by this ruling.

- Opponents know that the key to “breaking ObamaCare” is “breaking” subsidies, mandates, and non-discrimination (not charging women more than men, discrimination based on health, etc). This lawsuit was funded by opponents of the law for this purpose (yes, that is legal and many other lawsuits are funded this way).

- Congress doesn’t have the power to force a state to create an exchange (exchanges are health insurance marketplaces used to issue subsidies).

- Since a state can’t be forced to set up an exchange, the law (PPACA / Affordable Care Act / ObamaCare) allowed for the Federal government to set up an exchange for state’s that didn’t (HealthCare.Gov).

- Critics of the law say that the wording was purposely ambiguous to urge “play ball” and set up exchanges.

- The law never specifically says that the federal government can issue subsidies through the exchange they set up for the state. It only says that states can issues subsidies (even though essentially right after that it says the Federal government can set up the exchange for states).

- The IRS later clarified that, “the Federal government can issue subsidies”. The lawsuit challenges that they didn’t have the authority to do this.

- The lawsuit says that, “since it doesn’t say it specifically, the IRS had no right to clarify, and subsidies can only be offered by state exchanges themselves. Therefore, Healthcare.Gov and the 34 states that use it are breaking the law.”

- States depended upon HealthCare.Gov to set up their exchanges for them. For instance, a state like Oregon tried to set-up their own Marketplace, couldn’t get it right, and defaulted to HealthCare.Gov in good faith that subsidies would be issued to Oregonians.

- The lawsuit is suspiciously backed up by a cast of characters that sort of seemed cherry picked for show.however, almost all of the plaintiffs are unaffected by the law. In oral arguments the justices brought up this case. However, only one of the 4 plaintiffs actually need to show they were affected.

- Both the states and the people involved with the case seemed to have moved forward with supporting a federal exchange because they interpreted the law as allowing for Federal subsidies.

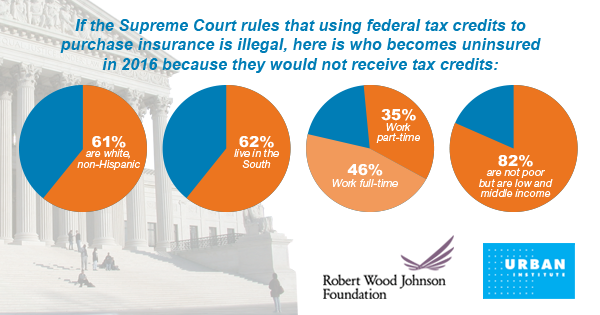

- If subsidies are declared illegal, 8.2 million Americans may lose access to subsidies.

- In state’s that support ObamaCare the fixes are easy and numerous, but also expensive. The most simple answer being for affected states to set up a state exchange and transferring everything over.

- The issue is, in very anti-ObamaCare state’s, where certain state politicians have been creeping in, and anti-ObamaCare support is strong… State’s will most likely refuse to set up exchanges.

- So we risk a divided country where a core group of states rejected Medicaid (already done) and may reject subsidies (we can assume essentially the same states will do this), while the rest of the country expands and reforms healthcare under the PPACA.

The long story short, the latest battle to repeal ObamaCare at a state level begins March 4th when the first arguments are heard, but we won’t know the outcome until at least June.

If the ruling is against subsidies, then we are one step closer to the ALEC based model of healthcare reform (essentially healthcare reform with less subsidies and less regulations which favors businesses) and one step away from the PPACA (healthcare reform with subsidies and regulation which favors people).

Author: Thomas DeMichele

Thomas DeMichele is the head writer and founder of ObamaCareFacts.com, FactsOnMedicare.com, and other websites. He has been in the health insurance and healthcare information field since 2012. ObamaCareFacts.com is a...

Thomas DeMichele's Full Bio

Megan

hopefully they get all this figured out. I spent the last 6 months fighting to get the market place and the insurance company on the same page. Turned out the person we talked to over the phone clicked something wrong. What ever they clicked in January couldn’t be fixed but no one could see this problem but the computers. I wasted about 90+ hours of my life trying to fix something that couldn’t be fixed. Now what do I do the market place screwed me over. Now I have no insurance and am fighting them on paying back payments I made. Since I never had insurance there’s no reason to keep payments for nothing right.

ObamaCareFacts.comThe Author

That is an unfortunate situation. If someone can get a Marketplace plan (enroll in a plan through the Marketplace) they can claim their own tax credits at tax time using form 8962. Marketplace approval is NOT needed. That being said, the Marketplace IS needed to get advanced premium tax credits, to make sure payments done through the site make it to the insurer, and to make sure when you choose a plan through them the insurer knows and that first months premium is paid. You can appeal all of this, although that may be something you have already tried: https://obamacarefacts.com/appeal-health-insurance-denial/

Henry O. Harwell

I may share Mr Busack’s opinion that the Supreme Court has become “an increasingly political branch of the gov’t,” (sic), but I hardly agree with the outcome he proposes, namely that the Court will be intimidated into siding with the current status quo. This is a struggle within the ruling elites of this country; whether the parties truly give a d*** is questionable. The spirit of the law is pretty clear, at least at one level, and that is that uninsured people who need assistance to obtain health care ought to able to do so. Further, that having fewer people without health coverage would reduce the burden on our emergency rooms and give people a stake in their own health with wellness exams. The list goes on. Just the opportunity for young adults to stay with their parents’ health plan while still in school is a an immense benefit for the society. Ending de facto discrimination against women and those with some excluded pre-existing conditions are really no-brainers that the male-dominated insurance industry would never have changed on their own. The question is, of course, for all those good Christians out there — Are you your brother’s keeper, or not.

vta

irregardless of how this law was written, and how it will be decided, this is just a bad law. it was rammed down the people’s throat. its pretense, “affordable” , is really an oxymoron, affordable/expensive, for most people. it’s real purpose is just a huge (federal) government takeover. most know that government is much less efficient than private business, or a well run state government.

if this law was prepared in a fairer, more truthful fashion, by legislation that enabled it to work i. e. tort reform, being allowed to purchase less expensive drugs, being able to purchase insurance across state lines, etc. etc., it would have been embraced, it could have worked for everyone.

instead, it is an abomination (obamanation).

hopefully scotus will take some of these words into consideration.

Douglas

There are reasons why many presidents had tried and failed to pass health insurance laws. Democratic Congressman rammed this through the Congress in a strictly party line vote.

Why should any vote that affects almost every American be allowed to stand under such circumstances? We do need affordable health insurance in this country. The ACA is a total failure. It has taken insurance from millions of people who already had it.

It has significantly raised deductibles. This makes most policies virtually worthless. This is the key part of the law that the insurance companies and President Obama do no want you to know. The insurance companies make you pay several thousand dollars before you see one penny of benefit.

Now we have this issue. The law was passed that said each state was to set up its own marketplace. What the writers of the law did not count on was that the majority of states have decided not to set up their own marketplace. Without a marketplace, these people have no right to a subsidy.

Douglas

Subsidies need to be available or no one at all.

Any attempt for the court to say otherwise would be unconstitutional.

Lynn

I feel we have 2 Governments trying to run this country (Democrats and Republicans) .Its not about what is best for the people Its more on which side you sit on. It is suppose to be “we the People”…I guess maybe we should rewrite it to say “we the politicians” Personally speaking I am for the Obama care. I hear what it hasn’t done- But stop and look at what it has done for Millions of people that could not afford it other wise……..AND NO… I PERSONALLY AM NOT ON OBAMA CARE…But when people cannot afford Health Insurance and they go to the hospital and can’t afford to pay. Who in the end pays. We do, Hospital and Medical bills has to pass the cost to somebody. March 4th it faces a law suit supposedly by 4 People, Two of these people are veterans, which is probably getting VA benefits, The other one is a woman that was in a motel room ( and now they do not where she is) and the other one is a school teacher that says she does not know how she got involved . Give me a break.

Duane Stillabower

Them republicans will not stop until people have no insurance again . What is wrong with them?

Larry Busack

Obamacare and the Supreme Court

The latest challenge to Obamacare seems to be an argument over health insurance subsidies. Some people qualify for federal subsidies if they buy their health insurance through an insurance exchange “established by the STATE”

In common language the state includes both the federal government and/or an individual state. If Obamacare was intended to only include US state established exchanges, then it seems that STATES would be used instead of STATE. Unless Congress believed that only 1 state would set-up an exchange (a typical pork project for one lucky state)

In general usage the word state often applies to the federal government, similar to the French State or the German State. If Congress truly meant that only an exchange created by a US state would qualify, then they would also mean that the people of Kentucky, Massachusetts, Pennsylvania, and Virginia would not qualify for a federal subsidy because these are COMMONWEALTHS, not STATES. Also no one in the District of Columbia would be eligible for subsidies.

If state does not mean STATE, then it seems inappropriate that the Fourth Circuit Court of Appeals would have been an inappropriate place to hear the initial appeal because it is located in Richmond, Virginia and Virginia is a COMMONWEALTH and not a STATE.

Brian

This is going to be interesting and have far-reaching consequences (i.e., applicable to all laws): Going forward in the U.S., do we go by the letter of the law or the spirit/intent of the law?

zuzu

According to the man who submitted the Act (Baucus), the spirit/intent was to use the subsidies as carrot to get states to set up their own exchanges. So they could go with either, and the result should be the same. However, the SCOTUS has become an increasingly political branch of the gov’t, and I wouldn’t be surprised if they’re (Roberts in particular) scared into siding with Obamacare and the Dems, to avoid the inevitable smear campaign the left leaning media would wage.